Rental Property Depreciation NZ: What You Can Claim

If you're a Kiwi property investor, understanding depreciation rules is crucial for maximising your tax deductions and keeping more money in your pocket. The landscape has shifted significantly in rec...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

If you're a Kiwi property investor, understanding depreciation rules is crucial for maximising your tax deductions and keeping more money in your pocket. The landscape has shifted significantly in recent years, and knowing what you can and can't claim could save you thousands of dollars. Let's walk through the current rules, what's changed, and how to make the most of your rental property investment.

Understanding Depreciation on Rental Properties

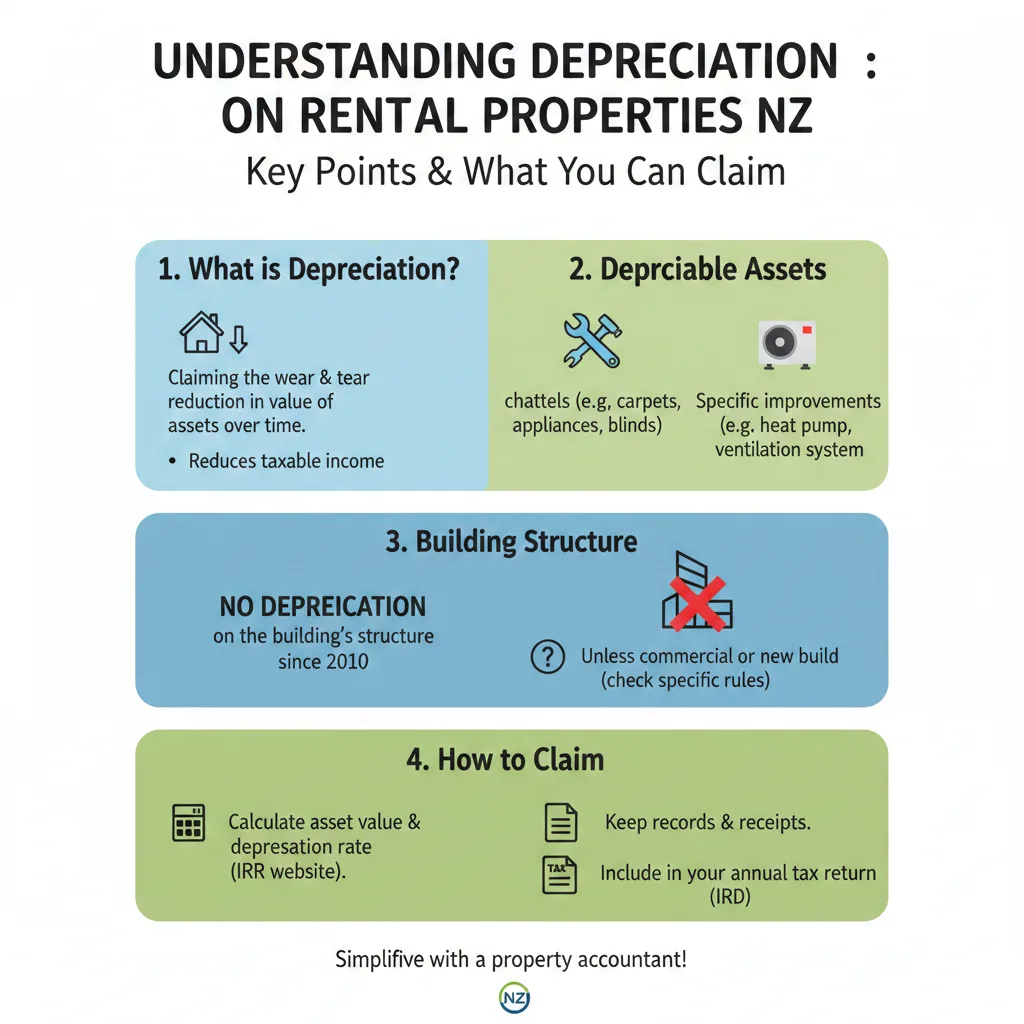

Depreciation is a tax deduction that recognises the wear and tear of assets used in your rental business. When you own a rental property, certain assets lose value over time, and the IRD allows you to claim a deduction for this loss. This includes everything from chattels (moveable items like appliances and furniture) to building components, though the rules around buildings themselves have changed dramatically.

The basic principle is straightforward: if you own an asset that depreciates, you can claim a percentage of its cost as a deductible expense each year. However, the rules differ significantly depending on what type of asset you're claiming for.

What Changed in 2024: The Big Picture

From 1 April 2024, depreciation deductions for commercial and industrial buildings were removed entirely. This means the status quo that existed from 2011 through to 2020 has been restored. However, residential buildings have a different fate—they've never been depreciable for tax purposes, and that hasn't changed.

This shift represents a significant change in policy. Previously, property investors could claim depreciation on building components, but those days are largely behind us now. What you can still claim depreciation on are chattels—the separate assets within your rental property that are valued over $1,000.

What You Can Claim Depreciation On

Chattels and Moveable Assets

Chattels are your best opportunity for depreciation claims. These are items like ovens, fridges, furniture, and other moveable assets that are separate from the building itself and valued over $1,000. Each chattel has an IRD-prescribed depreciation rate that determines how much you can claim each year.

How it works in practice: Let's say you purchase a commercial-grade fridge for your rental property for $2,000. The IRD's depreciation rate for fridges is 25% annually. In your first financial year, you'd be entitled to claim a depreciation deduction of $500 (25% of $2,000). If you purchased the fridge partway through the financial year, you'd need to pro-rate this amount based on how many days you owned it.

Other common chattels you might claim include:

- Kitchen appliances (ovens, microwaves, dishwashers)

- Furniture and furnishings

- Carpets and floor coverings (if installed separately from the building)

- Light fittings and ceiling fans

- Air conditioning units

Depreciation Methods

For tax purposes, depreciation can be calculated using three methods:

- Diminishing-value method: You claim a percentage of the remaining value each year, so your deduction decreases over time

- Straight-line method: You claim the same amount each year over the asset's useful life

- Pooling method: You group similar assets together and claim depreciation on the pool as a whole

You must use the economic depreciation rates prescribed by the Inland Revenue, unless you apply for a special depreciation rate.

What You Can't Claim Anymore

Building Depreciation

This is the big one. From 1 April 2024, you can no longer claim depreciation on commercial and industrial buildings. If you purchased a building before this date and were claiming depreciation, you need to stop claiming it from 1 April 2024 onwards.

Residential buildings have never been depreciable for tax purposes, so if you're investing in a residential rental property, building depreciation has never been available.

Building Fit-Out (15% Provision)

The 15% provision for fit-out (for buildings acquired on or before the 2010-11 income year) has also been removed from 1 April 2024. If you're a property investor who separated out building fit-out from the main building, the IRD directs you to seek an amendment to your income tax returns for the years in which building depreciation existed.

Assets Under $1,000

Assets with a cost base of less than $1,000 are immediately deductible in the year of purchase, rather than being depreciated over time. This is a practical rule that means you don't need to track small items—you can simply deduct them as an expense in the year you buy them.

Timing Matters: Pro-Rata Depreciation

Here's an important practical tip: depreciation is calculated on a pro-rata basis depending on when you acquired the asset during the financial year. If you buy a chattel in March (near the end of the financial year), you'll only be able to claim a small portion of the depreciation for that year. It's not worth rushing to buy chattels late in the financial year just to offset your tax liability—you'll get a better deduction if you purchase them earlier in the year.

How Depreciation Fits With Other Tax Changes

Depreciation is just one piece of the rental property tax puzzle. You should also be aware of two other significant changes that affect rental property investors:

Interest Deductibility Restoration

From 1 April 2025, you can now claim 100% of the interest you incur on your rental property mortgage. This is a major win for investors. From 1 April 2024 to 31 March 2025, you could claim 80% of the interest you incurred. This applies regardless of when you purchased the property or drew down the loan.

The Bright-Line Test

From 1 July 2024, the bright-line test returned to a two-year period. This means if you sell your rental property and have owned it for two years or less, you'll be taxed on any capital gains you make. If you've owned it for more than two years, the gain is generally not taxed.

Practical Steps for Claiming Depreciation

If you're planning to claim depreciation on your rental property, here's what you need to do:

- Identify your chattels: Walk through your rental property and list all moveable assets valued over $1,000

- Find the IRD depreciation rate: Look up the prescribed rate for each asset type on the IRD website

- Calculate the deduction: Multiply the cost by the depreciation rate, then pro-rate based on when you acquired it during the financial year

- Keep records: Maintain receipts and documentation for all chattels you're claiming

- Include on your tax return: Report your depreciation deductions when you file your tax return with the IRD

Ring-Fencing Rules: Important Limitations

From 1 April 2019, deductions for expenditure incurred in relation to residential rental properties are limited to the extent of the residential income derived. This means if your rental expenses (including depreciation) exceed your rental income, you can't use the excess to offset other income. Instead, the excess is "ring-fenced" and carried forward to offset against future residential rental income.

This is an important limitation to understand. It means depreciation deductions won't reduce your overall tax bill if your rental property is running at a loss—they'll simply accumulate as a loss to carry forward.

Frequently Asked Questions

Can I claim depreciation on my residential rental building itself?

No. Residential buildings have never been depreciable for tax purposes in New Zealand. You can only claim depreciation on chattels (moveable assets valued over $1,000) within the property.

What if I purchased a building before 1 April 2024 and was claiming building depreciation?

You must stop claiming building depreciation from 1 April 2024 onwards. If you'd like to amend your previous tax returns for years when building depreciation was available, the IRD directs you to seek an amendment.

How do I know what depreciation rate to use for my chattels?

The IRD prescribes economic depreciation rates for different asset types. You must use these prescribed rates unless you apply to the IRD for a special depreciation rate. Common examples include fridges at 25% annually.

If I buy a chattel in March, can I claim full depreciation for that year?

No. Depreciation is pro-rated based on how many days you owned the asset during the financial year. A purchase in March will only give you a small deduction for that year, so it's not worth rushing to buy chattels late in the financial year just to offset your tax liability.

What's the difference between depreciation and interest deductibility?

Depreciation is a deduction for the wear and tear of assets. Interest deductibility allows you to deduct the mortgage interest you pay on your rental property. From 1 April 2025, you can claim 100% of your mortgage interest. These are separate deductions that work together to reduce your taxable rental income.

Will ring-fencing rules prevent me from claiming depreciation?

Ring-fencing rules limit how you can use rental property deductions, but they don't prevent you from claiming depreciation. If your rental expenses exceed your rental income, your depreciation deduction will be carried forward to offset future rental income, rather than reducing your overall tax bill.

Next Steps for Property Investors

Understanding depreciation is just one part of optimising your rental property investment. Here's what we recommend:

Review your current situation: If you've been claiming building depreciation, you need to stop as of 1 April 2024. Check whether you need to amend any previous tax returns.

Identify your chattels: Make a comprehensive list of moveable assets in your rental property valued over $1,000 and research the IRD depreciation rates for each.

Maximise interest deductibility: Remember that from 1 April 2025, you can claim 100% of your mortgage interest. Make sure you're not missing out on this significant deduction.

Keep detailed records: Maintain receipts, invoices, and documentation for all chattels and rental expenses. Good record-keeping makes tax time much easier and protects you if the IRD ever questions your claims.

Consider professional advice: Given the complexity of rental property tax rules and ring-fencing limitations, it's worth speaking with a tax accountant or financial adviser who specialises in rental property investment. They can help you optimise your deductions and ensure you're complying with all the rules.

The rental property tax landscape has changed significantly in recent years, but there are still genuine opportunities to reduce your tax bill through depreciation claims and interest deductibility. By understanding what you can claim and keeping meticulous records, you'll be in a strong position to maximise your rental property investment returns.

Related Articles

Working Multiple Jobs NZ: Tax and Legal Considerations

Juggling multiple jobs can boost your income, but it's crucial to understand the tax implications and legal requirements that come with working more than one role in Aotearoa. Whether you're a contrac...

Name Changes NZ: Legal Process and Costs

Considering a fresh start with a new name? Whether it's after marriage, divorce, or simply embracing a personal transformation, changing your name in New Zealand is straightforward but requires follow...

Holiday Home Tax Rules NZ: Private Use and Rental

Own a bach in Coromandel or a holiday home in Queenstown? You're not alone—many Kiwis cherish these escapes, but renting them out while enjoying personal use can trip you up on tax rules. Getting the...

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...