The Truth About NZ Superannuation: Will It Be There When You Retire?

Picture this: you're finally hitting 65, dreaming of lazy mornings with a flat white and adventures in the Coromandel, only to wonder if NZ Superannuation—the safety net we've all counted on—will actu...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Picture this: you're finally hitting 65, dreaming of lazy mornings with a flat white and adventures in the Coromandel, only to wonder if NZ Superannuation—the safety net we've all counted on—will actually be there when you need it. With an election year looming in 2026 and whispers of policy tweaks, many Kiwis are asking the big question: is our universal super system sustainable, or are we one budget away from uncertainty?

Don't worry—we've got the facts straight from official sources and recent updates. NZ Super remains a cornerstone of retirement planning, designed to provide basic income security for all eligible over-65s. But let's dive into the truth: what it pays, who's eligible, recent changes, and how to make sure you're set for the long haul.

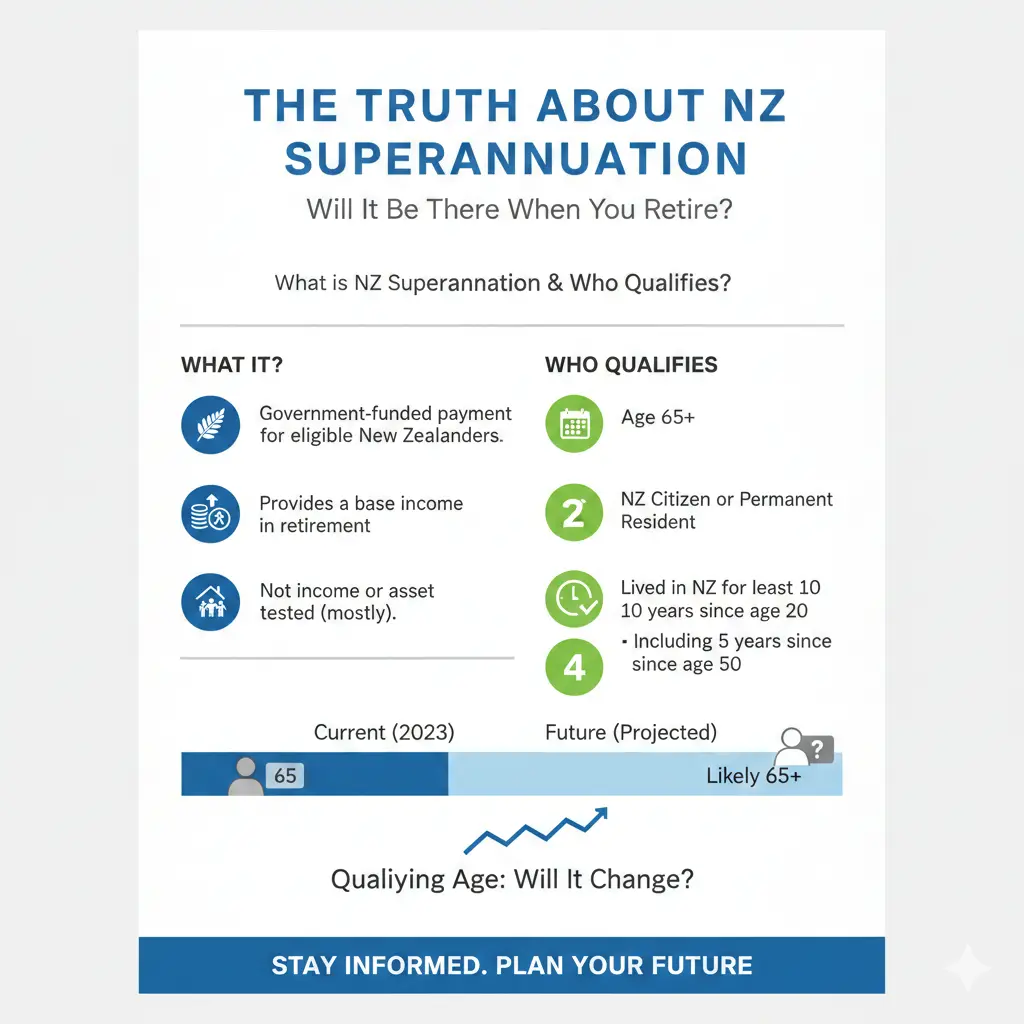

What is NZ Superannuation and Who Qualifies?

NZ Superannuation, often just called NZ Super, is a government-funded payment for New Zealand residents aged 65 and over. It's universal, meaning you don't need to have paid into it directly—it's funded through general taxation to ensure every eligible Kiwi gets a baseline retirement income.

To qualify, you must:

- Be 65 or older (the eligibility age stays at 65 for now, despite political debates).

- Meet residency criteria: generally 10 years in NZ since age 20, with 5 of those after 50. New residence rules kicked in from 1 July 2024 for those turning 65, tightening requirements slightly for recent arrivals.

- Live in NZ (with some exceptions for overseas travel or living in the Cook Islands, Niue, or Tokelau).

Important update: from 10 February 2026, rules refine residency duration for new applicants, overseas pension offsets, and documentation processes. These tweaks aim for clarity and sustainability amid our ageing population, but they won't cut existing payments.

Recent Changes You Need to Know About

The 2026 updates focus on administration rather than slashing benefits. Key shifts include:

- Stricter verification for overseas residency histories.

- Revised calculations for offsetting foreign pensions.

- Streamlined digital applications via MyMSD.

- Clearer rules on temporary travel abroad.

If you're already receiving NZ Super, your payments continue uninterrupted, and rates will rise automatically from February 2026—no reapplication needed. Always report changes like relationship status, address, or extra income to Work and Income to avoid reductions.

How Much Does NZ Super Pay in 2026?

Rates adjust annually on 1 April and sometimes mid-year. For the period 1 April 2025 to 31 March 2026 (with February 2026 uplifts), here's what eligible Kiwis receive gross (before tax), paid fortnightly every Tuesday.

| Situation | Weekly (gross) | Fortnightly (gross) | Annual (gross) | Annual after tax (tax code M, income up to $53,500) |

|---|---|---|---|---|

| Single, living alone or with dependent child | $627.14 | $1,254.28 | $32,611.28 | $27,994.53 ($538.36 weekly) |

| Single, living with non-partner | $576.80 | $1,153.60 | $29,993.60 | $25,876.82 ($497.63 weekly) |

| Couple, both qualify | $476.47 each | $952.94 each | $24,776.44 each | $21,656.14 each ($416.46 weekly each) |

| Couple, one qualifies | $476.47 (eligible only) | $952.94 (eligible only) | $24,776.44 (eligible only) | $21,656.14 ($416.46 weekly) |

These are for qualifying individuals. Tax matters: if NZ Super is your main income, use tax code 'M' for lower rates—e.g., a single living alone gets about $538 weekly after tax. Extra income (like KiwiSaver withdrawals or rentals) might bump you to 'SH' (30% rate), reducing your net payout.

Example: Retired teacher Sally and her husband draw $50k each from other sources. On 'SH', their fortnightly NZ Super drops to $667 each—$161 less weekly combined than on 'M'. Rates update again in April 2026, so check Work and Income for the latest.

Will NZ Super Be Sustainable When You Retire?

Here's the truth: yes, but with pressures. New Zealand's population is ageing—more over-65s, longer lifespans, fewer workers per retiree. By 2048, twice as many superannuitants could be renting, straining budgets assuming home ownership.

Politically, it's hot. National and ACT eye raising the age to 67 post-2044; New Zealand First vows to keep it at 65. With 2026 elections, expect debates on KiwiSaver hikes (to 6% by 2032) and maybe reintroducing income surtaxes on superannuitants scrapped in 1998.

Yet, governments affirm NZ Super's future: the 2023-2026 Statement of Intent commits to reviews for intergenerational fairness. No plans for means-testing—it's universal by design. Fiscal tweaks like the February 2026 changes ensure it endures without big cuts.

Challenges Ahead

- Demographics: Rising healthcare and pension costs.

- Housing: 40% of retirees rely solely on NZ Super; renters face shortfalls.

- Election Risks: Age hikes or contribution boosts could shift timelines.

The system's stable, but don't rely on it alone—40% do, but supplementing is smart.

Practical Tips to Maximise Your Retirement Income

NZ Super covers basics (about 90% of the after-tax pre-retirement wage for a couple), but you'll need more for travel, hobbies, or rising costs. Here's actionable advice:

- Boost KiwiSaver Early: Aim for 6% contributions. Employer matches help—rates rise from 2029.

- Check Eligibility Now: Use Work and Income's online checker if turning 65 soon. Apply via MyMSD up to 12 weeks early.

- Manage Tax: Stick to 'M' if possible; consult IRD for multi-income setups.

- Plan Housing: Downsizing or equity release eases burdens, especially with rents climbing.

- Explore Supplements: Accommodation Supplement, Winter Energy Payment if eligible via WINZ.

- Review Annually: Report changes promptly to lock in rates.

For personalised advice, chat with a certified financial adviser or use Retirement Commission's free tools.

Your Next Steps for a Secure Retirement

NZ Super will be there—universal, reliable, and adjusting for the future. But treat it as your floor, not your ceiling. Today, log into MyMSD to check eligibility, review your KiwiSaver balance, and model scenarios with extra income. Chat with WINZ or a adviser for tailored plans. With smart moves now, your retirement can be golden, not just gilded.

Frequently Asked Questions

Sources & References

-

1

NZ Superannuation Rules Change From 10 February 2026: Seniors Should Be Prepared — dirtdevildetailing.co.nz

-

2

New Zealand Superannuation Rates 2025 and 2026 — www.moneyhub.co.nz

-

3

How Much Is NZ Superannuation in 2025? [Explained] — www.opespartners.co.nz

-

4

Statement of Intent 2023-2026 — retirement.govt.nz

- 5

-

6

New Zealand Superannuation — www.workandincome.govt.nz

- 7

-

8

New Zealand Retirement Budget 2026: How Much NZ Super Pays and What Retirees Need to Know — korakospecklepark.co.nz

Related Articles

Pension Age and Residency Requirements for NZ Super

Planning your retirement in New Zealand means understanding the ins and outs of NZ Superannuation—it's the safety net many Kiwis rely on after 65. But with changing residency rules and specific age re...

Retirement Villages and Aged Care Options in NZ

Planning your retirement living in New Zealand doesn't have to feel overwhelming. Whether you're dreaming of low-maintenance villas with like-minded neighbours or need reliable aged care support, unde...