KiwiSaver Default Funds: Are You Still in One?

Ever wondered if your KiwiSaver savings are parked in a default fund, quietly chugging along without you steering the ship? With over 3 million Kiwis in KiwiSaver and total funds hitting $111.8 billio...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Ever wondered if your KiwiSaver savings are parked in a default fund, quietly chugging along without you steering the ship? With over 3 million Kiwis in KiwiSaver and total funds hitting $111.8 billion as of March 2024, many are still in these automatic options—potentially missing out on returns tailored to their life stage or goals. As we head into 2026 with fresh changes like the default contribution rate jumping to 3.5% from April, it's time to check your settings and see if a switch could supercharge your retirement or first home deposit.

This guide breaks down everything you need to know about KiwiSaver default funds: what they are, how they've evolved, their performance, and practical steps to review or change yours. Whether you're a new grad auto-enrolled at work or a long-time member who's never looked back, here's how to make your money work harder for you.

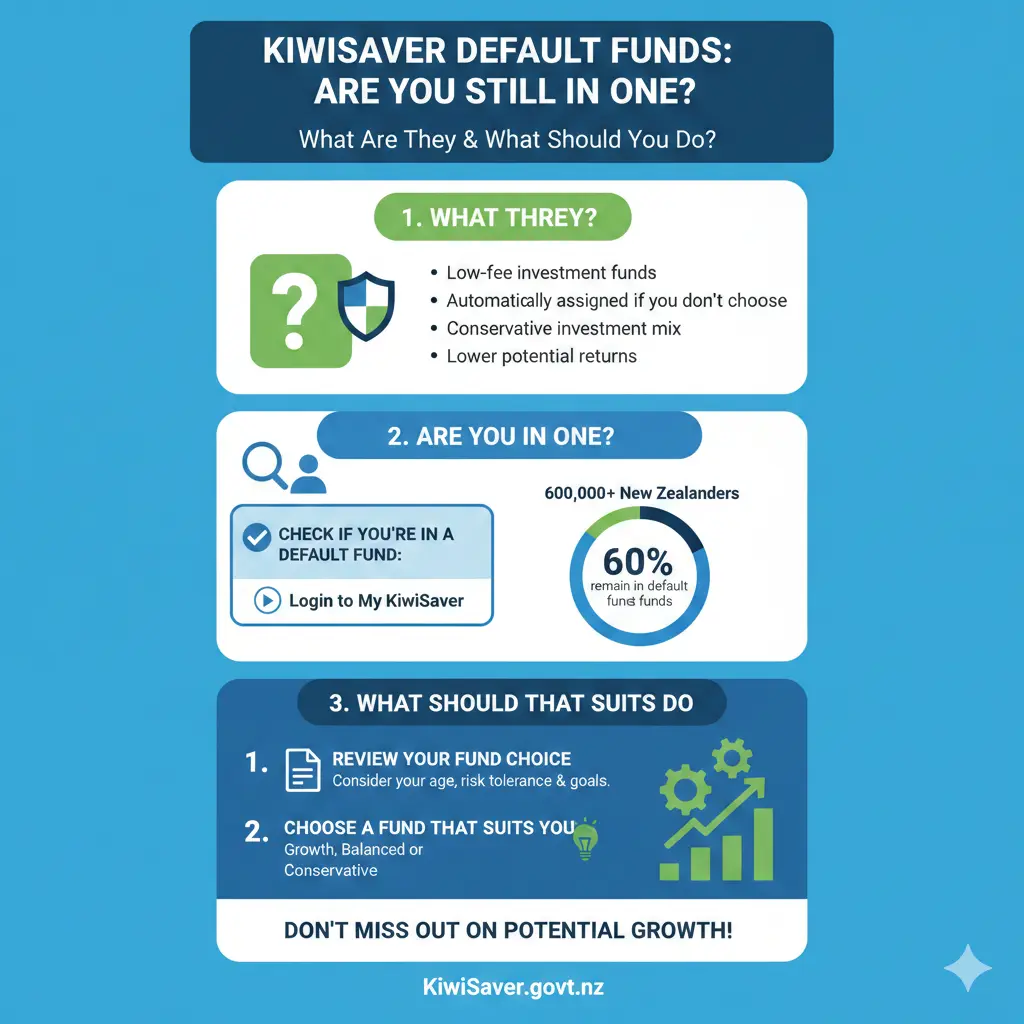

What Are KiwiSaver Default Funds?

KiwiSaver default funds kick in when you're automatically enrolled—typically new workers aged 18-65 who don't pick a provider. Your employer sorts it, placing you with one of six appointed providers: BNZ, Booster, BT Funds Management (Westpac), Kiwi Wealth, Simplicity, or Smartshares (NZX). These providers hold seven-year terms, with the current ones running until 1 December 2028.

Default funds aren't your average conservative option anymore. Pre-2021, they mirrored low-risk conservative funds, prioritising capital protection over growth. But from late 2021, the government shifted policy to a balanced mix—now targeting 35-63% growth assets like shares, with the rest in income assets such as bonds and cash. Simplicity's default fund, for example, holds 59% growth (43.5% international shares, 15.5% NZ shares) and 41% income assets (10% cash, 16.5% NZ fixed interest, 14.5% international fixed interest), suited for medium-term growth over 6+ years.

Why the Shift to Balanced?

The change aims for higher long-term returns while keeping volatility in check. Balanced/default funds offer more growth potential than conservative ones (0-34.9% growth assets) but less risk than growth funds (over 63% growth). No Crown guarantee backs these investments, so returns aren't promised, but diversification across assets helps smooth ups and downs.

For many Kiwis, this suits retirement saving—locked in until 65 (with exceptions like first home withdrawals). But if you're eyeing a house soon, a conservative fund might protect your balance better.

Recent Changes to KiwiSaver in 2026

Budget 2025 brought big tweaks to boost savings sustainability. From 1 April 2026, the default employee and employer contribution rate rises from 3% to 3.5% of salary, phasing to 4% by 1 April 2028. You can opt down to 3% if cashflow's tight—it resets after 12 months, but you can re-opt.

Government contributions halved to 25 cents per dollar you put in (max $260.72 yearly), effective from 1 July 2025. Hit the full whack by contributing at least $1,042.86 by 30 June. Sixteen and 17-year-olds now qualify for employer matches too.

How These Hit Your Pay Packet

- 3.5% default from April 2026: On a $60,000 salary, that's $35 fortnightly more from you and your employer—building your balance faster.

- Opt-down option: Ideal if living costs bite, but expect the auto-reset to nudge you up.

- Govvie top-up: Still free money—contribute steadily to max it, even if suspending for up to 12 months.

These shifts mean default funds will grow quicker at the new rates, padding retirement nests and first home deposits.

Performance of Default Funds: What to Expect

Default funds aim for steady growth with moderate risk. ANZ's Default KiwiSaver Scheme (high growth tilt in parts) showed 6.65% over 3 months, 10.49% over 1 year to 31 August 2025 (before tax, after fees). Simplicity notes higher long-term returns than conservative but lower than pure growth, with volatility in between.

Fees Matter More Than You Think

Defaults are low-cost by design, but fees erode returns as balances grow. Your annual statement lists dollar fees, influenced by balance size, fund type, and provider. Lower-risk funds cost less but return less overall. Compare via Sorted's KiwiSaver fund finder.

| Fund Type | Growth Assets | Risk/Return Profile | Best For |

|---|---|---|---|

| Defensive/Conservative | 0-34.9% | Low volatility, predictable | Near-term withdrawals |

| Balanced/Default | 35-63% | Medium growth, moderate ups/downs | Retirement 10+ years away |

| Growth | 63%+ | High potential, volatile | Long horizon, high tolerance |

Past performance isn't future-proof—diversify and match your risk appetite.

Are Default Funds Right for You?

If you're hands-off and saving for 65, defaults work fine—low fees, balanced risk, auto-enrolment simplicity. But life changes: nearing retirement? Switch conservative. Saving for a home? Defensive might shield from market dips.

Check if you're still defaulted: Log into your provider's portal or call them. Over 40% of KiwiSaver funds invest in NZ assets, so staying boosts local economy too.

Pros and Cons

- Pros: Automatic, low-cost, balanced for most, easy access for anyone.

- Cons: Not personalised—may underperform if mismatched (e.g., high risk tolerance), no guarantees.

How to Check If You're in a Default Fund

- Review statements: Your annual KiwiSaver statement shows fund name, provider, and fees.

- Log in online: Providers like Simplicity, BNZ, or Kiwi Wealth have dashboards—search for "fund type" or "default".

- Contact employer/HR: They enrolled you; ask for details.

- Use Sorted: Free tool at Sorted KiwiSaver Fund Finder compares everything.

- Call FMA hotline: If unsure, Financial Markets Authority monitors all schemes.

Steps to Switch Out of a Default Fund

Switching is free and straightforward—no lock-in penalties.

- Choose a provider/fund: Compare on Sorted for returns, fees, ethics (e.g., Simplicity's low-fee focus).

- Apply online/in-app: Most let you transfer seamlessly—new contributions go to the new fund, old balance can follow or split.

- Notify employer: Update your contribution rate if changing (e.g., to 4%, 6%, 8%, or 10%).

- Track transfer: Takes days to weeks; confirm via statements.

Pro tip: If volatility worries you post-switch, direct new money only—leave existing in default.

Contribution Tips Post-2026 Changes

- Opt up to 4%+ for max growth, especially with employer match.

- Never suspend long-term—miss govvie $521.44 max and employer input.

- Voluntary after-tax boosts eligible for govvie top-up.

KiwiSaver for First Home or Retirement

Defaults suit long-haul retirement but tweak for homes: Withdraw after 3 years (plus $5k min contribution), but market crashes hurt balanced funds. Go conservative 2-3 years pre-withdrawal. First Home Withdrawal lets you pull savings tax-free for deposit.

For retirement, defaults build steadily—average balance $33,514 in 2024, growing with 3.5% rates.

Next Steps: Take Control Today

Don't let defaults decide your future by default. Log in now, check your fund, compare on Sorted, and adjust contributions ahead of April's 3.5% hike. Small tweaks compound hugely—your 65-year-old self (and maybe first-home buyer) will thank you.

Disclaimer: This isn't personalised financial advice. Consult a licensed adviser or use free Sorted tools for your situation. Tax rules via IRD; KiwiSaver via FMA.

Frequently Asked Questions

Sources & References

-

1

KiwiSaver changes to encourage savings | Beehive.govt.nz — www.beehive.govt.nz

-

2

Default KiwiSaver Fund - Simplicity — simplicity.kiwi

-

3

KiwiSaver default funds | Ministry of Business, Innovation and Employment — www.mbie.govt.nz

-

4

KiwiSaver - Financial Markets Authority — www.fma.govt.nz

-

5

KiwiSaver changes explained: How the new rules will hit pay packets | NZ Herald — www.nzherald.co.nz

-

6

ANZ-managed KiwiSaver scheme fund performance and fees | ANZ — www.anz.co.nz

-

7

KiwiSaver Changes - 22 January 2026 | Bay Financial Partners — www.bayfinancialpartners.co.nz

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...