Credit Scores NZ: How They Work and How to Check

Ever wondered why your loan application got rejected despite a steady job and regular KiwiSaver contributions? Or why interest rates seem sky-high on that personal loan you're eyeing? The culprit is o...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Ever wondered why your loan application got rejected despite a steady job and regular KiwiSaver contributions? Or why interest rates seem sky-high on that personal loan you're eyeing? The culprit is often your credit score—a number that lenders in New Zealand scrutinise more closely than ever in 2026. Understanding credit scores NZ isn't just smart; it's essential for securing better rates on everything from mortgages to mobile contracts. This guide breaks it down: how they work, how to check yours, and actionable steps to boost it.

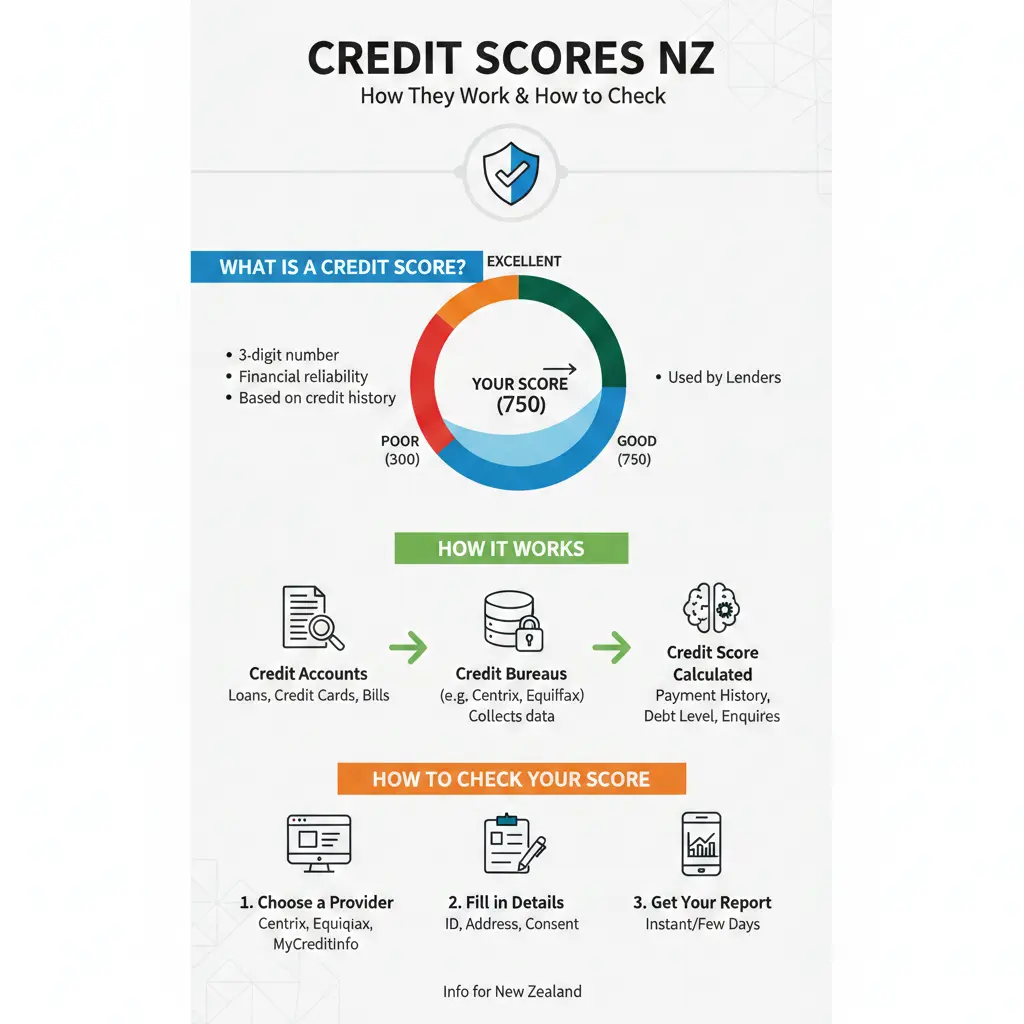

What Is a Credit Score in New Zealand?

In New Zealand, your credit score is a three-digit number (typically ranging from 0 to 1000 or 1200, depending on the agency) that summarises your creditworthiness based on your financial behaviour over the past five years. Unlike the US system, which emphasises credit card usage and history length, Kiwi scores prioritise payment history, defaults, and repayment timeliness. It's not a single national score—three main credit reporting agencies (Centrix, Equifax, and Illion) each calculate their own, so your number might vary slightly.

A good credit score in NZ generally falls between 650 and 749, with scores above 750 rated very good and over 800 excellent. The national average sits at 752 as of recent data, down slightly from 755 the year prior, showing most Kiwis maintain solid standings—but 46% don't even know their score. Low scores (under 600) can mean higher interest rates or outright rejections, especially from risk-averse banks.

Credit Score Ranges Across NZ Agencies

Each agency uses its own scale, but they align on key meanings. Here's a comparison:

| Rating | Centrix (0-1000) | Equifax (0-1200) | Illion (0-1000) | What It Means |

|---|---|---|---|---|

| Low/Poor | 0-494 | 0-509 | 0-299 | Defaults or missed payments; limited options, high rates |

| Fair | 495-649 | 510-621 | 300-499 | Improving but with negatives; possible approvals with checks |

| Good | 650-768 | 622-725 | 500-699 | Solid history; favourable for most loans |

| Very Good | 769-845 | 726-832 | 700-799 | Strong profile; better rates and terms |

| Excellent | 846-1000 | 833-1200 | 800-1000 | Top-tier; prime rates, high approvals |

Scores below 450 often block major bank loans. Remember, a score alone doesn't decide approvals—lenders also check income, application details, and more.

How Credit Scores NZ Are Calculated

Credit scores draw from your credit report, a record of your credit applications, accounts, repayments, defaults, and judgments. Agencies like Centrix (NZ's locally owned bureau covering 95% of credit-active Kiwis) collect this data from lenders, utilities, and courts. Positive history—like on-time bill payments—boosts your score, while negatives linger for up to five years.

Key Factors Affecting Your Score

- Payment History (Biggest Influence): On-time payments on loans, credit cards, power bills, and even phone contracts build your score. Late payments or defaults tank it.

- Credit Applications: Each hard inquiry (e.g., loan apps) is noted for five years. Too many signal risk—space them out.

- Credit Utilisation: Keep balances low relative to limits (under 30% ideal) to avoid red flags.

- Length of History: Longer, stable credit use helps, especially for excellent scores.

- Defaults/Collections: Serious negatives stay five years from default date.

Data retention varies: repayment history for two years post-due date, defaults for five years. Court judgments or bankruptcies also appear, impacting insurances and rentals too.

"Credit history influences not just mortgages and loans, but electricity, bank accounts, phone contracts, insurance, and car finance. The better your history, the more options you'll get."

How to Check Your Credit Score in New Zealand

Good news: You're entitled to a free credit report from each agency annually under NZ privacy laws—no credit card needed. Scores might be free or low-cost. Here's how:

Free Credit Checks: Step-by-Step

- Centrix: NZ's biggest—visit Centrix My Credit Score. Get your report instantly online (1-1000 scale). Covers 95% of Kiwis.

- Equifax (My Credit File): Free report via Equifax NZ or app. Scores 0-1200; processing up to 20 days.

- Illion (Credit Simple): Free score and report at Credit Simple. 0-1000 scale; quick online access.

- Experian: Order free via CreditConnect.

Expect 60 seconds to 20 working days. Check all three for the full picture—disputes are free if info's wrong. Pro tip: Set up free monthly score monitoring where available to track changes without hard inquiries.

How to Improve Your Credit Score in NZ

Boosting your score takes time—aim for consistent habits over 3-6 months. Here's a practical plan tailored for Kiwis:

Quick Wins (0-3 Months)

- Pay everything on time—set auto-payments for power, IRD, and loans.

- Reduce credit card balances below 30% utilisation.

- Dispute errors on your report promptly.

- Avoid new applications; some lenders like Pioneer don't impact scores.

Long-Term Strategies (3+ Months)

- Build history: Use a secured credit card or small loan, repay fully.

- Diversify credit: Mix cards and loans responsibly.

- Clear defaults: Negotiate payment plans; they drop off after five years.

- Register on electoral roll and keep addresses updated for positive verification.

For migrants: Start with utility bills and low-limit cards to build a Kiwi history—takes 6-12 months. Better scores mean lower rates; e.g., prime borrowers get from 6.99% p.a., while poor ones pay more.

Common Pitfalls to Avoid

- Maxing credit limits—even if paid off monthly.

- Closing old accounts (shortens history).

- Ignoring soft inquiries like pre-approvals—they're safe.

What a Good Credit Score Gets You in 2026

In NZ's cautious lending market, high scores unlock better deals. Excellent ratings mean faster approvals for mortgages (e.g., via KiwiBank or ASB), personal loans from Harmoney or Squirrel at low rates, and even cheaper insurance. Low scores? Expect scrutiny, higher rates (12-20%+), or denials—especially post-2026 economic shifts. WINZ or budgeting services can help if debt's an issue.

Disclaimer: This isn't personalised financial advice. Consult a licensed adviser or visit Sorted.org.nz for your situation.

Next Steps to Master Your Credit Score

Grab your free reports today from Centrix, Equifax, and Illion—knowledge is power. Track monthly, pay on time, and watch your score climb. Pair this with KiwiSaver boosts and IRD compliance for full financial health. In 2026's market, a strong score could save thousands on your next home loan or car finance. Start now, and lenders will notice.

Frequently Asked Questions

Sources & References

-

1

The Ultimate Guide to Understanding Credit Scores in New Zealand — pioneerfinance.co.nz

- 2

-

3

Complete Guide to Building Credit After Migrating to New Zealand — alternatefinance.co.nz

-

4

How Credit Scores Work in New Zealand - MoneyHub NZ — www.moneyhub.co.nz

-

5

Check My Credit Score | My Credit Report NZ - Centrix — www.centrix.co.nz

-

6

Credit checks, scores and history - Consumer Protection — www.consumerprotection.govt.nz

-

7

Order your credit report via CreditConnect - Experian New Zealand — www.experian.co.nz

-

8

2026 Credit Research Outlook - State Street Global Advisors — www.ssga.com

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...