ACC for Self-Employed: Understanding Your Levies

If you're a self-employed Kiwi juggling gigs, trades, or your own business, one bill that can catch you off guard is your ACC levy invoice. Understanding how these levies work ensures you're covered f...

Emma writes about health, wellbeing, and ACC topics for Lifetimes NZ. She translates complex health information into clear, actionable advice for New Zealand readers.

If you're a self-employed Kiwi juggling gigs, trades, or your own business, one bill that can catch you off guard is your ACC levy invoice. Understanding how these levies work ensures you're covered for injuries without nasty surprises come tax time.

ACC (Accident Compensation Corporation) provides no-fault cover for work, home, and leisure injuries across New Zealand. For self-employed folks, levies fund this safety net based on your income and job risk. With changes rolling out in 2025 and 2026, now's the time to get clued up on ACC for Self-Employed: Understanding Your Levies so you can plan ahead and avoid cash flow hiccups.

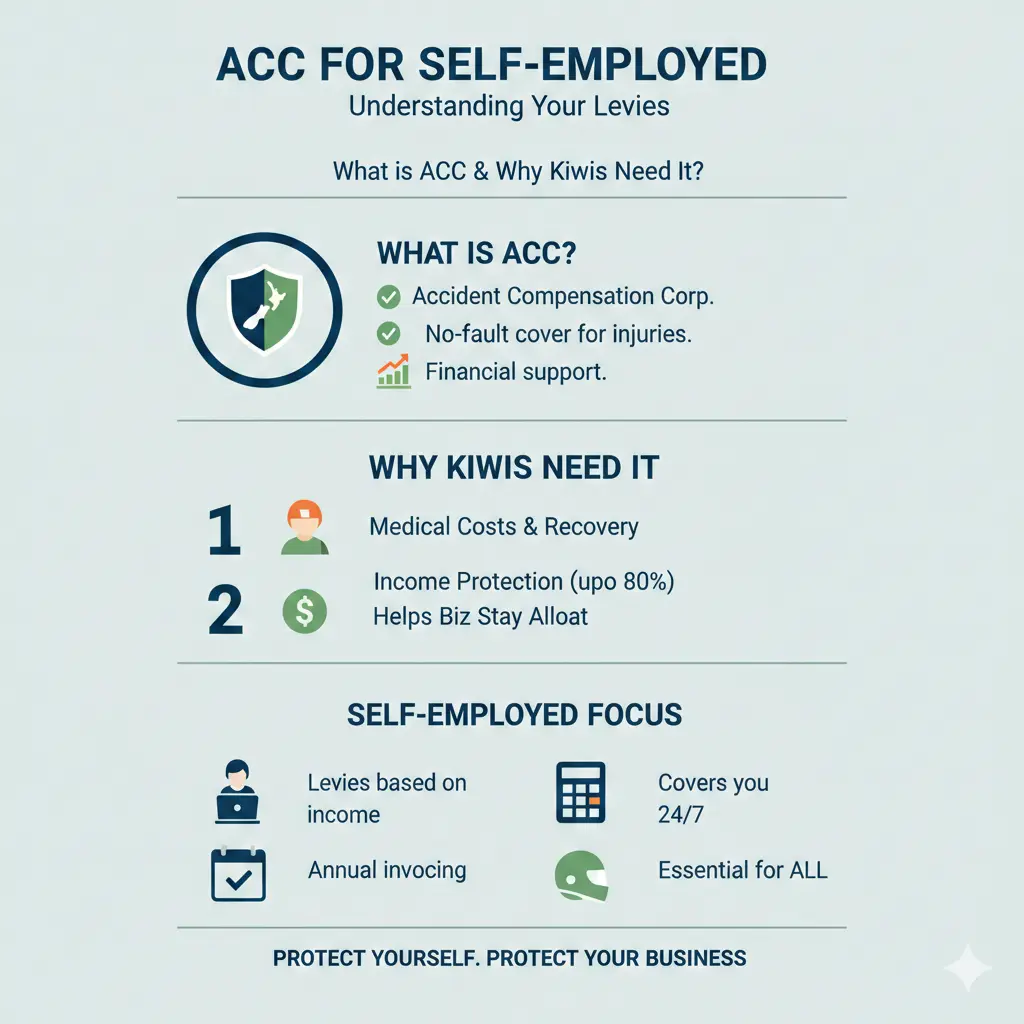

What is ACC and Why Do Self-Employed Kiwis Need It?

ACC is New Zealand's accident compensation scheme, replacing the old court-based system to deliver fast, fair support for injuries. It covers medical costs, weekly compensation up to 80% of your earnings, and rehab services—no matter if the injury happens at work, home, sports, or driving.

As a self-employed person, you're both an earner and a business owner, so you pay levies like everyone else. Employees get theirs deducted via PAYE, but sole traders and contractors handle it themselves after filing with IRD. Skip it, and you risk gaps in cover or penalties.

Your Automatic Cover: CoverPlus Explained

When you start self-employment, ACC automatically puts you on CoverPlus—the standard policy. It covers 100% of your liable income up to the annual maximum. No paperwork needed upfront; ACC pulls your details from your IRD tax return.

- Pros: Simple, full cover based on actual earnings.

- Cons: Levy invoice hits post-tax return (around July-August), based on prior year's income.

Upgrade Option: CoverPlus Extra (CPX)

Want more control? Switch to CoverPlus Extra (CPX). You pick your cover level—say, $100,000 instead of full income—for potentially lower levies if earnings fluctuate. Invoices come in April, with provisional payments and year-end adjustments.

To switch, apply via the ACC website or call 0800 222 902. Ideal for high earners or those with variable income.

How ACC Levies Are Calculated for Self-Employed

Your levies break into three parts: Earner's Levy, Work Levy, and Working Safer Levy. They're charged per $100 of liable income, with minimum and maximum thresholds set yearly.

Key Components

Liable Income: Self-employment earnings declared to IRD, excluding rental income. For FY 2025/26, minimum threshold is $49,365; maximum $152,790. Levies apply only between these.

BIC/CU Code: Your Business Industry Classification (BIC) or Classification Unit (CU) reflects job risk. Web designers pay less than jockeys or builders. Find yours via ACC's online tool or levy calculator.

Levy Rates (as of April 2025):

- Earner's Levy: Flat $1.67 per $100 liable income.

- Work Levy: Varies by BIC/CU (e.g., higher for construction).

- Working Safer Levy: Flat rate per $100 to promote safety.

Step-by-Step Calculation Example

Say you're a freelance graphic designer (low-risk CU) earning $120,000 liable income in FY 2025/26.

- Cap at max: $120,000 (under $152,790).

- Earner's Levy: ($120,000 / 100) x $1.67 = $2,004.

- Work Levy: Check CU rate (e.g., 0.45 per $100) = ($120,000 / 100) x 0.45 = $540.

- Working Safer: Say $0.20 per $100 = $240.

- Total: ~$2,784 (plus GST if applicable).

Use ACC's free levy estimator for your exact figures.

Upcoming Changes: What Self-Employed Need to Know for 2026

ACC is tweaking levies from July 2025 and April 2026 to boost fairness and sustainability. Self-employed on CoverPlus will see impacts via updated rates and rules.

Major Updates

- Average levy rate increase: Expect higher baseline costs.

- New min/max earnings: Adjusted annually; check ACC for 2026 figures.

- New classifications: Sports operators and home improvement stores get specific BIC codes.

- Interest on instalments: From 2026, all plans charge interest.

- Experience Rating shift: Non-participants won't subsidise others from 2026.

- No Claims Discount ends: Gone from 2026—no more discounts for clean records.

These aim to better match levies to risk and claims. Businesses outside Experience Rating get relief, but overall rates rise. Recalculate using ACC's tools post-April 2026.

Managing and Paying Your ACC Levies

ACC invoices automatically after your IRD return (CoverPlus) or April renewal (CPX). New sole traders get their first in year two.

Payment Options

- Lump sum: Due on invoice (avoids interest).

- Instalments: Flexible plans, but interest applies from 2026.

- Online, bank transfer, or direct debit via ACC portal.

Practical Tips for Self-Employed Kiwis

- Set aside cash: Stash 2-3% of income monthly (e.g., via apps like Solo).

- Track BIC/CU: Confirm yours matches your work to avoid reassignment penalties.

- Review cover yearly: Switch to CPX if income dips.

- Claim smart: Report injuries early for weekly comp (up to $1,223/week max).

- Bundle with tax: Use accounting tools linking IRD and ACC estimates.

- Stay safe: Lower risk = lower levies long-term.

For high-risk trades like roofing or fishing, consider Experience Rating to reduce levies based on your claims history (until 2026 changes).

Common Mistakes and How to Avoid Them

Don't get stung—many self-employed overlook ACC until the invoice lands.

- Mistake 1: Forgetting rental income exclusion—good news, it's levy-free.

- Mistake 2: Wrong BIC/CU—leads to over/underpayment and adjustments.

- Mistake 3: Ignoring provisional invoices for CPX—pay estimates to avoid big bills.

- Mistake 4: Not budgeting—treat levies like GST, set aside from day one.

Next Steps: Stay Covered and Levy-Savvy

Head to the ACC website today: estimate your levy, check your BIC, and consider CPX if it fits. Link your IRD myIR account for seamless tracking. Set a calendar reminder for April 2026 updates, and stash funds monthly to smooth cash flow. You're building your business—don't let an injury or surprise bill slow you down. For personalised advice, chat with an accountant or call ACC at 0800 222 902.

Frequently Asked Questions

Sources & References

-

1

ACC Workplace Cover Levy Changes - NZQBA — nzqba.co.nz

-

2

ACC Guide for Self-Employed - Solo NZ — www.soloapp.nz

-

3

ACC levies - Business.govt.nz — www.business.govt.nz

-

4

A guide to ACC levies for sole traders | Hnry — hnry.co.nz

-

5

Upcoming levy changes for business - ACC — www.acc.co.nz

Related Articles

ACC Explained: What’s Covered if You Have an Accident in NZ?

Picture this: you're out for a weekend tramp in the Coromandel, slip on a wet rock, and end up with a twisted ankle and a sprained wrist. The pain hits hard, but so does the relief of knowing New Zeal...

ACC vs Private Insurance: What's the Difference?

Imagine slipping on a wet floor at work and breaking your arm—that's when ACC steps in seamlessly, covering your treatment and lost wages. But what if a cancer diagnosis sidelines you for months? ACC...