Self-Employed? Your KiwiSaver Options Explained

Running your own business in New Zealand gives you freedom, but when it comes to retirement savings, self-employed Kiwis face a different path with KiwiSaver. Unlike employees who get employer contrib...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Running your own business in New Zealand gives you freedom, but when it comes to retirement savings, self-employed Kiwis face a different path with KiwiSaver. Unlike employees who get employer contributions automatically, you're in the driver's seat—making it crucial to understand your options to build a solid nest egg.

With KiwiSaver contribution rates set to rise to 3.5% from 1 April 2026, now's the time to review your strategy. Whether you're a freelancer, sole trader, or contractor, this guide breaks down how KiwiSaver works for the self-employed, from joining to maximising government perks. We'll cover practical steps tailored for NZ's 2026 landscape so you can save smarter for retirement.

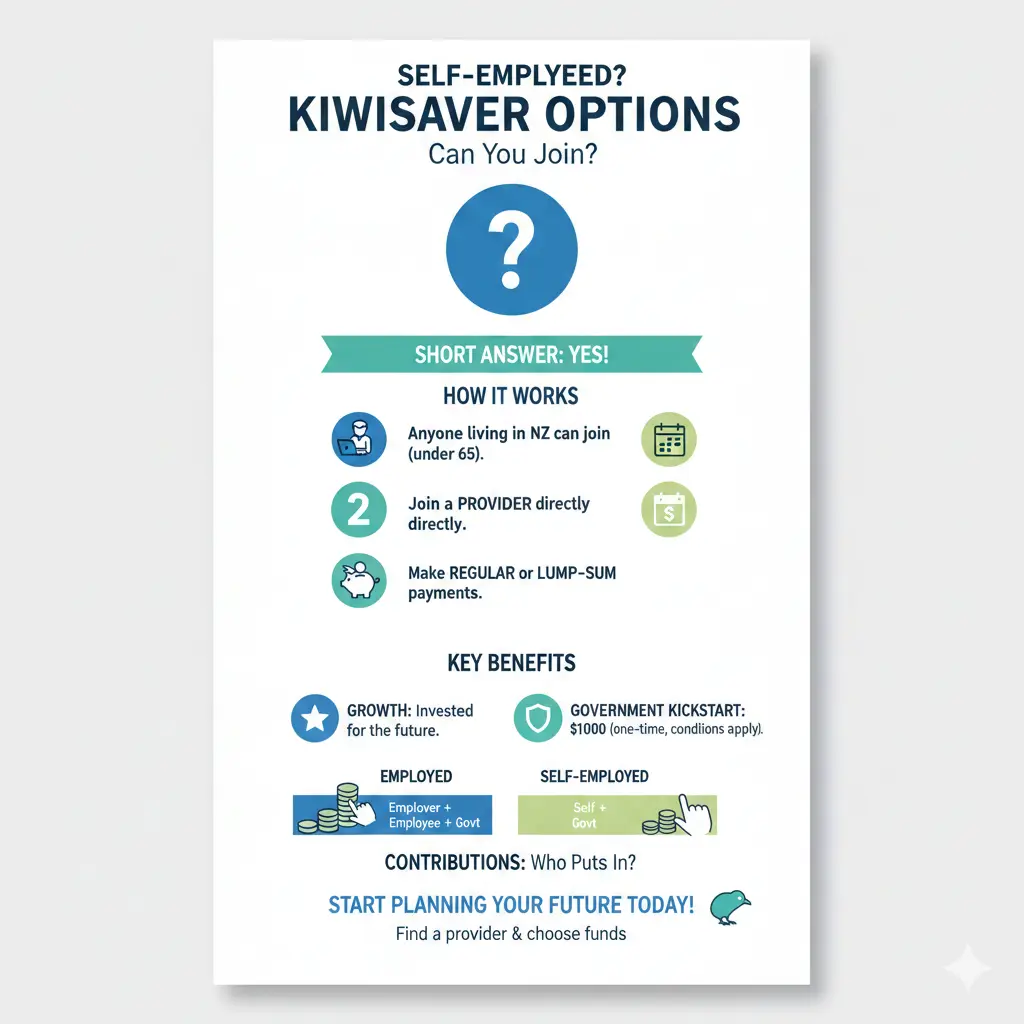

Can Self-Employed Kiwis Join KiwiSaver?

Absolutely—self-employed people can join KiwiSaver voluntarily, just like employees. You don't need PAYE income or an employer to participate. In fact, individuals of all ages can join, though eligibility for certain benefits like government contributions has age limits (16-65).

If you're already in KiwiSaver and switch from self-employed to employee, simply tell your new employer. They'll start deducting your contributions (3%, 4%, 6%, 8%, or 10% of before-tax pay) and add their matching contribution—minimum 3% until the 2026 increase.

Who Qualifies as Self-Employed for KiwiSaver?

- Freelancers and contractors without formal employment.

- Sole traders running a business under their own name.

- Anyone not receiving regular PAYE wages, but earning income through invoices or self-managed payments.

No minimum income threshold applies to join, but to unlock the full government contribution, you'll need to contribute at least $1,042.86 annually (more on this below).

How Do Contributions Work for the Self-Employed?

As a self-employed Kiwi, you're responsible for all contributions—no employer match means you fund it yourself from business or personal income. Pay directly to your provider or via IRD using the 'Pay tax' option in internet banking or automatic payments.

Contribution rates mirror employee options: 3% (rising to 3.5% default from April 2026), 4%, 6%, 8%, or 10% of your gross income equivalent. Change rates anytime by contacting your provider—flexibility is key for fluctuating self-employed earnings.

Upcoming 2026 Changes: What Self-Employed Need to Know

From 1 April 2026, the default rate jumps to 3.5% for both employees and employers, with a further rise to 4% by April 2028. Self-employed aren't forced into the default, but if basing contributions on income, plan for this shift. Apply for a temporary rate reduction by 1 February 2026 if 3.5% strains your cashflow.

Also, 16- and 17-year-olds qualify for contributions from this date, broadening access.

Unlock Free Money: The Government Contribution

One of the best perks for self-employed Kiwis is the annual government contribution—up to $260.72 if you contribute $1,042.86 or more by 30 June each year. That's a instant 25% return, regardless of no employer match.

Contribute less? You still get 25 cents per dollar, capped at $260.72. Requirements:

- Age 16-65.

- Principal residence in NZ (some exceptions for government employees).

- Income under $180,000 (as of 2024 thresholds; check IRD for 2026 updates).

Example: A Wellington graphic designer contributing $20/week ($1,040/year) bags the full $260.72. Set up auto-payments to hit the threshold effortlessly.

"That’s as little as contributing around $20 a week into your KiwiSaver account!"

Choosing the Right KiwiSaver Provider and Fund

With over 40 providers, pick one with low fees and strong performance. Self-employed savers benefit from KiwiSaver's competitive fees compared to other managed funds. Use tools like Sorted.org.nz to compare.

Fund Options for Your Risk Profile

Select from conservative (low risk, steady growth) to growth funds (higher risk, bigger long-term returns). As self-employed, match to your timeline—e.g., aggressive if retirement's 20+ years away.

| Fund Type | Risk Level | Best For |

|---|---|---|

| Conservative | Low | Short-term savers or risk-averse |

| Balanced | Medium | Most self-employed (10-20 year horizon) |

| Growth | High | Long-term, higher returns sought |

Declare your correct Prescribed Investor Rate (PIR) and IRD number to avoid tax issues—default to 28% if wrong.

Practical Tips for Maximising KiwiSaver as Self-Employed

- Automate contributions: $20-25/week ensures government top-up without thinking.

- Track income fluctuations: Contribute lumpy sums post-big jobs to smooth savings.

- Leverage tax deductions: KiwiSaver contributions from pre-tax equivalent income are tax-efficient; consult an accountant for provisional tax integration.

- Review annually: Switch providers or funds via IRD if needed—free and easy.

- First Home Withdrawal: Eligible after 3 years; self-employed qualify if meeting criteria.

- Prepare for 2026 rate hike: Budget now; apply for reduction if cash-strapped.

Real NZ example: Auckland plumber sole trader Sarah sets aside 6% of invoices monthly. She hits the govvie contrib easily and projects $500k by 65 in a balanced fund (assuming 5% annual return).

Common Mistakes to Avoid

- Treating contributions as an "expense" not investment—bigger now means more later.

- Missing the $1,042.86 threshold—free $260.72 left on table.

- Ignoring PIR—leads to tax headaches.

- Not diversifying—stick to one fund type forever.

FAQ: KiwiSaver for Self-Employed NZ

Q: Do I get employer contributions as a contractor?

A: No, unless classified as an employee. Sole traders/freelancers don't qualify.

Q: What's the minimum I need to contribute for government money?

A: $1,042.86/year for max $260.72 (25% match). Pro-rata below that.

Q: How do 2026 changes affect me?

A: Default rises to 3.5%; optional for self-employed but plan your rate.

Q: Can I withdraw KiwiSaver while self-employed?

A: Generally locked until 65, except first home (after 3 years) or hardship.

Q: What if my income varies wildly?

A: No minimums—contribute irregularly. Use IRD payments for flexibility.

Q: Is KiwiSaver worth it without employer match?

A: Yes—govvie contrib, low fees, compound growth make it competitive.

Next Steps to Boost Your KiwiSaver Today

Don't leave retirement to chance. Log into myIR to check/join KiwiSaver, set up auto-payments for that $260.72 boost, and compare providers on Sorted.org.nz. Chat with a financial adviser via MoneyTalks (0800 345 123) for personalised advice. With rates changing soon, act before April 2026—your future self will thank you.

Sources & References

-

1

KiwiSaver changes — ird.govt.nz — www.ird.govt.nz

-

2

How KiwiSaver works — amp.co.nz — www.amp.co.nz

-

3

Joining KiwiSaver if I'm self-employed or not working — ird.govt.nz — www.ird.govt.nz

-

4

How KiwiSaver works and why it's worth joining — sorted.org.nz — sorted.org.nz

-

5

Joining KiwiSaver if you're self-employed — westpac.co.nz — www.westpac.co.nz

-

6

Freelancer's guide to KiwiSaver — hnry.co.nz — hnry.co.nz

-

7

KiwiSaver Contribution Rates Jump on 1 April 2026 in NZ — artbeat.org.nz — www.artbeat.org.nz

-

8

KiwiSaver Government Contribution — nzdfsavings.mil.nz — www.nzdfsavings.mil.nz

Related Articles

KiwiSaver 2026: Which Fund is Actually Winning the Performance Race?

If you're tracking your KiwiSaver fund performance in 2026, you might be surprised to learn that the winners aren't always the biggest banks – and the rankings keep shifting. The latest investment sur...

PIR Rates Explained: Are You Paying Too Much Tax on Your KiwiSaver?

Ever checked your KiwiSaver statement and wondered why the tax on your returns seems off? You're not alone—many Kiwis are paying too much (or too little) on their KiwiSaver earnings because of an inco...

KiwiSaver vs Other Investments: Where Should Your Money Go?

Ever wondered if your hard-earned cash is working as hard as it could in KiwiSaver, or if there's a better spot for it elsewhere? With house prices cooling and shares hitting new highs, many Kiwis are...

Best KiwiSaver Providers in NZ 2025: Complete Comparison

Choosing the right KiwiSaver provider can supercharge your retirement savings or first home deposit, especially with government contributions and employer matches adding free money to your account. In...