How Much Can You Borrow? NZ Mortgage Affordability Calculator

Ever wondered if that dream home in Auckland or a cosy cottage in Christchurch is within your reach? Figuring out your mortgage affordability NZ is the first step to turning house-hunting excitement i...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Ever wondered if that dream home in Auckland or a cosy cottage in Christchurch is within your reach? Figuring out your mortgage affordability NZ is the first step to turning house-hunting excitement into reality. With interest rates fluctuating and house prices holding steady in 2026, our guide breaks down exactly how much you can borrow, using trusted calculators and real Kiwi examples to keep it practical.

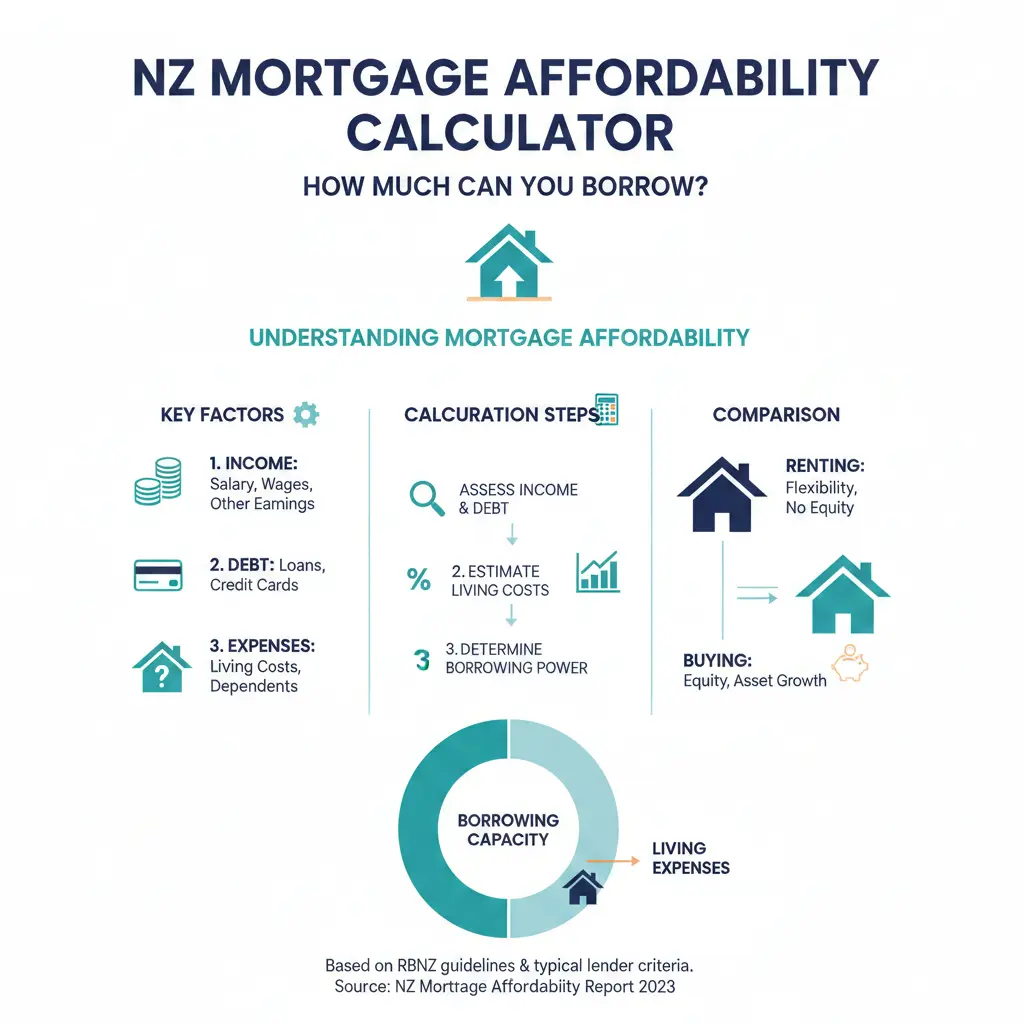

Understanding Mortgage Affordability in New Zealand

Mortgage affordability isn't just about your salary—it's a mix of income, expenses, deposit size, and current lending rules set by the Reserve Bank of New Zealand (RBNZ). Banks assess your ability to repay over the long term, often stress-testing at higher interest rates to ensure you're covered if rates rise.

In 2026, typical fixed mortgage rates hover around 5%, though they can vary by lender and term. First-home buyers face a minimum 15% deposit requirement, but many need 20% due to RBNZ debt-to-income (DTI) restrictions, which cap borrowing at about five times your gross annual income for owner-occupiers.

What Factors Determine How Much You Can Borrow?

- Income: Lenders consider all sources like salaries, bonuses, rental income, or dividends. Couples often qualify for more by combining incomes.

- Expenses: Everyday costs like groceries, utilities, and childcare count. Track these for three months to show your surplus.

- Existing Debts: Student loans, credit cards, or car repayments reduce your borrowing power.

- Interest Rates and Loan Term: Longer terms (e.g., 30 years) lower monthly repayments, boosting what you can borrow, but you'll pay more interest overall.

- Deposit: A bigger deposit means less to borrow and better rates. KiwiSaver withdrawals can help first-timers.

- Credit History: A clean record from CreditSafe or Equifax boosts approval chances.

The classic 28/36 rule still guides many lenders: housing costs shouldn't exceed 28% of your pre-tax income, and total debt no more than 36%. Recent data shows some new buyers stretching to 50% amid high prices, but banks are tightening up.

How to Use a Mortgage Affordability Calculator for NZ

Online mortgage affordability NZ calculators from banks like Westpac, ANZ, BNZ, and ASB give instant estimates tailored to Kiwi finances. They're free, secure, and factor in your real numbers—no obligation to apply.

Step-by-Step Guide to Calculating Your Borrowing Power

- Gather Your Numbers: List gross monthly income, after-tax take-home, rent or current housing costs, bills, and savings. Use a tax calculator for accuracy.

- Pick a Calculator: Try MoneyHub's tool, inputting max monthly repayment (e.g., if you save $500 after $1,000 rent on $5,000 income, aim for $1,500 mortgage).

- Enter Details: Add income, expenses, loan term (20-30 years), and interest rate (use 5-6% for stress-testing).

- Review Results: It might show a single earner on $80,000/year can borrow $450,000-$550,000 at 5% over 30 years, depending on expenses.

- Adjust and Compare: Tweak for fixed vs. floating rates or adding a partner.

For example, a couple earning $120,000 combined in Wellington, with $2,500 monthly expenses, could borrow around $700,000-$800,000 for a $900,000 home (20% deposit). Always get a pre-approval from a bank for the real figure.

NZ-Specific Tips for Accurate Results

- Factor in rates, insurance, and maintenance—about $300-500/month extra.

- Use Kāinga Ora tools if low-income; 5% deposits possible for first homes under schemes.

- Test at 7-8% rates to mimic RBNZ stress tests.

First-Home Buyers: Special Rules and Schemes

If you're buying your first home, you're in luck with Kiwi-specific help. RBNZ rules exempt first-home buyers from full DTI caps until mid-2026, but expect scrutiny. Aim for 15-20% deposits; for a $600,000 Auckland unit, that's $90,000-$120,000.

Kāinga Whenua and First Home Grants offer up to $10,000 for existing homes or new builds if you qualify (income under $95,000 single/$150,000 couple). Withdraw KiwiSaver tax-free for deposits after three years' contributions.

Investors need 40%+ deposits and face stricter DTI at 6x income.

Real-Life Examples: How Much Can You Borrow?

"We earned $100,000 combined, spent $3,000/month living, and borrowed $650,000 for our Hamilton home—calculators nailed it," shares a typical Kiwi couple via MoneyHub forums.

| Scenario | Combined Income | Monthly Expenses | Est. Borrow (5%, 30yrs) | Deposit Needed (20% on $800k home) |

|---|---|---|---|---|

| Single Professional | $80,000 | $2,500 | $450,000 | $70,000 |

| Couple, Auckland | $140,000 | $4,000 | $750,000 | $100,000 |

| Family, Regional | $160,000 | $5,000 | $900,000 | $120,000 |

These are indicative; regional prices vary—Auckland medians hit $1m, while Dunedin stays under $700k.

Common Pitfalls and How to Avoid Them

- Overlooking Hidden Costs: Budget 1-2% of home value yearly for maintenance.

- Ignoring Rate Changes: Fixed rates lock in peace; floating offers flexibility.

- No Pre-Approval: Shop multiple lenders via a broker for best rates.

- Student Loan Trap: Repayments kick in above $500/week—factor them.

Chat to a mortgage adviser registered with the Financial Markets Authority (FMA) for personalised advice.

Next Steps to Secure Your Mortgage

Plug your numbers into a mortgage affordability NZ calculator today—start with ANZ, Westpac, or MoneyHub. Track spending for a month, save aggressively for your deposit, and book a free broker consult. With rates stabilising in 2026, now's a great time to act. Get pre-approved, scour TradeMe Property, and step onto the property ladder confidently.

Frequently Asked Questions

Sources & References

-

1

How much can I borrow for a mortgage calculator - MoneyHub NZ — www.moneyhub.co.nz

-

2

How Much Can I Borrow Mortgage in NZ? Home Buyers Guide — fundmaster.co.nz

-

3

NZ Borrowing Power Calculator — mortgages.co.nz

-

4

Mortgage Borrowing Calculator — www.total.nz

-

5

Home loan affordability calculator | Westpac NZ — www.westpac.co.nz

-

6

Borrowing Calculator | How much can I borrow? | ANZ — tools.anz.co.nz

-

7

Home loan borrowing calculator - BNZ — www.bnz.co.nz

-

8

Find out how much of a mortgage you could get - Sorted — sorted.org.nz

-

9

Borrowing calculator - See how much you can borrow - ASB Bank — www.asb.co.nz

-

10

Mortgage Affordability Calculator - Finsol — www.finsol.co.nz