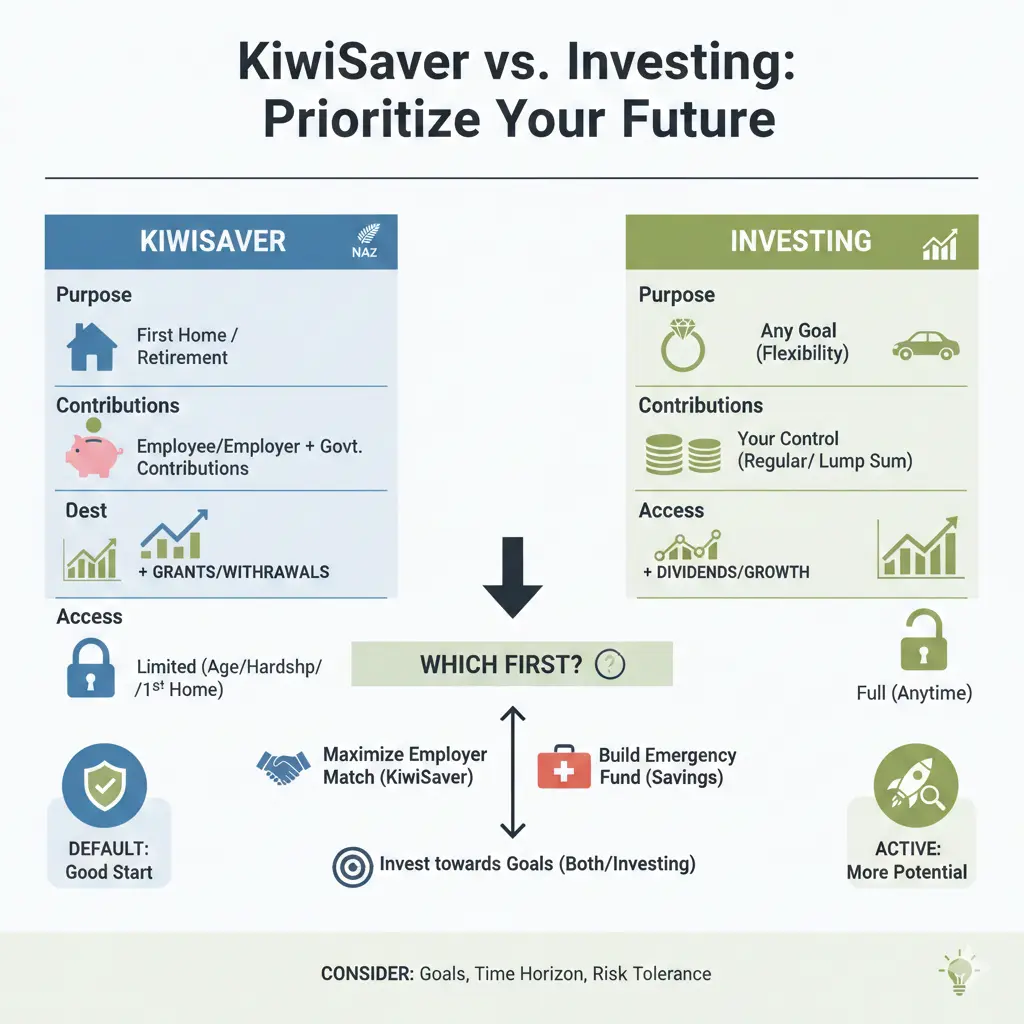

KiwiSaver vs. Investing: Which Should You Prioritize?

Imagine doubling your money every payday without lifting a finger—that's the magic of KiwiSaver's employer match. But what if you could access your cash sooner or chase higher returns through shares o...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

KiwiSaver vs Investing: Which Should You Prioritise?

Imagine doubling your money every payday without lifting a finger—that's the magic of KiwiSaver's employer match. But what if you could access your cash sooner or chase higher returns through shares or property? For Kiwis building wealth in 2026, deciding between KiwiSaver and other investments boils down to your goals, timeline, and risk appetite. Let's break it down so you can make a smart choice.

What is KiwiSaver and Why Does It Matter in 2026?

KiwiSaver is New Zealand's voluntary retirement savings scheme, perfect for anyone with a job. You choose to contribute 3%, 4%, 6%, 8%, or 10% of your pay, and your employer must match at least 3% if you do the same—effectively doubling your input. The government chips in up to $260.72 annually (25 cents per dollar you contribute, down from $521.43), but only if you earn under $180,000 and meet eligibility rules.

Big Changes Coming in 2026

From 1 April 2026, minimum contributions rise to 3.5% for both you and your employer, boosting your savings automatically. This ramps up to 4% by April 2028. Now, 16- and 17-year-olds qualify for employer contributions, and the government match extends to them too. If cash is tight, apply to Inland Revenue from February 2026 for a temporary drop back to 3% for up to 12 months—no hardship proof needed.

Your funds grow tax-free via multi-rate PIE (Portfolio Investment Entity) rules, and you pick funds like conservative, balanced, or growth. Recent performance shows high growth funds delivering 11.34% over 2025, driven by US tech stocks. No upfront cash required—just a paycheck.

Other Investment Options for Kiwis in 2026

Beyond KiwiSaver, New Zealanders love property, shares, and more. Each offers unique perks, but often demands your own capital and carries liquidity risks.

Property: The Kiwi Classic

Housing has been a star, with national average prices up 55.1% from 2015-2025 ($556,931 to $863,747). Leverage via mortgages amplifies returns, but it's a double-edged sword—downturns hurt hard. Unlike KiwiSaver, you can rent it out for income, but expect maintenance, tenants, and interest rate swings. In 2026, a generational shift sees boomers selling rentals, potentially flooding the market.

Shares and Managed Funds

Shares via NZX, ASX, or international markets shone in 2025: Korea +85%, Hong Kong/Taiwan +30%, Australia +10% pa over three years, while NZ lagged at 3%. Funds like PIE Funds eye AI, energy transition, and healthcare for 2026 gains. You can start small via platforms like Sharesies or Hatch, with no lock-in. Self-employed? This beats KiwiSaver's limited employer match.

Other Popular Picks

- Term Deposits: Safe, with Cash Funds returning 0.23% monthly amid falling rates.

- ETFs: Low-fee global exposure, often outperforming property long-term.

- P2P Lending or Digital Assets: Higher risk, higher reward—emerging as Kiwis diversify.

KiwiSaver vs Investing: Head-to-Head Comparison

Here's how they stack up for everyday Kiwis.

| Factor | KiwiSaver | Other Investing (e.g., Shares/Property) |

|---|---|---|

| Accessibility | Auto-enrol from age 18; no upfront cash needed. | Requires your money; platforms make shares easy. |

| Contributions | Employer match 3.5%+ from Apr 2026; govt top-up. | 100% your funds; no matches. |

| Liquidity | Locked till 65 (first home exception). | Flexible—sell shares anytime, property slower. |

| Returns (Recent) | High Growth: 11.34% (2025), 9.74% pa 5yr. | Property +55% decade; shares vary wildly. |

| Risk | Diversified funds; market volatility. | Leverage amps property risk; shares volatile. |

| Taxes | PIR rates (10.5-28%); growth tax-free. | Income/capital gains taxed; bright-line for property. |

KiwiSaver wins for hands-off retirement building, especially with matches. Direct investing suits shorter goals or higher risk tolerance.

Pros and Cons: Making Sense of Your Options

KiwiSaver Advantages

- Free money from employer/govt—maximise by hitting 3.5%+.

- Professional management; switch funds easily (e.g., to growth for 9.74% 5yr returns).

- First Home Withdrawal for deposits.

- Locked in—emergencies mean hardship applications.

- Lower govt top-up in 2026; ineligible over $180k.

- Self-employed get less match value.

- Liquidity and control—cash out for opportunities.

- Potential outperformance: KiwiSaver growth funds may beat property.

- Diversify into 2026 trends like AI.

- No matches; all your risk.

- Time-intensive; property leverage risky.

- Taxes bite harder without PIE shelter.

- Audit your KiwiSaver: Check fund, contributions via provider app. Switch to growth if young.

- Boost contributions: Aim 6-10% for max govt $260.72.

- Diversify: $100/month into shares via low-fee ETF.

- Seek advice: Free from Financial Mentors or adviser.

- Track 2026: Watch AI, bonds amid rate cuts.

KiwiSaver Drawbacks

Direct Investing Advantages

Direct Investing Drawbacks

Which Should You Prioritise? It Depends on You

Max out KiwiSaver first—grab that employer match—then invest extra elsewhere. Under 40? Growth KiwiSaver plus shares for balance. Nearing retirement? Shift conservative. Self-employed or high-earner? Direct investing shines. Run numbers via Sorted.org.nz's calculator. Review annually: 2025's 11.34% high growth beat NZ shares' 3%.

Practical Tips for Kiwis

Your Next Steps to Build Wealth

Log into KiwiSaver today—bump to 3.5%+ from April, pick a growth fund. Stash extra into a shares account. Use Kiwisaver.govt.nz for providers, IRD for changes. Chat a financial adviser for personalised plan. In 2026, blending both sets you up for retirement and beyond—start small, stay consistent.

Frequently Asked Questions

Sources & References

-

1

Top 8 Best Investments in New Zealand (2026) | Opes Partners — www.opespartners.co.nz

-

2

KiwiSaver Scheme Investment Update - January 2026 - SBS Wealth — www.sbswealth.co.nz

-

3

Key KiwiSaver changes you need to know for 2026 — www.generatewealth.co.nz

- 4

-

5

Stocks, Inflation & Kiwisaver w Greg Smith of Generate - YouTube — www.youtube.com

-

6

What To Expect In 2026: Stocks, Inflation & Kiwisaver w Greg Smith — podcasts.apple.com

-

7

Investing: six things to watch in 2026 - Pie Funds — www.piefunds.co.nz