ACC Explained: What’s Covered if You Have an Accident in NZ?

Picture this: you're out for a weekend tramp in the Coromandel, slip on a wet rock, and end up with a twisted ankle and a sprained wrist. The pain hits hard, but so does the relief of knowing New Zeal...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Picture this: you're out for a weekend tramp in the Coromandel, slip on a wet rock, and end up with a twisted ankle and a sprained wrist. The pain hits hard, but so does the relief of knowing New Zealand's no-fault accident compensation scheme has your back. That's ACC in action – our world's unique safety net that covers personal injury from accidents without the hassle of proving blame.

Whether you're a Kiwi worker clocking overtime, a student on a gap year adventure, or a visitor exploring our stunning landscapes, ACC steps in when accidents happen. But what exactly is covered? In this guide, we'll break it down with the latest 2026 details, real-life examples, and practical tips to help you navigate claims, coverage, and recovery. Let's dive in so you're prepared for whatever comes your way.

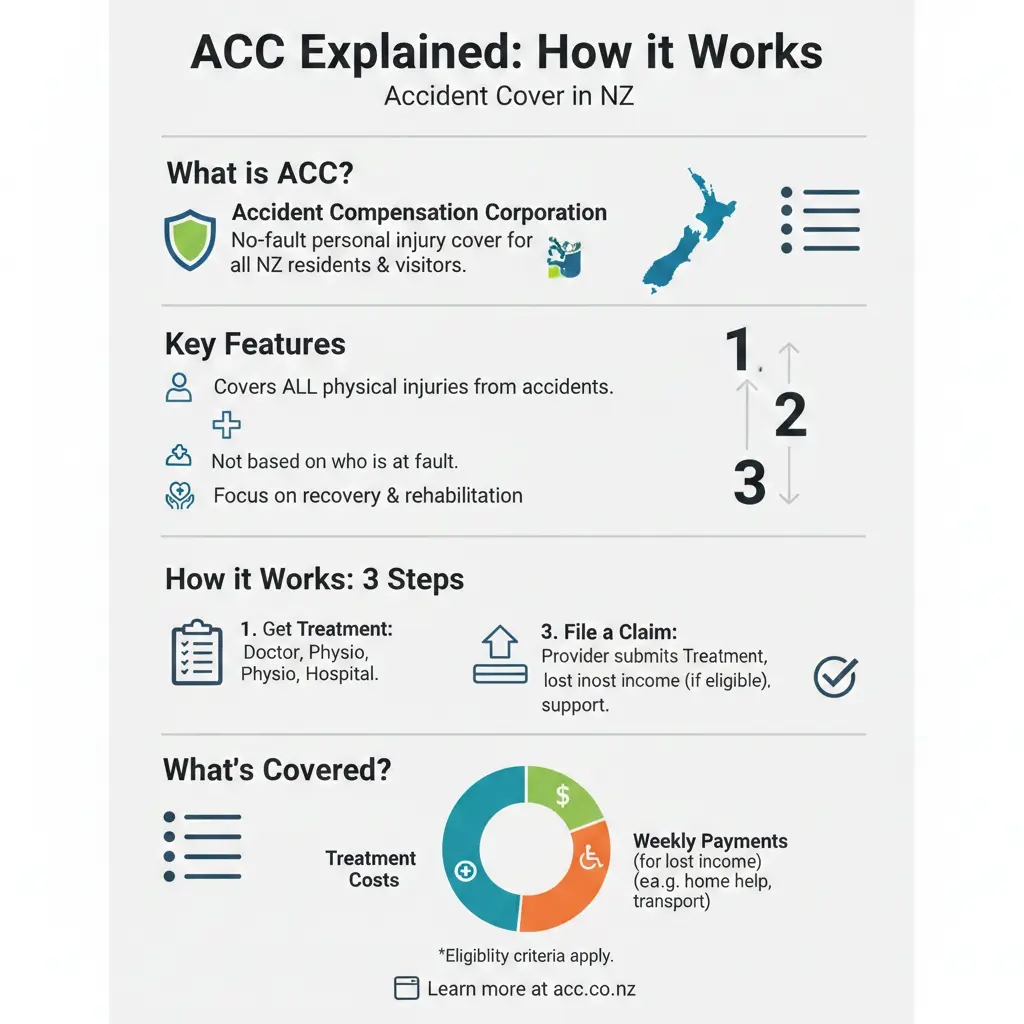

What is ACC and How Does It Work?

ACC, or the Accident Compensation Corporation, is New Zealand's publicly funded, no-fault personal injury cover scheme. It provides accident insurance for all New Zealanders and visitors, helping over two million new claims each year to get people back to everyday life. Unlike traditional insurance, you don't need to prove fault – if it's a personal injury from an accident, you're covered.

The scheme is funded mainly through levies on earners, employers, and vehicle registrations, ensuring broad support. ACC's core functions include injury prevention, rehabilitation, and compensation, all aimed at sustainability for current and future generations.

Key Principles of the ACC Scheme

- No-fault cover: Coverage regardless of who caused the accident.

- 24/7 protection: Applies anywhere in New Zealand, and for Kiwis overseas in some cases.

- Universal access: Everyone in NZ, including tourists, gets the same entitlements.

- Rehabilitation focus: Emphasis on getting you back to work and independence quickly.

What Counts as an 'Accident' Under ACC?

ACC defines an accident as any specific event that causes personal injury, like a fall, car crash, or sports mishap. It must result in harm such as sprains, fractures, or wounds – not illnesses or gradual wear-and-tear. For example, if you're biking in Auckland traffic and get clipped by a car, that's covered. But a sore back from years of manual labour might not be, unless linked to a specific incident.

Common Accident Types Covered

ACC handles a huge range of incidents. Here's what typically qualifies:

- Work-related injuries: Slips in the warehouse, machinery accidents, or repetitive strain from a one-off event.

- Sports and recreation: Rugby tackles, skiing wipeouts, or gym equipment failures – think a netball player in Wellington twisting her knee mid-game.

- Motor vehicle crashes: From State Highway 1 pile-ups to urban scooter collisions.

- Home and everyday mishaps: Kitchen burns, DIY power tool injuries, or tripping on uneven paths during a family bush walk.

- Medical misadventure: Rare cases of faulty treatment causing further injury.

In 2025/26, ACC is ramping up efforts to support Māori claimants, targeting a 26.3% claim lodgement rate increase to address access barriers.

What's Not Covered?

Not everything qualifies. Exclusions include:

- Sickness or disease (e.g., flu or cancer).

- Gradual process injuries without a specific incident (e.g., chronic back pain).

- Self-inflicted injuries or those from illegal activities.

- Injuries abroad for visitors (unless from NZ).

If in doubt, lodge a claim – ACC assesses on a case-by-case basis.

What's Covered: Entitlements Breakdown

Once approved, ACC covers a wide range of support tailored to your needs. Coverage includes treatment, weekly compensation, and rehab to minimise long-term impacts.

Treatment and Rehabilitation

ACC funds necessary medical care to help you recover:

- GP visits, specialists, x-rays, and surgeries.

- Physiotherapy, acupuncture, and gym programmes.

- Home help, transport to appointments, and childcare if needed.

The 2025/26 turnaround plan prioritises quicker rehab with 285 new case managers to get claimants back to work faster, avoiding prolonged reliance on the scheme.

Weekly Compensation

If you're off work 7+ days, you get 80% of your pre-injury earnings (up to a maximum weekly rate – check acc.co.nz for 2026 caps). For non-earners like students or caregivers, there's a flat rate. Payments start from day 1 for treatment, but weekly comp from week 2.

Example: A Christchurch builder earning $1,200/week pre-injury gets about $960/week while sidelined by a ladder fall.

Lump Sums and Independence Allowances

- Lump sums: For permanent impairment, up to $1.3 million max (2026 rates).

- Independence allowance: Ongoing help if you can't work long-term due to multiple injuries.

Other Supports

ACC also covers funeral grants, survivor grants for dependents, and home modifications like ramps for serious injuries.

How to Make an ACC Claim in 2026

Lodging a claim is straightforward and free. Here's your step-by-step guide:

- Report immediately: Tell your doctor or employer within 7 days – they often lodge for you.

- Online or app: Use MyACC app or acc.co.nz for quick lodgement.

- Provide details: Describe the accident, injuries, and impacts.

- Wait for assessment: ACC covers initial treatment while deciding (usually 4-6 weeks).

- Appeal if needed: Review or District Court options if declined.

Pro tip: Keep receipts and photos – they speed things up. ACC's 2026 service agreement aims for better client-first care.

Recent Changes and ACC's 2026 Turnaround Plan

ACC faces challenges like a projected $26b deficit by 2030 due to inflation, health pressures, and court expansions. The 2025/26 turnaround plan focuses on:

- Hiring more staff for personalised case management.

- Stronger rehab expectations – you'll need to participate actively.

- Basics like faster claims and better outcomes without cutting cover scope.

- Projections show a $2b surplus by 2030 with these reforms.

Recent laws clarify ACC overlaps with WINZ benefits, ensuring fair treatment – backdated ACC won't double-dip on welfare.

Practical Tips for Kiwis Dealing with ACC

- Prevent first: ACC funds safety initiatives – check work risk assessments or wear helmets on the bike.

- Stay engaged: Attend all rehab sessions; non-participation can affect entitlements.

- Track everything: Use MyACC for updates and payments.

- Seek advice: Free advocates via Citizens Advice Bureau or union reps.

- For employers: Support return-to-work plans to avoid levy hikes.

Next Steps: Stay Safe and Prepared

ACC is there when you need it, but prevention is best. Review your levy via myIR, update MyACC profile today, and chat to your whānau about safety. If injured, claim promptly – recovery starts with the right support. For personalised help, head to acc.co.nz or call 0800 101 996. Here's to fewer accidents and faster comebacks for all Kiwis.

Frequently Asked Questions

Sources & References

-

1

ACC Service Agreement 2025/26 — www.acc.co.nz

-

2

ACC Turnaround Plan to Deliver Better Outcomes — www.acc.co.nz

-

3

ACC's Back-to-Basics Plan — thespinoff.co.nz

-

4

ACC Focus on Rehabilitation to Avoid Deficit — www.nzherald.co.nz

-

5

ACC Moves to Avert Funding Gap — insurspy.co.nz

-

6

Government to Clarify Welfare and ACC Payments — www.beehive.govt.nz

Related Articles

ACC for Self-Employed: Understanding Your Levies

If you're a self-employed Kiwi juggling gigs, trades, or your own business, one bill that can catch you off guard is your ACC levy invoice. Understanding how these levies work ensures you're covered f...

ACC vs Private Insurance: What's the Difference?

Imagine slipping on a wet floor at work and breaking your arm—that's when ACC steps in seamlessly, covering your treatment and lost wages. But what if a cancer diagnosis sidelines you for months? ACC...