Complete Guide to KiwiSaver: A Beginner's Roadmap

Ever wondered if your KiwiSaver is quietly building the retirement you've always dreamed of, or if it's just sitting there gathering dust? For most Kiwis, it's the cornerstone of our nest egg, but wit...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Ever wondered if your KiwiSaver is quietly building the retirement you've always dreamed of, or if it's just sitting there gathering dust? For most Kiwis, it's the cornerstone of our nest egg, but with changes kicking in this year, now's the perfect time to get clued up and make it work harder for you.

Whether you're just starting out, switching jobs, or eyeing that first home, this KiwiSaver guide NZ breaks it all down simply. We'll cover the basics, the big 2026 updates, and practical steps to supercharge your savings—all tailored for everyday New Zealanders.

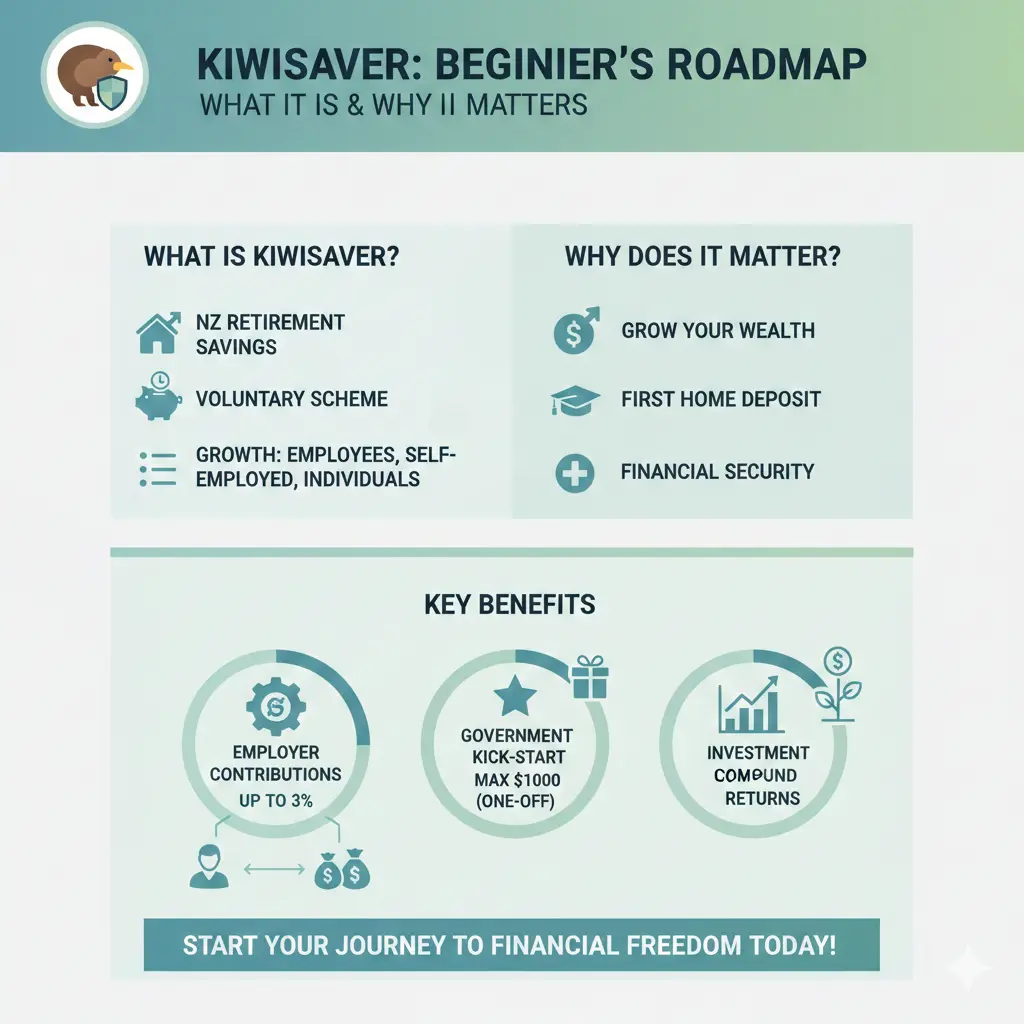

What is KiwiSaver and Why Does It Matter?

KiwiSaver is our voluntary, government-backed savings scheme designed to help us build a solid retirement fund. Launched in 2007, it's grown into a powerhouse with over 3 million members, holding billions in assets. It's not just for retirement though—you can withdraw for a first home or after financial hardship.

Here's why it's a game-changer:

- Three-way contributions: You put in money from your pay, your employer matches (at least the minimum), and the government chips in too.

- Tax advantages: Contributions are from before-tax pay, and investments grow tax-free inside the scheme (taxed at your PIR—Prescribed Investor Rate).

- Locked in for growth: Funds stay invested until age 65, letting compound interest do the heavy lifting over decades.

For a young Kiwi earning $60,000 a year contributing 3%, that's about $1,800 yearly from you, matched by your employer, plus government top-ups—potentially snowballing to hundreds of thousands by retirement.

Who Can Join KiwiSaver?

Most New Zealanders qualify. You can join if you're:

- A NZ citizen or entitled to live here indefinitely.

- Aged 18 or over (16-17-year-olds from April 2026 if employed).

- Living or normally living in NZ.

Even if you're self-employed, under 16, or not working, you can still join through Inland Revenue (IR). New employees under 65 are auto-enrolled, with an opt-out window of 8 weeks.

Special Cases: Self-Employed and Overseas Kiwis

Self-employed? Set up direct debits via your provider. Aussies or Brits moving here? Transfer your super or pension into KiwiSaver for seamless growth—providers like Compound Wealth specialise in this.

How KiwiSaver Contributions Work in 2026

Contributions come straight from your gross pay (before tax), making it painless. You pick your rate, employer matches the minimum, and it's all automatic.

Key Rates and the Big 2026 Change

From 1 April 2026, the default rate jumps from 3% to 3.5% for both you and your employer. It rises again to 4% in April 2028.

| Contribution Option | Your Rate (% of gross pay) | Employer Minimum Match |

|---|---|---|

| Default (pre-April 2026) | 3% | 3% |

| Default from 1 April 2026 | 3.5% | 3.5% |

| Common choices | 4%, 6%, 8%, 10% | 3% (or more if they offer) |

Can't swing the increase? Apply for a temporary rate reduction from 1 February 2026 via IR—stay at 3% for 3-12 months without proving hardship. Your employer might match or stick to 3.5%.

Government Contributions: What's New?

The government adds 25c per $1 you contribute (down from 50c), up to $260.72 max yearly (July-June). Max it out by contributing $1,042.86 yourself. No contribution if you earn over $180,000, but 16-17-year-olds now qualify.

"The increase to 3.5% KiwiSaver contributions from April 2026 is a positive step toward stronger retirement savings for many New Zealanders."Generate Wealth

Choosing the Right KiwiSaver Fund

Your fund choice is crucial—it's where your money gets invested. Providers offer options from safe cash to high-growth aggressive funds. Match it to your age, risk tolerance, and goals.

Fund Types Explained

- Cash/Conservative: Low risk, low returns (2-4% pa)—good for near-retirement.

- Balanced: Mix of shares, bonds—medium risk/return (4-7%).

- Growth/Aggressive: Heavy on shares/property—higher returns (6-10%+ historically), but volatile.

Many schemes auto-adjust (lifecycle funds) to get conservative as you near 65. Check fees too—aim under 0.5% pa.

Top Providers and Advice

Compare via Sorted's Fund Finder. Standouts include ANZ, Compound Wealth (for custom plans), and National Capital for impartial advice.

Withdrawals and Exceptions

KiwiSaver locks funds until 65, but exceptions apply:

- First Home: Save 3+ years, withdraw with $5,000+ balance (plus govt top-up).

- Hardship: Serious illness, bankruptcy—apply via IR.

- Over 65: Full withdrawal as lump sum, regular payments, or mix.

Check IR's KiwiSaver page for forms.

Practical Tips to Maximise Your KiwiSaver in 2026

Don't leave it on autopilot—here's how to level up:

- Review now: Log into your myIR account or provider app. Bump to 6% if affordable—employer matches minimum only.

- Switch providers: Free once yearly; pick low-fee, high-return funds.

- Track performance: Use FMA's KiwiSaver dashboard.

- Salary sacrifice: Voluntarily increase via payroll for tax perks.

- Get advice: Free from providers or call Sorted (0800 367 673).

For 2026, act before April: confirm your rate, apply for reduction if needed, and choose growth funds if young.

Next Steps for Your KiwiSaver Journey

Grab your coffee, log into myIR today, and spend 10 minutes reviewing your settings. With the 3.5% default hitting in April, tweak your rate, fund, and provider to match your goals. Chat to a Sorted adviser or your provider—they're there to help us everyday Kiwis retire comfortably.

Small actions now compound into big wins later. Here's to a stronger financial future—kiwi-style.

Frequently Asked Questions

Related Articles

KiwiSaver 2026: Which Fund is Actually Winning the Performance Race?

If you're tracking your KiwiSaver fund performance in 2026, you might be surprised to learn that the winners aren't always the biggest banks – and the rankings keep shifting. The latest investment sur...

PIR Rates Explained: Are You Paying Too Much Tax on Your KiwiSaver?

Ever checked your KiwiSaver statement and wondered why the tax on your returns seems off? You're not alone—many Kiwis are paying too much (or too little) on their KiwiSaver earnings because of an inco...

KiwiSaver vs Other Investments: Where Should Your Money Go?

Ever wondered if your hard-earned cash is working as hard as it could in KiwiSaver, or if there's a better spot for it elsewhere? With house prices cooling and shares hitting new highs, many Kiwis are...

Best KiwiSaver Providers in NZ 2025: Complete Comparison

Choosing the right KiwiSaver provider can supercharge your retirement savings or first home deposit, especially with government contributions and employer matches adding free money to your account. In...