How Much Does It Cost to Buy a House in Auckland?

Buying a house in Auckland remains one of the biggest financial decisions most Kiwis will ever make, especially with house prices Auckland 2025 still navigating a post-peak landscape. Whether you're a...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Buying a house in Auckland remains one of the biggest financial decisions most Kiwis will ever make, especially with house prices Auckland 2025 still navigating a post-peak landscape. Whether you're a first-home buyer eyeing the dream family home or an investor weighing up returns, understanding the true cost—from median prices to hidden extras—helps you plan smarter in 2026.

We've crunched the latest data from banks, REINZ, and government sources to break it down. Auckland's market has cooled from its 2021 frenzy but shows signs of stabilisation, with forecasts pointing to modest growth ahead. Let's dive into what it really costs to buy here now, suburb by suburb, and how to budget effectively.

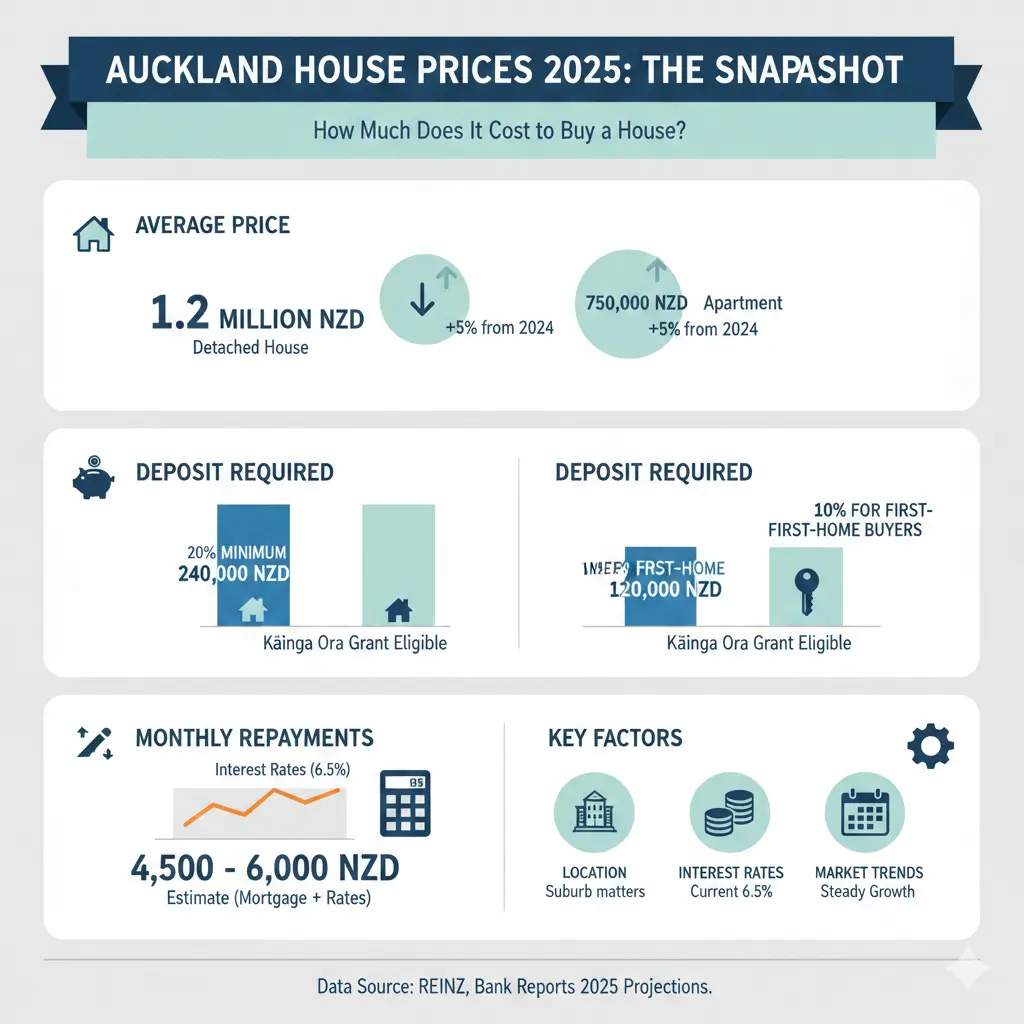

Auckland House Prices in 2025: The Current Snapshot

Auckland's median house price has levelled out after sharp corrections from the 2021 peak, creating a more balanced buyer's market. While national headlines grab attention, Auckland tells its own story: prices remain below those dizzying highs, but well-located homes in good school zones continue to attract keen buyers.

Median Prices Across Auckland

Recent REINZ data shows Auckland's median sale price hovering in the mid-$1 million range, though this varies wildly by suburb. For context:

- Central Auckland (e.g., Ponsonby, Grey Lynn): Often $1.5M+, where demand from professionals keeps values firm despite the broader dip.

- East Auckland (e.g., Howick, Pakuranga): Around $1.2M median, popular with families for schools and space.

- West Auckland (e.g., Henderson, Massey): More affordable at $900K–$1M, appealing to first-home buyers.

- South Auckland (e.g., Papakura, Otara): Entry-level options from $800K, though growth has been slower here.

Standalone houses have corrected more sharply than townhouses, which sit 9–10% below peak—still a gentler fall. Inventory is at a 10-year high, giving buyers more choice and putting downward pressure on overpriced listings.

Regional Comparisons: Why Auckland Lags

Auckland isn't alone in its caution—Wellington has seen sharper drops of 13–15% from peak—but contrasts with rising prices in Canterbury, Otago, and Southland. Auckland sentiment is improving, with 73% of locals expecting growth, though affordability and jobs temper optimism.

| Region | 2025 Trend | Key Driver |

|---|---|---|

| Auckland | Flat to modest recovery (mid-teens % from trough) | High inventory, cautious lending |

| Wellington | Down 4% (6 months), 13–15% from peak | Employment uncertainty |

| Canterbury | Modest gains | Balanced supply/demand |

This two-speed market means Auckland buyers might find relative value now, before any snap-back.

House Price Forecasts for Auckland 2026

Looking ahead, economists predict subdued growth for house prices Auckland 2025 into 2026, with ANZ slashing its forecast to 2% nationally amid looming rate hikes. The median bank prediction sits at 3.8%, while BNZ eyes 4% and the Reserve Bank 3.75%.

Factors Shaping 2026 Prices

- Interest Rates: OCR at 2.25% in late 2025 has eased mortgage rates from peaks, but test rates keep lending tight.

- Supply and Demand: High housing stock favours buyers early 2026, though new builds could ease pressure later.

- Economy: Unemployment above 5% softens momentum, per the Phillips Curve trade-off.

- Migration and Jobs: Steady inflows support demand, especially for family homes.

For an $800K Auckland property, 3.8% growth adds about $30K by year-end—solid but no boom. Suburb-level insights matter most: quality homes in supply-scarce areas could outperform.

Breaking Down the Full Cost to Buy a House in Auckland

The headline price is just the start. Here's a realistic budget for a $1M median Auckland home in 2026.

Upfront Costs Beyond the Price Tag

| Cost Item | Estimated Amount ($1M Purchase) | Notes |

|---|---|---|

| Deposit (20% min for investors) | $200,000 | First-home buyers can go lower via KiwiSaver/First Home Grant. |

| Legal Fees & Searches | $2,500–$4,000 | Includes LIM, project info memo. |

| Building/Lim Inspection | $800–$1,500 | Essential—skipping risks big surprises. |

| Bank Legal Fees | $1,000 | Standard for mortgage setup. |

| Valuation Fee | $800–$1,200 | Bank-required. |

| Moving Costs | $2,000–$5,000 | Depends on distance/furniture. |

Total extras: 1–2% of purchase price, or $10K–$20K. First-home buyers, check Kāinga Ora for grants up to $10K on existing homes.

Ongoing Ownership Costs

Rates, insurance, and maintenance add up fast—Auckland City Council rates average $3K–$5K/year for a median home, up amid cost pressures. Factor in:

- Insurance: $2K–$4K annually, rising with rebuild costs.

- Maintenance: 1% of value/year ($10K for $1M home).

- Council Rates: Vary by suburb—use Auckland Council calculator.

Financing Your Auckland Home: Loans and Affordability

Mortgage rates have eased to around 5–6% fixed, but debt-to-income (DTI) rules from mid-2025 cap borrowing at 6x income. For a couple earning $150K combined:

- Max borrow: ~$900K (plus $200K deposit for $1.1M home).

- Weekly repayments: $800–$900 on $800K loan @5.5% (30 years).

Practical tip: Use the Reserve Bank mortgage calculator and get pre-approval from lenders like ASB or Kiwibank. First-home buyers, maximise KiwiSaver withdrawals—up to $200K/person with partner match.

Practical Tips for Buying in Auckland's 2026 Market

- Research Suburbs Deeply: Use REINZ suburb reports and OneRoof for sold prices—avoid medians alone.

- Get Inspections Always: Auckland's older stock (pre-2000) often hides issues like weathertightness.

- Time Your Move: Spring sees more listings; early 2026 could offer buyer leverage.

- Leverage Government Help: First Home Loan via Kāinga Ora for low deposits (5%).

- Negotiate Smart: With days on market up, offer 5–10% below asking on overpriced homes.

- Build Your Team: Lawyer, mortgage broker, and buyer's agent for auctions.

Avoid townhouses if chasing growth—they lag standalone homes long-term.

Next Steps to Buy Your Auckland Home

Start by calculating your borrowing power on the Reserve Bank's site, then view 5–10 properties in target suburbs. Engage a buyer's agent for insider tips, and track weekly REINZ updates. With forecasts modest, prioritise lifestyle and location over chasing peaks. Chat to a mortgage broker today—affordability is improving, making 2026 a pragmatic entry point for many Kiwis.

Frequently Asked Questions

Sources & References

-

1

ANZ slashes 2026 house price forecast as rate hikes loom — www.mpamag.com

-

2

NZ's biggest bank downgrades house price forecast - 1News — www.1news.co.nz

-

3

New Zealand House Prices 2026: What the Numbers Actually Say — www.najibrealestate.co.nz

-

4

House Price Predictions 2026 & 2027 - MoneyHub NZ — www.moneyhub.co.nz

-

5

Auckland Property Market 2026: Simple Guide for Auckland Home Sellers — pricemyproperty.co.nz

-

6

House Price Predictions (2026): What to Expect in NZ | Opes Partners — www.opespartners.co.nz

-

7

What will happen to house prices in 2026? | RNZ News — www.rnz.co.nz

Related Articles

How Much Does It Cost to Buy a House in Wellington?

Wellington's property market is at a crossroads in 2026. House prices have softened from their pandemic peaks, inventory levels are at their highest in a decade, and public sector uncertainty continue...

How Much Does It Cost to Buy a House in Christchurch?

Thinking about buying a house in Christchurch? You're not alone—many Kiwis are eyeing the Garden City as house prices Christchurch 2025 data shows steady growth into 2026, making it an attractive spot...

Property Prices by Region: Where Can You Afford in NZ?

Ever wondered if that dream home is within reach, or if it's time to look beyond the big smoke? With New Zealand's property market stabilising in 2026, affordability varies wildly by region—some spots...