Leaky Building History: How to Check Before You Buy

Imagine discovering your dream home is hiding a nightmare of rotting timber, mould, and repair bills running into hundreds of thousands. For Kiwis buying property, the leaky building history remains a...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

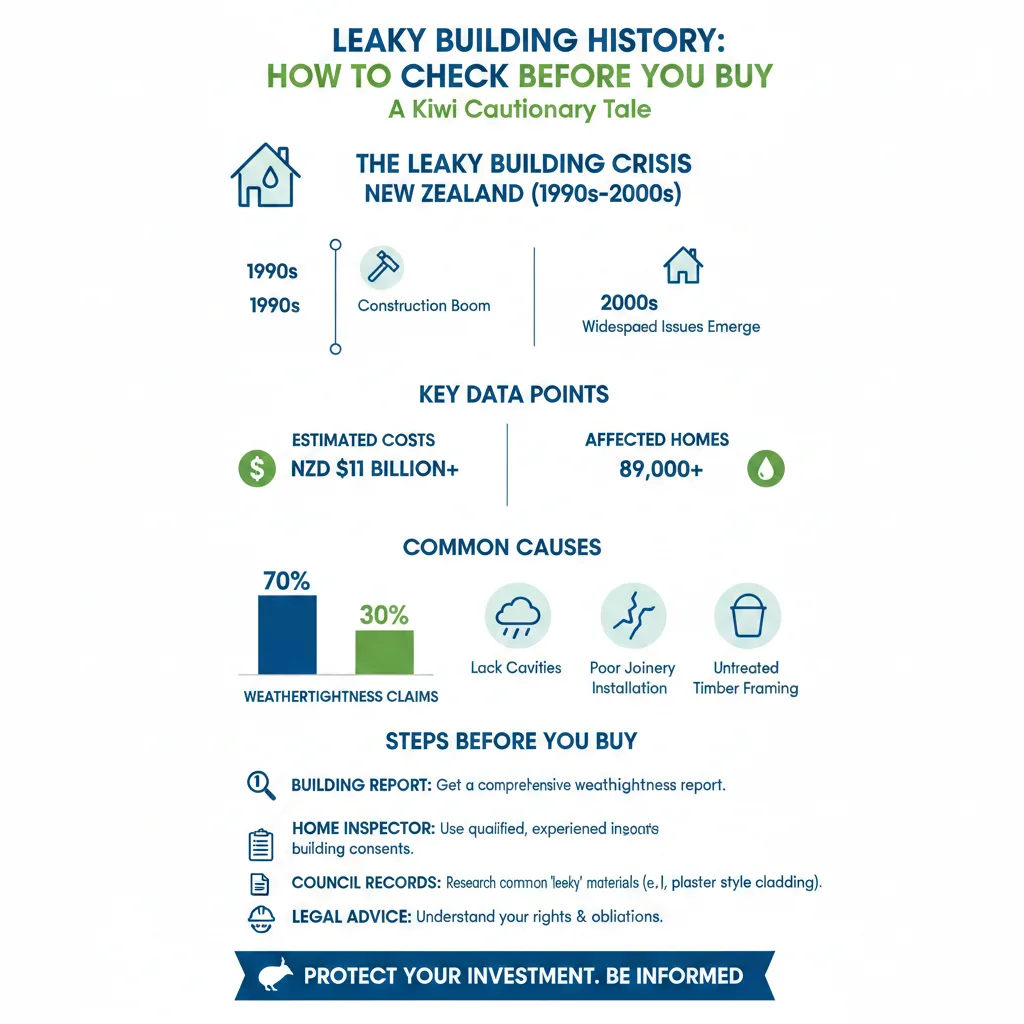

Imagine discovering your dream home is hiding a nightmare of rotting timber, mould, and repair bills running into hundreds of thousands. For Kiwis buying property, the leaky building history remains a stark reminder of why checking before you buy is non-negotiable. With New Zealand still reeling from a crisis that cost up to $47 billion and affected nearly 90,000 homes, knowing how to uncover a property's weathertight past could save you from financial ruin.

In the 1990s and early 2000s, a perfect storm of imported claddings, untreated timber, and lax regulations turned thousands of Kiwi homes into moisture traps. Today, in 2026, while reforms aim to prevent a repeat, over a third of new builds in greater Auckland are failing final inspections due to issues like cladding (22.1%), framing (27%), and drainage (14.5%). As building consents hit 10-year lows and productivity lags, buyers must arm themselves with knowledge to navigate this risky market.

The Leaky Building Crisis: A Kiwi Cautionary Tale

New Zealand's leaky homes epidemic peaked in the late 1990s and early 2000s, triggered by deregulation in the 1980s that shifted to a self-regulated, hands-off model. Builders adopted overseas claddings without proper testing for our wet climate, paired with untreated timber frames that rotted when water infiltrated. The result? Mouldy walls, structural decay, and health issues like respiratory illnesses costing $145 million annually in hospitalisations.

Councils, as Building Consent Authorities, faced massive payouts after court battles, affecting 73 local bodies nationwide. Estimates peg the total economic hit at $23-47 billion, with up to 89,000 buildings impacted. Real-life horror stories abound: one apartment complex revealed disintegrating pipes lacking fire collars and seismic weaknesses only after invasive probes.

Why It Happened: Key Culprits

- Monoclad and stucco systems: These plaster-based claddings trapped moisture behind facades, common in monolithic designs.

- Untreated timber: Kiwi timber wasn't kiln-dried properly, accelerating rot in damp cavities.

- "Build now, fix later" culture: A 2014 BRANZ study found 92% of new houses had compliance defects, with productivity losses equating to 5,000 missing Auckland homes yearly.

- Poor oversight: Self-certification led to a tick-box mentality, ignoring real-world performance.

Fast-forward to 2026: Despite Healthy Homes Standards for rentals, one-third of Auckland projects still fail final checks, fuelling fears of history repeating.

2026 Updates: Reforms to Curb the Crisis

The government is acting. Building Minister Chris Penk announced 2026 changes strengthening Licensed Building Practitioner accountability, including improved complaints processes, public suspension registers, and ethics codes for plumbers, electricians, and drainlayers. A $2.5 billion Building Bill targets the "build now, fix later" mindset by clarifying liability and speeding consents.

Yet challenges persist. Concrete sales dropped 15.4% year-on-year, signalling a thinning new-build pipeline amid rising re-inspections—up to 220,000 annually. For buyers, this means older homes (pre-2010) carry higher risks, but vigilance is key even for newer ones.

How to Check Leaky Building History: Step-by-Step Guide

Don't rely on seller disclosures alone—they're not foolproof. Follow this actionable checklist tailored for Kiwi buyers to reveal a property's leaky building history.

Step 1: Run a LIM and Property File Search

Every council-issued Land Information Memorandum (LIM) details consents, code compliance certificates (CCCs), and weathertightness issues. Request the full property file for plans, inspections, and remediation records—essential for pre-1990s homes.

- Cost: $200-400, available via council websites or services like Certificate of Title NZ.

- Red flags: Missing CCCs (required since 1992), remediation consents, or water ingress complaints.

Step 2: Conduct a Weathertightness Title Search

Leaky claims often appear on Land Information Memoranda (LIMs) or affect titles via caveats. Specialist searches scan for:

- Financial Assistance for Weathertight Homes (FAWH) claims.

- Council settlements or insurance disputes.

- Body corporate litigation for apartments.

Services like Certificate of Title NZ flag these instantly, crucial since leaky history can slash resale value by 20-50%.

Step 3: Hire a Specialist Building Inspector

Skip the generalist—engage an NZ Institute of Building Surveyors member experienced in weathertightness. They use moisture meters, thermal imaging, and invasive tests (with permission) to detect hidden rot.

- Inspect cladding joins, decks, balconies, and penetrations (windows, vents).

- Test cavities for drainage planes and flashings.

- Check untreated timber exposure—pre-2005 builds are prime suspects.

Expect $800-2,000; insist on a detailed report with photos.

Step 4: Review Body Corporate Records (for Apartments/Units)

Under Unit Title Act 2010, request minutes, levies, and sinking funds for the last 10 years. Probe for special levies funding leaky repairs—common in 2000s complexes.

Step 5: Engage a Lawyer and Get a Producer Statement

Your conveyancer can cross-check against EQC claims (via eqc.govt.nz) and peer reviews designs. Demand PS4 Producer Statements from designers confirming compliance.

Bonus Checks: Insurance and Valuation

Alert your insurer pre-purchase—leaky history may void house insurance. Bank valuers often note risks, influencing lending (e.g., lower LVRs).

Red Flags: Signs of Leaky Trouble

Visual cues aren't definitive but warrant deeper digs:

- Staining or efflorescence on walls/windows.

- Buckled cladding or swollen frames.

- Mouldy interiors, musty smells, or health complaints from sellers.

- History of multiple owners or quick sales.

- Monolithic cladding on multi-storey homes (pre-2011 Acceptable Solution E2/AS1).

Invasive signs require drilling: soft timber, corroded fixings, or failed fire barriers.

Costs of Getting It Wrong vs. Checking Right

Average leaky remediation: $100,000-$500,000 per home, plus lost equity. Proactive checks ($2,000-5,000 total) pale in comparison. Post-2026 reforms may shift liability to builders, but buyers still bear upfront risks.

"Councils can't afford another crisis—neither can you," echoes industry warnings, with productivity drags costing the sector 10% of output.

FAQ: Leaky Building Checks

Q1: Do all pre-2010 homes have leaky issues?

A: No, but 1990s-2000s builds using monoclad are highest risk. A title search clarifies.

Q2: What's the difference between LIM and property file?

A: LIM summarises; the full file has raw docs like inspection notes—request both.

Q3: Can I claim on EQC for leaky homes?

A: Generally no—EQC covers weather damage, not poor construction. Check via their portal.

Q4: How do 2026 changes affect buyers?

A: Stronger practitioner accountability reduces future risks, but doesn't retro-fix old stock.

Q5: Is thermal imaging enough?

A: It's a start, but pair with moisture probes for accuracy—hire specialists.

Q6: What if the seller refuses inspections?

A: Walk away—it's a major red flag under the fair trading principle of the Property Law Act.

Your Next Steps: Buy Smart, Stay Dry

Start with a title search today via Certificate of Title NZ, then layer on LIM, inspection, and legal review. Budget 1% of purchase price for due diligence—it's your best insurance against New Zealand's lingering leaky legacy. Consult a licensed professional for tailored advice; this isn't financial guidance.

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...