First Home Grant NZ: How to Get Up to $10000

Buying your first home is one of the biggest financial decisions you'll make, and the New Zealand government wants to help. The First Home Grant puts up to $10,000 directly towards your deposit, makin...

James writes about the New Zealand property market, renting, home ownership, and housing costs. He breaks down complex property topics into practical advice for renters and buyers.

Buying your first home is one of the biggest financial decisions you'll make, and the New Zealand government wants to help. The First Home Grant puts up to $10,000 directly towards your deposit, making homeownership more achievable for eligible Kiwis. Whether you're saving hard or wondering if you qualify, this guide breaks down exactly what you need to know to access this valuable support.

What Is the First Home Grant?

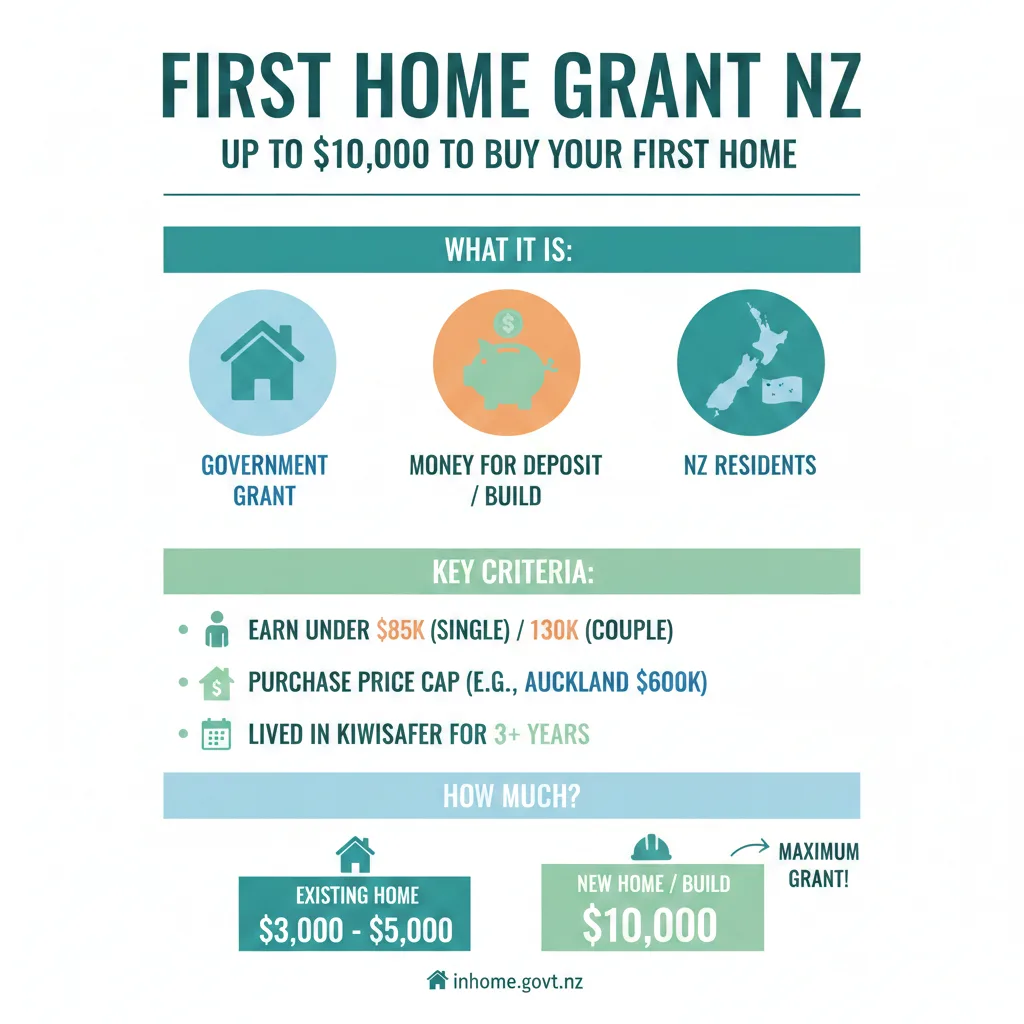

The First Home Grant is a government initiative that provides eligible first-home buyers with up to $10,000 to put towards their deposit. Unlike a loan, this is a grant—you don't need to repay it. It's designed to help Kiwis who are saving hard but struggling to accumulate the deposit needed to enter the property market.

The grant works alongside your KiwiSaver savings and can be combined with other government support like the First Home Loan, which allows you to purchase with just a 5% deposit instead of the typical 20%.

Am I Eligible for the First Home Grant?

Before you get excited about that $10,000, you'll need to meet several eligibility criteria. The good news is that if you're serious about saving and haven't owned a home before, you're likely in the running.

Key Eligibility Requirements

To qualify for the First Home Grant, you must:

- Be over 18 years old

- Be a first-home buyer—meaning you don't currently own any property or land (ownership of Māori land doesn't count against you)

- Have never received the First Home Grant or its predecessor, the KiwiSaver deposit subsidy

- Be a member of a KiwiSaver scheme, complying fund, or exempt employer scheme

- Have contributed at least the minimum amount (currently 3% of your income) to KiwiSaver for at least three years—these don't need to be consecutive

- Have earned within the income limits in the last 12 months

- Have a deposit of at least 10% of the purchase price

- Purchase a property within your region's house price caps

- Agree to live in the property for at least six months

Income Limits

Your income is a crucial factor. The limits are generous enough to help working Kiwis but designed to target those who need support most:

- Single buyer, no dependants: $95,000 or less (before tax) in the last 12 months

- Single buyer with one or more dependants: $150,000 or less (before tax) in the last 12 months

- Two or more buyers: $150,000 or less combined (before tax) in the last 12 months

If you've had a pay rise that pushed you slightly over these limits, don't assume you're ineligible. Kāinga Ora assesses your total earnings over the full 12 months, so a recent increase might not disqualify you.

KiwiSaver Requirements

You must have been contributing to a KiwiSaver scheme for at least three years. The key points:

- Your contributions must be at least the minimum allowable percentage (3% of your income)

- The three years don't need to be consecutive—they just need to add up to three years' worth of contributions

- If you've contributed to a different superannuation scheme, you can call 0508 935 266 to check if you're eligible

How Much Can You Get?

The First Home Grant provides up to $10,000 towards your deposit. The exact amount depends on factors like the purchase price of your home and your specific circumstances. This money is applied directly to your deposit, reducing the amount you need to save yourself.

If you're purchasing a Fletcher Living property, you may also qualify for an additional $10,000 from Fletcher Living (applied when you settle), though this is a separate offer with its own eligibility criteria.

How to Apply for the First Home Grant

The application process is straightforward, and you have two options depending on where you are in your home-buying journey.

Step 1: Check Your Eligibility

Before applying, make sure you meet all the criteria listed above. You'll need to gather documents that prove your eligibility, including:

- Proof of your KiwiSaver membership and contribution history

- Evidence of your income for the last 12 months (payslips, tax returns, or employment letters)

- Identification to confirm you're over 18

- Details of any property you've owned previously (if applicable)

Step 2: Apply Through Kāinga Ora

You can apply for the First Home Grant in two ways:

- Pre-approval: Apply before you've found a property. This gives you certainty about your eligibility and how much you might qualify for, which is useful when you're house hunting.

- Grant approval: Apply once you've found a property and have a signed sale and purchase agreement.

Applications are made through Kāinga Ora – Homes and Communities, the government agency that administers the scheme.

Step 3: Meet Regional House Price Caps

Your property must fall within the regional house price caps set by the government. These vary by location, so check with Kāinga Ora to confirm your target property qualifies.

First Home Grant vs. First Home Loan: What's the Difference?

You might hear about both the First Home Grant and the First Home Loan. They're different support mechanisms, and you may be eligible for one, both, or neither.

First Home Grant: Up to $10,000 towards your deposit. Requires KiwiSaver membership and three years of contributions.

First Home Loan: Allows you to borrow with just a 5% deposit instead of the typical 20%. You must be a New Zealand citizen, permanent resident, or resident visa holder ordinarily resident in New Zealand, with income limits similar to the First Home Grant. You don't need KiwiSaver for this loan.

Many first-home buyers use both: the grant tops up their deposit, and the First Home Loan helps them borrow with a smaller deposit requirement.

Tips for Maximising Your First Home Grant

Start Contributing to KiwiSaver Early

If you're not yet at the three-year mark, start contributing now. Even small regular contributions add up, and you'll be eligible sooner than you think.

Keep Your Income Below the Threshold

If you're close to the income limit, be strategic about timing. Remember that the assessment is based on your total earnings over 12 months, so a recent pay rise doesn't necessarily disqualify you.

Combine Support Schemes

Use the First Home Grant alongside your KiwiSaver first-home withdrawal and the First Home Loan to minimise the deposit you need to save personally.

Explore Regional Variations

House price caps vary by region. If you're flexible about location, you might find more affordable properties in regions with higher caps, stretching your budget further.

Frequently Asked Questions

Can I use the First Home Grant if I've owned property before?

No. The First Home Grant is exclusively for first-time home buyers. If you've owned property in the past, even if you no longer own it, you're not eligible.

What if I exceed the income limit by a small amount?

Kāinga Ora assesses your total income over the full 12 months before you apply. If you've recently received a pay rise that pushed you over the limit, you might still be eligible depending on your average earnings across the year. Contact Kāinga Ora to discuss your specific situation.

Do the three years of KiwiSaver contributions need to be consecutive?

No. The three years don't need to be consecutive—they just need to add up to three years' worth of contributions. So if you've had breaks in your contributions, as long as the total adds up to three years, you're eligible.

Can I apply for the grant before I've found a property?

Yes. You can apply for pre-approval before you start house hunting. This gives you clarity on your eligibility and how much you might qualify for, which is helpful when you're making offers.

What if I'm part of a couple—does the income limit apply to both of us combined?

Yes. If you're applying as two or more buyers, your combined income must be $150,000 or less (before tax) in the last 12 months.

Can I use the First Home Grant with the First Home Loan?

Yes. Many first-home buyers combine both schemes. The grant provides up to $10,000 towards your deposit, and the First Home Loan allows you to borrow with just a 5% deposit.

Your Next Steps

If you're serious about buying your first home, the First Home Grant could be the boost you need. Here's what to do next:

- Check your KiwiSaver balance and contribution history to confirm you've been contributing for three years.

- Review your income for the last 12 months to ensure you're within the limits.

- Visit the Kāinga Ora website to learn more and start the application process.

- Consider applying for pre-approval to get clarity on your eligibility before you start house hunting.

- Combine the grant with the First Home Loan to maximise your borrowing power and minimise your personal deposit.

Homeownership in Aotearoa is within reach, and the First Home Grant is designed to help you get there. With up to $10,000 towards your deposit, combined with smart saving and the right support, you can turn that dream of owning your own home into reality.

Related Articles

Why 2026 is the Hardest Year to Buy a Home (and How to Beat the Odds)

Imagine standing at the edge of the property ladder in 2026, eyeing your dream home while prices hover stubbornly high, listings pile up, and buyer confidence wavers. For Kiwis, this year feels toughe...

Buying Your First Home in 2026: A Step-by-Step NZ Checklist

Imagine standing in your own Kiwi bach or cosy family home, keys in hand, after years of renting. In 2026, with interest rates stabilising and first-home schemes still strong, buying your first home i...

Selling Your Home? 10 Low-Cost Renovations That Add $50k in Value

If you're planning to sell your home in New Zealand, you don't need to break the bank with a complete renovation to attract buyers and boost your sale price. The good news? Some of the most effective...

Tiny Homes in NZ: Legal Hurdles and Living Realities

Imagine downsizing your life into a cosy 70-square-metre haven on your own section, free from the hassle of building consents and council red tape. For Kiwis grappling with sky-high housing costs, tin...