Mortgage Pre-Approval: What You Need to Know

Imagine finding your dream home in Auckland or Christchurch, only to lose it to another buyer because your finance wasn't sorted. That's where mortgage pre-approval NZ comes in—it's your ticket to sta...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Imagine finding your dream home in Auckland or Christchurch, only to lose it to another buyer because your finance wasn't sorted. That's where mortgage pre-approval NZ comes in—it's your ticket to standing out in New Zealand's competitive property market, showing sellers you're serious and ready to go.

Whether you're a first-home buyer dipping into KiwiSaver or upsizing your family home, getting pre-approved gives you clarity on what you can afford and strengthens your offers. In this guide, we'll walk you through everything you need to know, from the step-by-step process to essential documents and tips tailored for Kiwis in 2026.

What is Mortgage Pre-Approval?

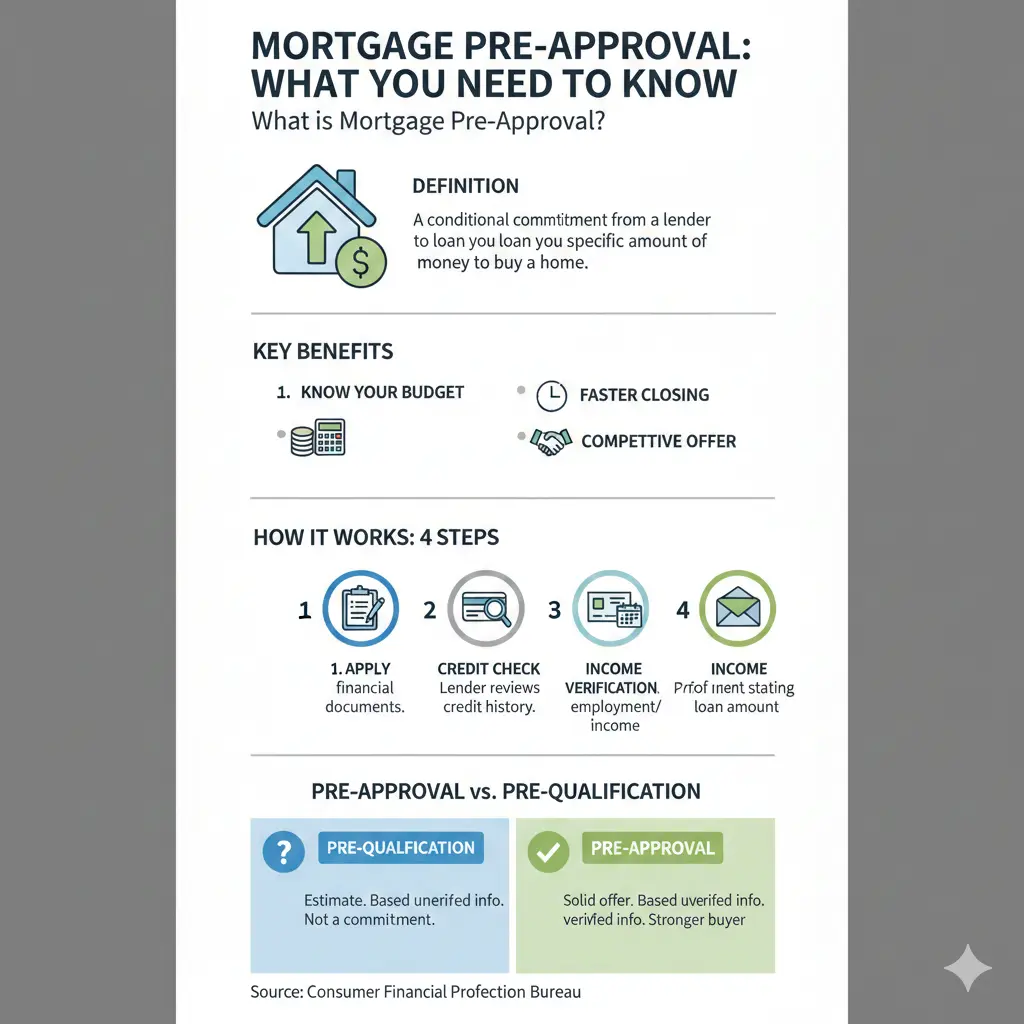

Mortgage pre-approval is a lender's written confirmation of how much they're willing to lend you, based on your financial situation—before you've even found a property. It's not a full loan offer, but a conditional green light that typically lasts 60-90 days.

In New Zealand, banks assess your income, expenses, credit history, and deposit to give you key details like your maximum borrowing amount, affordable property price, required deposit, and estimated repayments. This helps you house hunt with confidence, knowing your limits.

Pre-Approval vs Full Approval

Don't confuse pre-approval with final (unconditional) approval. Pre-approval is generic and property-agnostic, while full approval happens after you've signed a sale and purchase agreement. It includes property-specific checks like valuation, LIM report, title search, and building inspection.

| Aspect | Pre-Approval | Full Approval |

|---|---|---|

| Timing | Before house hunting | After offer accepted |

| Property Check | None | Valuation, LIM, title |

| Validity | 60-90 days | Leads to settlement |

| Guarantee | Conditional | Unconditional |

Why Get Mortgage Pre-Approval in NZ?

In our fast-moving market, pre-approval makes you a stronger buyer. Sellers and agents prioritise offers from pre-approved buyers because they know finance is verified, reducing the risk of deals falling over. It's especially crucial for first-home buyers competing in hotspots like Wellington or Queenstown.

- Shop with certainty: Know your budget upfront—no surprises.

- Boost your negotiating power: Offers stand out in multi-offer situations.

- Save time: Avoid viewing unaffordable homes.

- Lock in rates: Get a rate hold (often 60-90 days) amid interest rate fluctuations.

For Kiwi first-home buyers, it's a game-changer alongside schemes like Kāinga Ora First Home Loan, which may require pre-approval eligibility checks.

Who Needs Pre-Approval?

Anyone serious about buying in New Zealand—first-home buyers, families upsizing, investors, or migrants with resident visas. Even if you're using KiwiSaver withdrawals or First Home Grants, pre-approval confirms your numbers stack up under 2026 lending rules, including loan-to-value (LVR) restrictions.

It's not mandatory by law, but real estate pros strongly recommend it. Without it, your offer might be overlooked in a hot auction.

How to Get Mortgage Pre-Approval: Step-by-Step

Getting pre-approved in NZ takes just 3-5 working days if you're prepared. Here's the practical process:

Step 1: Check Your Readiness

Assess your finances. Aim for a 20% deposit to avoid LVR speed bumps (low-deposit lending is tighter post-2021 rules). Use online calculators from banks like BNZ or ASB, but a mortgage adviser gives personalised advice.

Step 2: Choose Your Path—Bank or Broker?

Go direct to a bank like SBS Bank for a simple chat (book via 0800 727 2265 or branch), or use a broker for multiple lender options. Brokers like those at Lenda or Haven access better rates and save time.

Step 3: Gather Documents

Lenders need a full picture. Have these ready:

- Proof of identity: Passport, driver's licence, or proof of NZ citizenship/permanent residency.

- Income proof: 3 months' payslips (PAYE), 2 years' tax returns (self-employed), or financials.

- Bank statements: 3 months from all accounts, showing spending habits.

- Deposit evidence: Savings statements, KiwiSaver balance, or gift letters.

- Debts: Credit card limits, loans (car, student, personal).

- Expenses breakdown: Power, food, subscriptions (compared to HEM benchmarks).

- Other: Employment contract, government subsidies (WINZ, ACC confirmation if applicable).

"Complete, organized documentation speeds things up—PAYE employees with clean credit often get approved fastest."

Step 4: Submit and Wait

Your adviser or bank assesses income stability, debt-to-income ratio, credit score, and stress tests for rate rises. Expect questions on your finances.

Step 5: Receive Your Letter

If approved, get a letter detailing loan amount, property price cap, deposit needed, terms, and conditions (e.g., property valuation). Validity: 60-90 days—start hunting!

How Long Does It Take?

Typically 3-5 working days for lender review, plus 1-3 days gathering docs—total 4-6 days. Speed it up with:

- Organised files.

- Stable PAYE job.

- Experienced broker.

- Clean credit.

Costs and Conditions to Watch

Pre-approval is usually free, but full approval may involve valuation fees ($800-$1,200) or legal costs. Common conditions: no financial changes, acceptable property (freehold, no issues), KiwiSaver confirmation.

In 2026, watch LVR rules: <20% deposit needs lender approval; first-home buyers can access low-deposit options via Kāinga Ora.

Practical Tips for Kiwis

- Clean up finances: Pay down debts, reduce spending 3 months pre-application.

- Boost deposit: Max KiwiSaver, use First Home Grant (up to $10k singles).

- Get advice: Free from advisers registered with NZ Mortgage Brokers Association.

- House hunt smart: Focus on your pre-approval limits; get a builder's report early.

- Renew early: If expiring, reapply—rates may have dropped.

Next Steps to Your New Home

Ready? Gather your docs today, book a free broker chat or bank meeting, and secure your pre-approval. With NZ's market heating up in 2026, don't delay—start house hunting stronger. Visit Kāinga Ora for first-home help or your bank's site for calculators. You've got this!

Frequently Asked Questions

Sources & References

-

1

How to Get Pre-Approved for a Mortgage NZ 2025 | First Home Buyers — insights.luminate.co.nz

-

2

Understanding mortgage pre-approval: why it's important and how to get it — lendalmortgages.co.nz

-

3

Gaining pre-approval | Guide to home buying - SBS Bank — www.sbsbank.co.nz

- 4

-

5

5 Things First Home Buyers Can Do to Buy in 2026 — www.thefirsthomebuyersclub.co.nz

-

6

Demystifying the home loan application process - BNZ — www.bnz.co.nz

-

7

From application to keys: What to expect from the mortgage process — mortgagelink.co.nz

Useful Tools

Related Articles

Using the NZ Mortgage Calculator to Plan Your House Hunt

Imagine spotting your dream home in Auckland or Christchurch, but wondering if you can actually afford it. That's where the NZ Mortgage Calculator comes in—your essential tool for turning house-huntin...

Mortgage Refixing Guide: How to Negotiate the Best Rate with Your Bank

Imagine slashing hundreds of dollars off your weekly mortgage payments just by knowing when and how to refix. With interest rates easing in 2026, thousands of Kiwis are facing refix decisions that cou...

Mortgage Refinancing: When Does It Make Sense?

Imagine shaving thousands off your mortgage interest while unlocking cash for that home reno or debt consolidation you've been dreaming about. For Kiwis with home loans, mortgage refinancing can be a...

How to Pay Off Your Mortgage Faster (NZ Strategies)

Imagine owning your home outright years earlier than planned, freeing up thousands in interest payments and giving you financial freedom sooner. For Kiwis with mortgages, paying off your home loan fas...