Student Loans Explained: How the NZ System Works

If you're heading to university, polytechnic, or another tertiary education provider in Aotearoa, you've probably heard about student loans. They're one of the main ways Kiwis fund their studies, but...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

If you're heading to university, polytechnic, or another tertiary education provider in Aotearoa, you've probably heard about student loans. They're one of the main ways Kiwis fund their studies, but understanding how they actually work can feel overwhelming. This guide breaks down everything you need to know about New Zealand's Student Loan Scheme—from what you can borrow and who's eligible, to how interest works and what repayment looks like once you're earning.

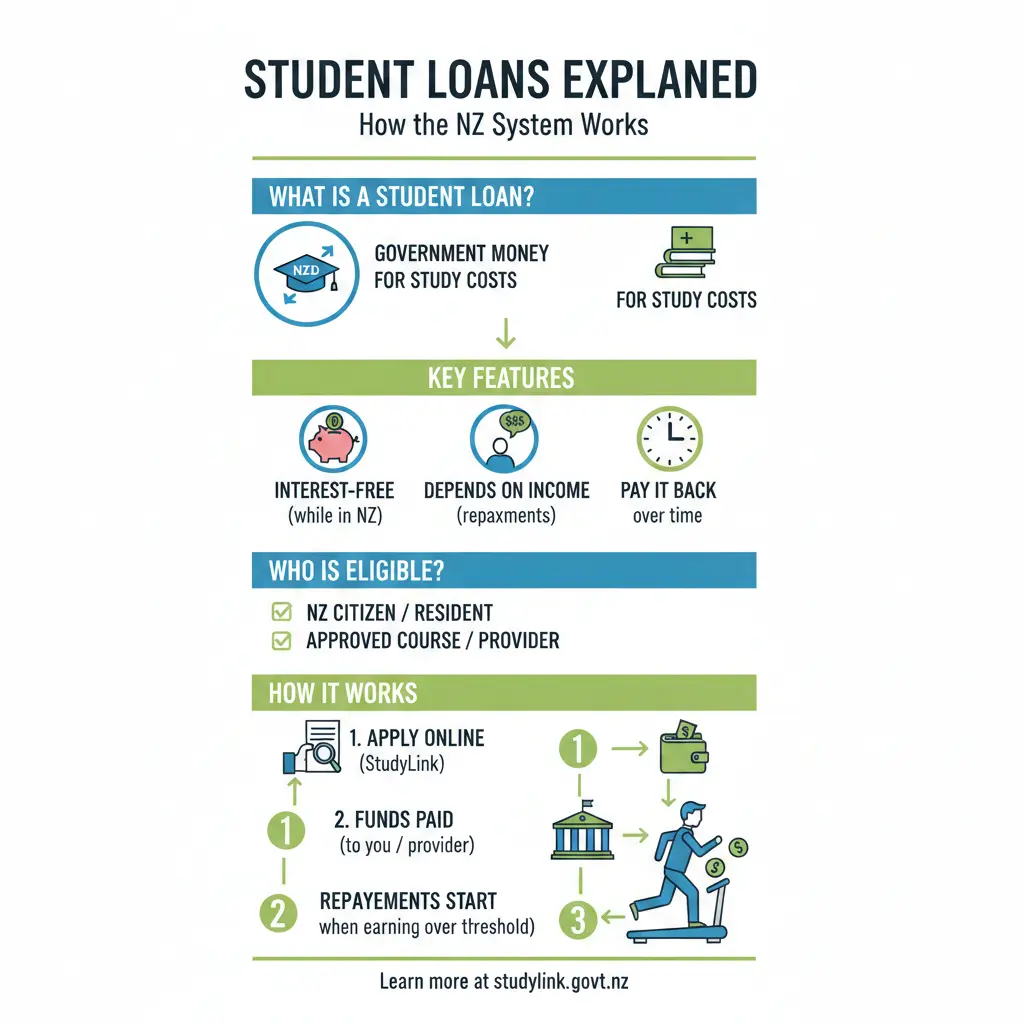

What Is a Student Loan?

A Student Loan is financial help from the Crown to cover the costs of studying at an approved tertiary education provider in New Zealand. Unlike a traditional bank loan, it's specifically designed to support students with course fees, study materials, and living expenses while they're studying full-time or part-time.

The key thing to remember is that it's a loan—you'll need to pay it back once you start earning above a certain threshold. The scheme is administered by StudyLink, which is part of the Ministry of Social Development, and repayments are managed by Inland Revenue once you've finished studying.

What Can You Borrow?

Depending on your circumstances, you can borrow for three different things:

- Compulsory course fees – the tuition fees set by your education provider

- Course-related costs – up to $1,000 for things like books, stationery, or a computer

- Living costs – up to $323.43 per week if you're studying full-time

There's an important limit to know about: you can borrow a maximum of 2 EFTS (Equivalent Full-Time Students) per loan period. This is roughly 240 points or credits, which means you're limited in how much you can borrow each year.

If you're studying part-time, your borrowing options are more limited unless you can be classified as a full-time student. And if you're 55 or older, you can only borrow for compulsory course fees—not living costs or course-related costs.

Who's Eligible for a Student Loan?

To qualify for a Student Loan, you need to meet several criteria:

Residency Requirements

You must be either:

- A New Zealand citizen, or

- Ordinarily resident in New Zealand and have lived here for at least 3 years and held a residence class visa for at least 3 years

There are some exceptions to these rules—for example, if you're a refugee or protected person, different criteria may apply. It's worth checking with StudyLink directly if your situation is unique.

Course Requirements

Your course must be:

- Run by an approved education provider

- An approved course (you can study overseas, but your course must be approved)

- At least 32 weeks long with a minimum of 0.25 EFTS

Who Can't Get a Student Loan

You won't be eligible if you're:

- Still at secondary school

- Bankrupt

- More than $500 behind on existing Student Loan repayments and overdue by a year or more

- Under 18 and studying a fees-free level 1 or 2 qualification or on a Youth Guarantee programme (though you can get one if you're over 18 for these programmes)

- In prison or on a benefit (if you're trying to get living costs)

If you've had a Student Loan before, you'll also need to meet passing requirements and not have exceeded the number of loans you're allowed to take out.

Interest Rates and Charges

One of the most attractive features of New Zealand's Student Loan Scheme is that there's no interest charged while you're studying. This is a significant advantage compared to many other countries.

However, once you've finished your course and start earning, interest does apply. For the 2026 tax year, the base interest rate is 4.9% per year. This interest is charged on your outstanding loan balance, though it only applies once you're earning and required to make repayments.

There's also an establishment fee that's charged when your loan is set up, though the exact amount depends on your individual circumstances.

How Much Will You Pay Back?

Once you're earning, you'll start repaying your loan—but only if your income is above a certain threshold. Here's how it works:

The Repayment Threshold

For the 2026 tax year, the annual repayment threshold is $24,128. This means you only start repaying your loan once you're earning more than this amount per year.

The threshold breaks down into different pay periods:

- $464 per week if you're paid weekly

- $928 per fortnight if you're paid fortnightly

- $1,856 every 4 weeks

- $2,010.66 per month if you're paid monthly

The Repayment Rate

Once you're earning above the threshold, you'll repay 12% of every dollar you earn over the threshold. This is a straightforward calculation.

Here's a practical example: if you're paid weekly and earn $600 before tax in 2026:

$600 (weekly pay) − $464 (weekly threshold) = $136 over the threshold

$136 × 12% = $16.32 repayment

Your employer will automatically deduct this from your pay if you've registered a Student Loan with them, using a tax code with 'SL' (like M SL or ME SL).

What Counts as a New Zealand Based Borrower?

If you're physically in New Zealand for 183 or more consecutive days, you're considered a New Zealand based borrower. This is important because it determines your repayment threshold and interest rate. Some overseas borrowers may be treated as New Zealand based on application.

The Final-Year Fees-Free Scheme

From 1 January 2025, the government introduced a new scheme that allows students to claim up to $12,000 for their final year of study (or final two years of work-based learning). This is a significant change—the scheme previously funded the first year of study.

If you have an existing Student Loan, the final-year fees-free entitlement goes towards your loan balance. You apply through myIR within a year of completing your eligible qualification, and Inland Revenue will make the first payments in 2026 for study completed in 2025.

How to Apply for a Student Loan

Applying for a Student Loan is straightforward:

- Apply online through StudyLink at any time before or during your course

- Provide all required documents and information

- If you're studying for more than one year, you'll need to reapply each year

- Once approved, you'll receive a loan entitlement advice letter detailing your loan details

- Claim course-related costs in MyStudyLink once you've received your Student Loan contract

StudyLink recommends applying before 16 December if you want to be organised for the following year. Once your application is approved and payments are made, your loan is transferred to Inland Revenue, who'll manage your repayments.

Important Things to Remember

Only borrow what you need. Your Student Loan contract is a binding agreement—you'll have to pay back every dollar you borrow. Taking out a loan is a big decision, so it's worth thinking carefully about how much you actually need to study comfortably.

If you're uncertain about any part of the process, you can get independent advice. StudyLink and Inland Revenue both have resources available, and your education provider can also help answer questions about how loans work.

Next Steps

If you're planning to study in 2026, here's what to do:

- Visit StudyLink to check your eligibility and understand what you can borrow

- Apply for your Student Loan before 16 December 2025 to be organised for the new year

- Check with your education provider about approved courses and any specific requirements they have

- Consider how much you actually need to borrow—remember, you'll be paying it back

- Keep records of your application and loan details in MyStudyLink

The Student Loan Scheme has helped countless Kiwis access tertiary education. Understanding how it works—what you can borrow, how repayments work, and what your obligations are—puts you in a strong position to make informed decisions about funding your studies.

Frequently Asked Questions

Sources & References

-

1

Student Loan Contract — www.msd.govt.nz

-

2

Repaying my student loan when I earn salary or wages — www.ird.govt.nz

-

3

Student Loan — www.studylink.govt.nz

-

4

Learners can now apply for final-year Fees Free — www.tec.govt.nz

-

5

Students can now claim $12,000 but is it money well spent? — www.rnz.co.nz

-

6

Getting ready for 2026 — www.providers.studylink.govt.nz

Useful Tools

Related Articles

The 2026 Student Loan Guide: Repayments; Interest; and Strategies

Heading into 2026, many Kiwis are navigating their student loans with repayments kicking in at just $24,128 a year and interest at 4.9%—but smart strategies can make all the difference in paying it of...

The Ultimate Word Counter for NZ Students and Writers

Ever stared at your screen at 2am, racing to finish that uni essay, only to realise you've smashed past the word limit by 500 words? Or worse, come up short and need to pad it out without sounding flu...

Scholarships & Financial Aid for Tertiary Study in NZ

Pursuing tertiary education in New Zealand doesn't have to drain your bank account. Whether you're a school leaver, career changer, or postgraduate student, there's a surprising range of scholarships...

Studying Part-Time While Working: A Kiwi's Guide

Balancing a full-time job with part-time study is a smart move for many Kiwis looking to boost their career without hitting pause on life. Whether you're eyeing a promotion, switching fields, or just...