Living Overseas with KiwiSaver: Repayment Rules Explained

Imagine packing up your life in Aotearoa for an exciting adventure abroad—maybe chasing job opportunities in London, family ties in the UK, or a fresh start in Canada. But what happens to your hard-ea...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine packing up your life in Aotearoa for an exciting adventure abroad—maybe chasing job opportunities in London, family ties in the UK, or a fresh start in Canada. But what happens to your hard-earned KiwiSaver nest egg? For many Kiwis dreaming of living overseas, understanding the KiwiSaver overseas rules is crucial to avoid nasty surprises. Whether you're emigrating permanently or just testing the waters, these rules dictate when and how you can access your savings, with special twists for Aussies down under.

This guide breaks it all down with the latest 2026 info, straight from Inland Revenue and trusted providers. We'll cover withdrawal timelines, what you can take, Australia-specific quirks, and practical steps to keep your retirement on track—no matter where you roam.

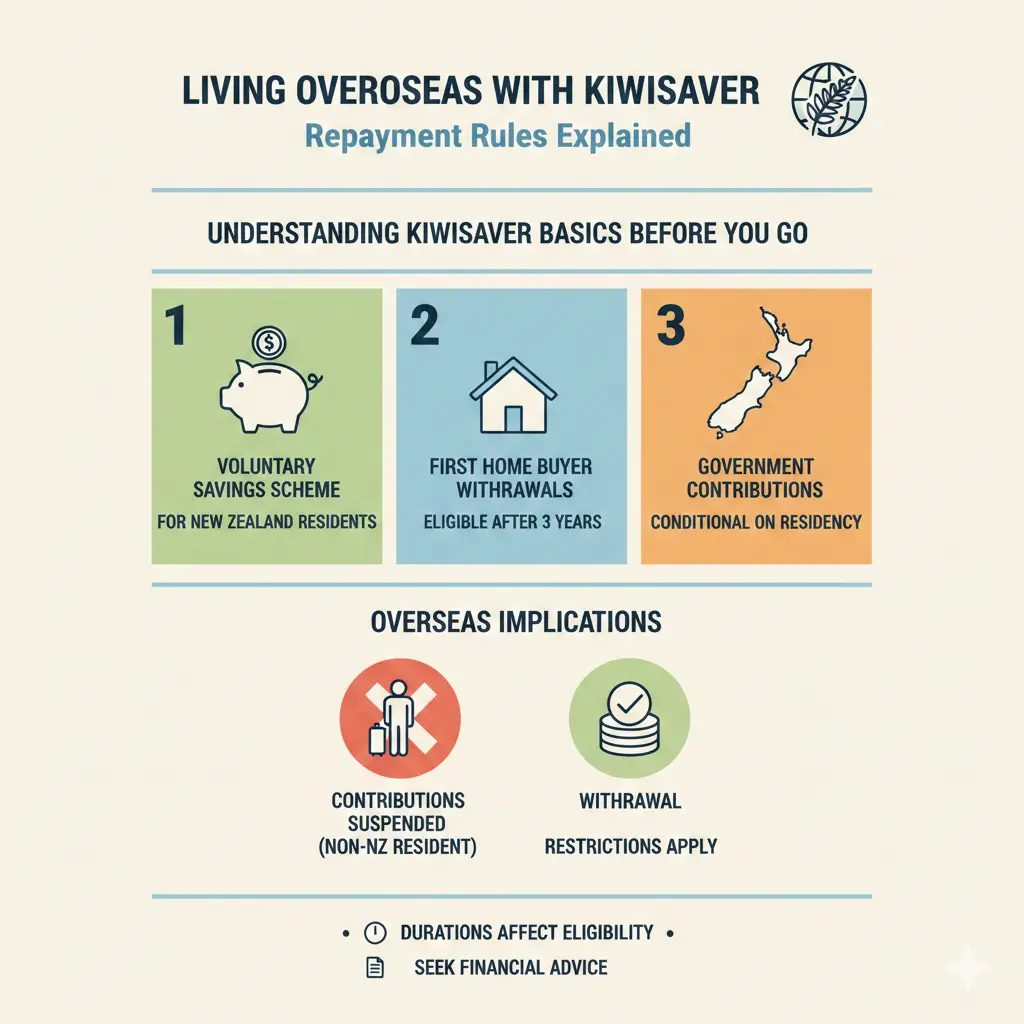

Understanding KiwiSaver Basics Before You Go

KiwiSaver is New Zealand's voluntary retirement savings scheme, where you, your employer, and the government chip in to grow your funds tax-free until retirement. But heading overseas triggers specific KiwiSaver overseas rules under the KiwiSaver Act 2006. Normally, you can't touch your money until age 65 (or for first homes/hardship), but permanent migration changes that—after a waiting period.

Key 2026 updates affect everyone: From 1 April 2026, default contribution rates bump up to 3.5% for both employees and employers (from 3%), with options to stick at 3% temporarily if needed. If you're 16-17, you'll finally qualify for employer contributions too. These shifts mean planning ahead is smarter than ever, especially if you're contributing from abroad.

Contributions While Overseas

- You can keep contributing voluntarily if you want—many providers allow it via direct debit.

- Government contributions (up to $260.72/year for $1,042.86+ personal input) require you to mainly live in NZ, but exceptions apply for State Services employees or approved volunteers overseas.

- Employers won't contribute unless you're on a Kiwi payroll, so expect solo funding abroad.

Pro tip: Before leaving, chat with your provider about pausing or adjusting contributions to match your new reality.

Moving to Australia: Special Transfer Rules

Australia gets VIP treatment thanks to the close ties—think shared super schemes. If you're relocating permanently across the ditch, you cannot withdraw your KiwiSaver early like other destinations. Instead:

- Transfer to an Australian superannuation scheme: Optional, but seamless. Your provider handles it, subject to caps and Aussie rules (with some Kiwi exceptions). No tax hit on transfer, but future growth follows Australian laws.

- Leave it in KiwiSaver: Fine too—no forced move. You'll access at 65, but likely miss government contributions unless you're a qualifying government worker.

Example: Sarah, a Kiwi nurse moving to Sydney, transferred her $50,000 KiwiSaver to her new employer's super fund. She kept growing it under Aussie rules, planning to retire beachside Down Under.

"If you change KiwiSaver to an Australian superannuation scheme, you will generally be subject to Australian superannuation laws, with a few exceptions."

Check the Australian Taxation Office for transfer limits—they're complex and evolve.

Moving Anywhere Else: Withdrawal After 12 Months

For destinations like the UK, USA, Europe, or Asia, the rules loosen up—but not immediately. After living overseas (not Australia) for 1 full year, you can withdraw most of your savings early.

What You Can Withdraw

| Withdrawable | Not Withdrawable |

|---|---|

| Your contributions | Government contributions (e.g., annual $521.43 max) |

| Employer's contributions | - |

| $1,000 kick-start (if received) | - |

| Fee subsidies | - |

| Earned interest/growth | - |

Apply via your provider's online portal—prove your overseas residency with a statutory declaration or utility bills. Funds arrive tax-free, but plan for that first-year funding gap (no access during it).

Alternative: Transfer to an approved foreign super scheme under KiwiSaver Act Section 228(e). It must meet strict regs—your provider checks eligibility.

Real Kiwi Example

Take Mike, who moved to Canada in 2024. After 12 months, he withdrew $80,000 (minus gov contributions), using it for a house deposit in Vancouver. He left $5,000 behind to keep options open.

Tax Implications and 2026 Changes

Withdrawals are generally tax-free as lump sums, but growth was already taxed at your PIR (Prescribed Investor Rate). From 1 April 2026, transferring overseas pensions back to NZ schemes lets the scheme handle tax—handy if you return.

No major tax shifts for outbound KiwiSaver in 2026, but always confirm your PIR with IRD. Overseas income might affect future eligibility too.

Practical Steps: What to Do Before, During, and After Moving

Don't wing it—follow this checklist for smooth sailing:

- Pre-departure (3-6 months out): Notify your KiwiSaver provider of plans. Review fund performance—switch to cash if markets are volatile during your wait year.

- Prove permanent move: Get an IRD emigration certificate or overseas address proof ready.

- Fund year 1: Save 12+ months' expenses—KiwiSaver won't help immediately.

- Application time: After 12 months, log in, fill forms, and wait 2-4 weeks for payout.

- Return to NZ? You can rejoin KiwiSaver, but withdrawn funds don't go back—withdrawals are final.

- Get advice: Free KiwiSaver health checks from providers like National Capital ensure you're optimised.

For Australia movers: Weigh transfer vs. leaving it—run numbers with both providers.

Common Pitfalls and How to Avoid Them

- Forgetting the 12-month clock: Starts from your NZ departure—holidays don't count.

- Gov contributions trap: They stay locked till 65, even on withdrawal.

- Aussie misconceptions: No cash-out option—don't bank on it.

- Market dips: Time withdrawals wisely; consider low-risk funds during transition.

Frequently Asked Questions

Related Articles

KiwiSaver 2026: Which Fund is Actually Winning the Performance Race?

If you're tracking your KiwiSaver fund performance in 2026, you might be surprised to learn that the winners aren't always the biggest banks – and the rankings keep shifting. The latest investment sur...

PIR Rates Explained: Are You Paying Too Much Tax on Your KiwiSaver?

Ever checked your KiwiSaver statement and wondered why the tax on your returns seems off? You're not alone—many Kiwis are paying too much (or too little) on their KiwiSaver earnings because of an inco...

KiwiSaver vs Other Investments: Where Should Your Money Go?

Ever wondered if your hard-earned cash is working as hard as it could in KiwiSaver, or if there's a better spot for it elsewhere? With house prices cooling and shares hitting new highs, many Kiwis are...

Best KiwiSaver Providers in NZ 2025: Complete Comparison

Choosing the right KiwiSaver provider can supercharge your retirement savings or first home deposit, especially with government contributions and employer matches adding free money to your account. In...