How Much Does It Cost to Buy a House in Wellington?

Wellington's property market is at a crossroads in 2026. House prices have softened from their pandemic peaks, inventory levels are at their highest in a decade, and public sector uncertainty continue...

James writes about the New Zealand property market, renting, home ownership, and housing costs. He breaks down complex property topics into practical advice for renters and buyers.

Wellington's property market is at a crossroads in 2026. House prices have softened from their pandemic peaks, inventory levels are at their highest in a decade, and public sector uncertainty continues to weigh on buyer confidence. But beneath those headlines sits a more nuanced story—one where location, property type, and timing matter more than ever. If you're thinking about buying a home in Wellington, understanding where prices actually sit right now is the first step to making a smart decision.

What's the Current Median House Price in Wellington?

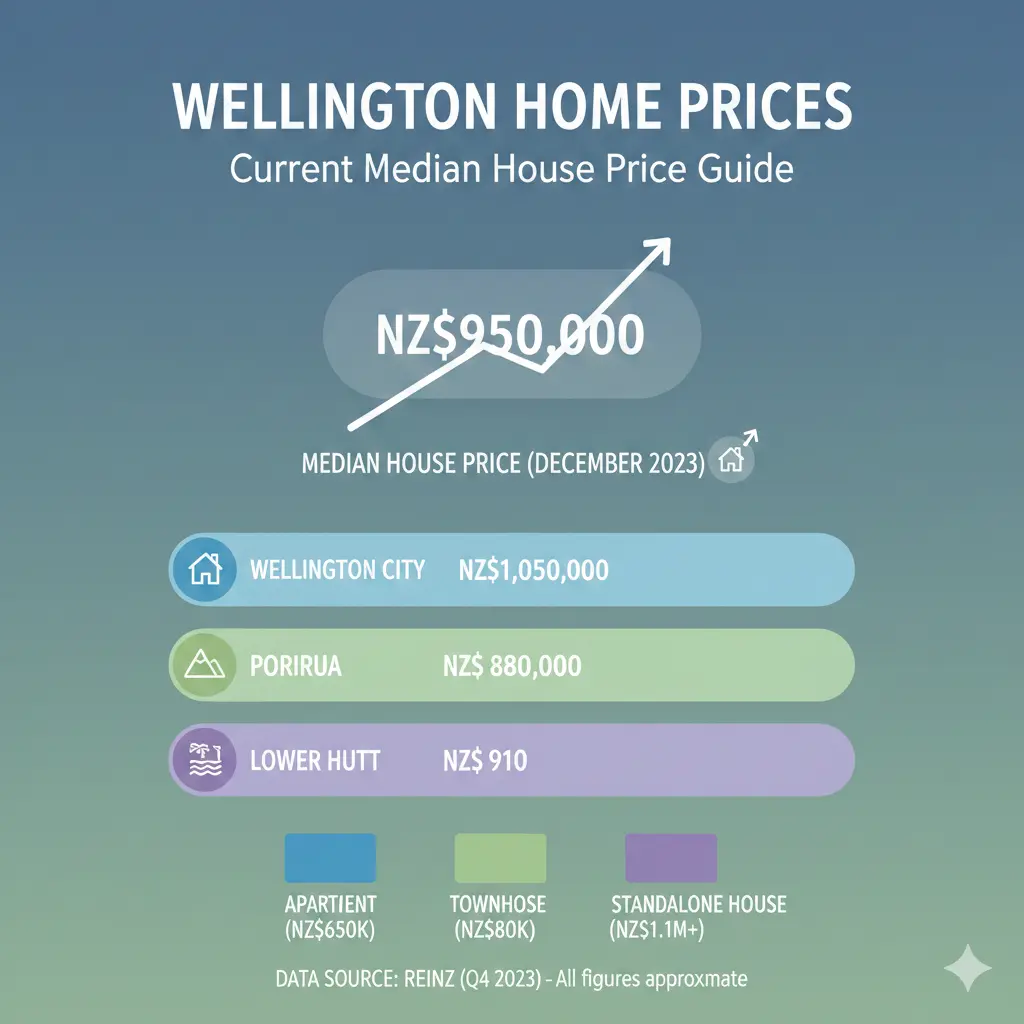

The headline figures can be confusing because Wellington's market moves differently depending on which metric you look at. The Wellington Region median sale price sits around $790,000, while Wellington City's average value is $915,492. Both numbers tell you something useful, but neither tells you the whole story.

Here's why the difference matters: the regional median includes suburbs further out (like Porirua and the Hutt Valley), which tend to be more affordable. Wellington City's average is higher because it captures the central suburbs where demand—and prices—remain stronger. Over the past three months, Wellington City property prices have moved up just 0.22%, which reflects the market's cautious mood.

If you're looking at specific suburbs, prices vary dramatically. Seatoun is the most expensive suburb with an average value of $1,661,600, while Wellington Central is the most affordable at $414,350. That $1.2 million spread shows you why suburb-by-suburb research matters far more than any single "Wellington average."

How Much Have Wellington House Prices Fallen?

Wellington's median price is down 3.5% to $767,500 year on year, and the broader picture is even more sobering for some property types. Both townhouses and standalone homes remain 13–15% below their 2022 peaks, reflecting weaker demand and employment uncertainty in the region.

Nationally, prices are up 1.1% year on year, but Wellington is moving in the opposite direction. QV data shows Wellington prices are now 3.6% lower than a year ago. For owners who bought during the pandemic boom, that's a painful reality check. But for buyers entering the market now, it means better negotiating power and more choice.

The public sector job losses and restructuring have hit Wellington harder than other regions. People are leaving the city—students, workers, families—which means fewer buyers competing for homes and more stock sitting on the market. That imbalance is the primary driver keeping prices under pressure.

Why Is Wellington's Market Different Right Now?

Wellington isn't behaving like the rest of New Zealand, and understanding why is crucial if you're buying or selling here.

The Inventory Problem

Wellington has logged 23 consecutive months of year-on-year inventory growth, meaning there are more homes for sale than buyers looking to purchase. Time to sell has stretched to 46 days, up five days from the same time last year. That's a buyer's advantage—you can be selective, negotiate harder, and wait for the right property rather than rushing into a bidding war.

Public Sector Uncertainty

Wellington's economy is disproportionately dependent on government employment. The public sector restructuring over the past couple of years has created job losses and uncertainty that ripple through the entire market. People delay buying decisions when they're unsure about their employment, and some relocate entirely. This headwind is unique to Wellington and doesn't affect Auckland or Christchurch to the same degree.

Falling Interest Rates (A Bright Spot)

The Reserve Bank cut the Official Cash Rate to 2.25% in November 2025, which has eased mortgage pressure heading into 2026. One-year mortgage specials are sitting around the mid-4% range, making borrowing cheaper than it was in 2024. This is supporting demand, even if it's not driving rapid price growth.

Rental Market Softening

Rents in Wellington have fallen 7–10% as landlords try to fill vacancies. The average rent is $595 per week, down from higher levels a year ago. While this is tough for landlords, it means renters have more breathing room and can negotiate better deals.

What's Driving the "Two-Speed" Market?

Wellington isn't one market—it's multiple micro-markets reacting to different pressures. Premium, scarce stock in desirable suburbs can still perform reasonably well. But compromised properties, townhouses in oversupplied pockets, or homes in areas hit hardest by public sector job losses face real downward pressure.

The result is a market where location, condition, and timing matter far more than they did during the boom years. A well-positioned three-bedroom home in a sought-after suburb might attract multiple offers. A tired two-bedroom townhouse in a saturated development might sit for months.

What's the Outlook for Wellington House Prices in 2026?

Most credible forecasts point to modest growth or sideways movement rather than a rapid rebound. Bank economists are predicting 2–5% house price growth for 2026 nationally, but Wellington is likely to lag that. The base case for Wellington is flat to low single-digit gains.

The factors that could change this outlook are:

- Faster rate relief: If the Reserve Bank cuts rates more aggressively, affordability improves and demand could lift.

- Public sector confidence: If employment uncertainty eases and people stop leaving Wellington, demand will strengthen.

- Listing absorption: If the excess stock gets absorbed faster than expected, it could support prices.

- Unemployment fears: If the broader economy weakens and unemployment rises, Wellington could dip further given its exposure to public sector employment.

How to Find a Realistic Price Range for Your Home

Don't rely on medians alone. Here's what serious buyers and sellers do:

- Look at recently sold comparables in your suburb. Find homes similar to yours (same number of bedrooms, similar condition, similar location) that sold in the past 4–8 weeks. What did they actually sell for?

- Check the REINZ regional median as a direction-of-travel marker. It tells you if the market is moving up or down, but it's not a price guide for your specific home.

- Use QV's average values for your suburb. This gives you a valuation-based trend line and helps you spot if your suburb is moving faster or slower than the broader market.

- Pay attention to inventory and time-to-sell. If homes in your suburb are sitting for 60+ days, you've got buyer leverage. If they're selling in 20 days, you need to price competitively.

- Get a professional valuation. A registered valuer can give you a defensible price range based on comparable sales, property condition, and market conditions.

Key Takeaways for Buyers

If you're buying in Wellington right now, you're in a buyer's market. You have choice, negotiating power, and falling interest rates on your side. Use that advantage:

- Don't rush. With 46+ days to sell and high inventory, the right property will still be there next month.

- Get pre-approved for a mortgage so you can move quickly when you find the right home.

- Factor in subject-to-sale offers. Many Wellington buyers need to sell their current home first, so be prepared for longer settlement timelines.

- Look beyond the headline price. Consider what condition and location will mean for your long-term satisfaction and resale value.

- Watch for insurance constraints. Wellington's earthquake risk and insurance costs are higher than other regions—factor this into your budget.

Key Takeaways for Sellers

If you're selling, the market is more challenging than it was two years ago. But it's not impossible:

- Price realistically based on recent comparables, not on what you paid or what you think your home "should" be worth.

- Invest in presentation. With buyers having more choice, a well-presented home stands out.

- Be flexible on settlement timelines. Accepting a subject-to-sale offer might get you a better price than waiting for a cash buyer.

- Consider your suburb carefully. Some Wellington suburbs are moving faster than others—understand where you sit in that spectrum.

What to Do Next

If you're thinking about buying or selling a home in Wellington, start with the basics: understand your suburb's recent comparable sales, get a professional valuation, and check your mortgage pre-approval. Wellington in 2026 rewards the prepared. The market isn't frantic, but it is selective. The homes that sell well are the ones priced right, presented well, and marketed to the right audience.

Don't get caught up in national headlines or long-term predictions. Focus on the fundamentals: comparable sales, your budget, and what you actually need from a home. Wellington's market is softer than it was, but that softness creates opportunity for buyers who do their homework.

Frequently Asked Questions

Sources & References

-

1

Wellington house price 2026: Trends, sold evidence, suburb shifts — pricemyproperty.co.nz

-

2

Wellington City House Prices [2025] | Property Market — www.opespartners.co.nz

-

3

Wellington property market update — Outlook for 2026 — www.squirrel.co.nz

-

4

House prices are up - but what's going on in Wellington? — www.rnz.co.nz

-

5

New Zealand House Prices 2026: What the Numbers Actually Say — www.najibrealestate.co.nz

-

6

House Price Predictions 2026 & 2027 — www.moneyhub.co.nz

Related Articles

How Much Does It Cost to Buy a House in Auckland?

Buying a house in Auckland remains one of the biggest financial decisions most Kiwis will ever make, especially with house prices Auckland 2025 still navigating a post-peak landscape. Whether you're a...

How Much Does It Cost to Buy a House in Christchurch?

Thinking about buying a house in Christchurch? You're not alone—many Kiwis are eyeing the Garden City as house prices Christchurch 2025 data shows steady growth into 2026, making it an attractive spot...

Property Prices by Region: Where Can You Afford in NZ?

Ever wondered if that dream home is within reach, or if it's time to look beyond the big smoke? With New Zealand's property market stabilising in 2026, affordability varies wildly by region—some spots...