Revolving Credit Mortgages: Pros and Cons for Kiwis

Imagine turning your everyday bank account into a powerful tool that chips away at your mortgage interest every time you deposit your paycheck. That's the promise of a revolving credit mortgage (RCM)...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Imagine turning your everyday bank account into a powerful tool that chips away at your mortgage interest every time you deposit your paycheck. That's the promise of a revolving credit mortgage (RCM) for Kiwis looking to get ahead on home loan repayments. But with great flexibility comes the need for ironclad discipline—let's dive into the pros, cons, and real-world strategies to see if it's right for you in 2026.

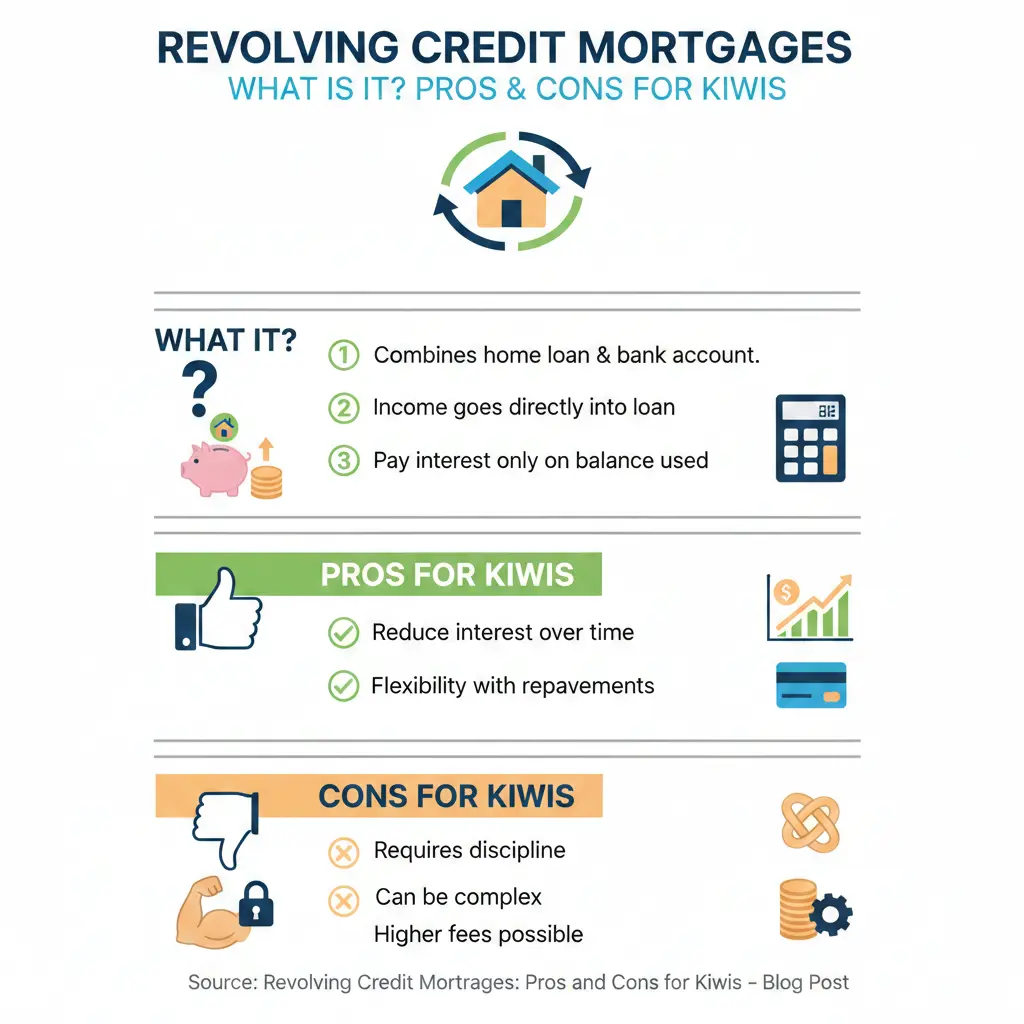

What is a Revolving Credit Mortgage?

A revolving credit mortgage functions like a massive overdraft tied to your home equity, typically at a floating home loan rate around 4-6% rather than the steeper 15% of standard overdrafts. You deposit your income into this account, use it for bills and spending, and only pay interest on the outstanding daily balance—meaning every dollar you pay in reduces your interest bill instantly.

Unlike traditional mortgages with fixed repayments, there's no set schedule; you draw down as needed and repay flexibly. Banks like ASB, Kiwibank, and others offer RCMs, often as part of a mixed mortgage structure where you split your loan across fixed, floating, interest-only, or revolving options. To qualify, you'll generally need at least 20% equity in your home post-RCM setup, ensuring the bank has security.

How Does It Work in Practice?

Picture this: Your RCM limit is $100,000. You deposit your $2,000 weekly pay—balance drops to $98,000, interest calculated daily on just that amount. Spend $1,500 on bills, it rises back up, but you've saved interest on the full pay for those days it sat there. Use it as your everyday transaction account, and it becomes a seamless way to minimise interest while maintaining access to funds.

In 2026, with New Zealand's housing loan book at $389 billion and many Kiwis refixing off higher 2023-2024 rates, RCMs shine for those facing floating rates around 6% or 1-year fixed in the low 5%s.

Pros of Revolving Credit Mortgages for Kiwis

RCMs offer smart ways to leverage cashflow in our high-cost living environment. Here's why many Kiwis swear by them:

- Interest Savings on Daily Balances: Pay interest only on what's drawn down, not the full limit. Depositing salary can slash interest significantly—far more efficient than standard mortgages.

- Ultimate Flexibility: No fixed repayments or dates; ideal for irregular incomes like contractors or seasonal workers. Pay what you can, when you can, and redraw anytime without penalties.

- Accelerates Mortgage Payoff: Strategies like the "Mortgage Buster" build savings in the RCM (e.g., $300/week to $15,000/year), then lump-sum it to your main mortgage—rinsing and repeating to finish years faster.

- Everyday Account Integration: Combine bill payments and salary deposits to keep balances low, saving pennies daily that add up hugely over time.

- Mixed Loan Compatibility: Pair with fixed or offset portions for tailored strategies, common in NZ where many banks allow splits.

Real Kiwi Example: Saving on a New Build Deposit

For property investors eyeing new builds, set up a 20% deposit RCM: Pay 10% upfront, save the rest in the facility (earning no interest but reducing loan interest), then access at settlement. This bridges the gap without tying up cash elsewhere.

Cons of Revolving Credit Mortgages for Kiwis

While powerful, RCMs aren't for everyone. Discipline is key, or they can backfire spectacularly.

- Higher Interest Rates: Floating rates average 0.91% above 1-year fixed (historically), sitting under 6% in 2026—costly if you don't actively reduce the balance.

- Requires Rock-Solid Discipline: Easy access tempts overspending; without budgeting, balances stay high, accruing more interest than fixed options.

- Not for Full Mortgages: Banks limit RCM portions (often 20-30% of loan) due to risk, and full conversion means paying premium floating rates on everything.

- Fees and Charges: Setup fees, potential annual fees, and daily interest calculation mean small balances still cost—plus no tax deductibility for personal use.

- Risk in Rising Rates: Variable rates fluctuate with the OCR (now 2.25% but subject to change), exposing you more than fixed terms.

- Equity Requirements: Need 20%+ equity; not viable for low-equity homeowners or first-timers.

Offset vs Revolving: Quick Comparison

| Feature | Revolving Credit | Offset |

|---|---|---|

| Interest Calculation | Daily on outstanding balance | On net balance after offset |

| Flexibility | High—draw/redraw freely | Lower—funds stay in offset |

| Tax Implications | Withdrawals non-deductible | Offset funds earn no interest (tax-free shelter) |

| Best For | Cashflow managers | Savers with stable extras |

| Rate | Floating ~6% | Matches loan rate |

Many Kiwis combine both for optimal results.

Who Should Consider a Revolving Credit Mortgage in 2026?

Ideal for disciplined Kiwis with steady incomes, 20%+ equity, and goals to pay off faster. Great for self-employed with lumpy cashflow or those using Mortgage Buster tactics. If you're refixing in 2026 amid OCR cuts and lower rates, splitting into RCM could optimise cashflow.

Avoid if you're prone to impulse spending or prefer payment certainty—stick to fixed terms instead.

Practical Tips for Using Revolving Credit Mortgages Effectively

- Start Small: Limit RCM to 20-30% of your mortgage; keep the rest fixed for stability.

- Budget Ruthlessly: Track every dollar—apps like PocketSmith or bank tools help. Aim to keep balances under 50% daily.

- Direct All Income Here: Salary, KiwiSaver bonuses, side hustles—funnel everything to maximise interest savings.

- Use Mortgage Buster: Save set amounts weekly, lump-sum annually to principal. Models show it shaves years off loans.

- Monitor Rates: Compare bank specials via sites like MoneyHub; switch if better floating rates emerge.

- Talk to a Broker: Free advice from mortgage advisers ensures it fits your IRD, ACC, and overall finances.

- Combine Strategies: Pair with offsets for family savings or low-rate investments.

ASB's Orbit options let you choose fixed or reducing limits for added control.

Next Steps for Kiwis Eyeing Revolving Credit

Crunch your numbers: Use online calculators to model interest savings based on your cashflow. Chat with a mortgage broker for personalised splits, check current specials, and ensure it aligns with your budget. With rates easing in 2026, now's a prime time to restructure and get ahead—discipline turns RCMs into mortgage accelerators, but mismanagement does the opposite. Ready to revolving your way to freedom?

Frequently Asked Questions

Sources & References

-

1

Revolving Credit Mortgages - MoneyHub NZ — www.moneyhub.co.nz

-

2

Revolving Credit: What Is It and How to Use It in 2026 | Opes Partners — www.opespartners.co.nz

-

3

New Zealand's Mortgage Market Update – What Borrowers Should ... | Te Korowai — te-korowai.org.nz

-

4

Revolving mortgage - Giving you flexibility - ASB Bank — www.asb.co.nz

-

5

Offset vs Revolving in New Zealand Mortgages — Which Structure ... | Prosperity Finance — prosperityfinance.co.nz

-

6

Revolving credit vs offset home loans | Which mortgage option is ... | Property Brokers — www.propertybrokers.co.nz

-

7

Refixing in 2026: A Decision Framework (Split, Float, or Fix Longer?) | New Zealand Mortgages — www.newzealandmortgages.co.nz

-

8

Revolving home loan - Kiwibank — www.kiwibank.co.nz

- 9

-

10

Compare Revolving Credit Mortgages - Finance.co.nz — finance.co.nz

Related Articles

Using the NZ Mortgage Calculator to Plan Your House Hunt

Imagine spotting your dream home in Auckland or Christchurch, but wondering if you can actually afford it. That's where the NZ Mortgage Calculator comes in—your essential tool for turning house-huntin...

Mortgage Refixing Guide: How to Negotiate the Best Rate with Your Bank

Imagine slashing hundreds of dollars off your weekly mortgage payments just by knowing when and how to refix. With interest rates easing in 2026, thousands of Kiwis are facing refix decisions that cou...

Mortgage Refinancing: When Does It Make Sense?

Imagine shaving thousands off your mortgage interest while unlocking cash for that home reno or debt consolidation you've been dreaming about. For Kiwis with home loans, mortgage refinancing can be a...

How to Pay Off Your Mortgage Faster (NZ Strategies)

Imagine owning your home outright years earlier than planned, freeing up thousands in interest payments and giving you financial freedom sooner. For Kiwis with mortgages, paying off your home loan fas...