Utes and Work Vehicles: Tax and FBT Considerations

Picture this: you're cruising down State Highway 1 in your trusty double-cab ute, fresh from a job site, but as you pull into the driveway, a nagging thought hits—am I racking up Fringe Benefit Tax (F...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Picture this: you're cruising down State Highway 1 in your trusty double-cab ute, fresh from a job site, but as you pull into the driveway, a nagging thought hits—am I racking up Fringe Benefit Tax (FBT) without even knowing it? For Kiwi business owners, tradies, and farmers, utes and work vehicles are lifelines, but navigating their tax and FBT implications can feel like tackling a gravel road in the rain.Utes and work vehicles aren't automatically FBT-free, despite common myths, and with changes looming from 1 April 2026, getting it right now could save you thousands.Tax and FBT considerations for these vehicles demand attention to avoid IRD surprises.

In this guide, we'll break down the current rules, unpack proposed reforms, and arm you with practical steps tailored for New Zealand businesses. Whether you're eyeing a new Ford Ranger or keeping your Toyota Hilux fleet humming, understanding depreciation, exemptions, and FBT calculations keeps your operation compliant and cashflow positive.

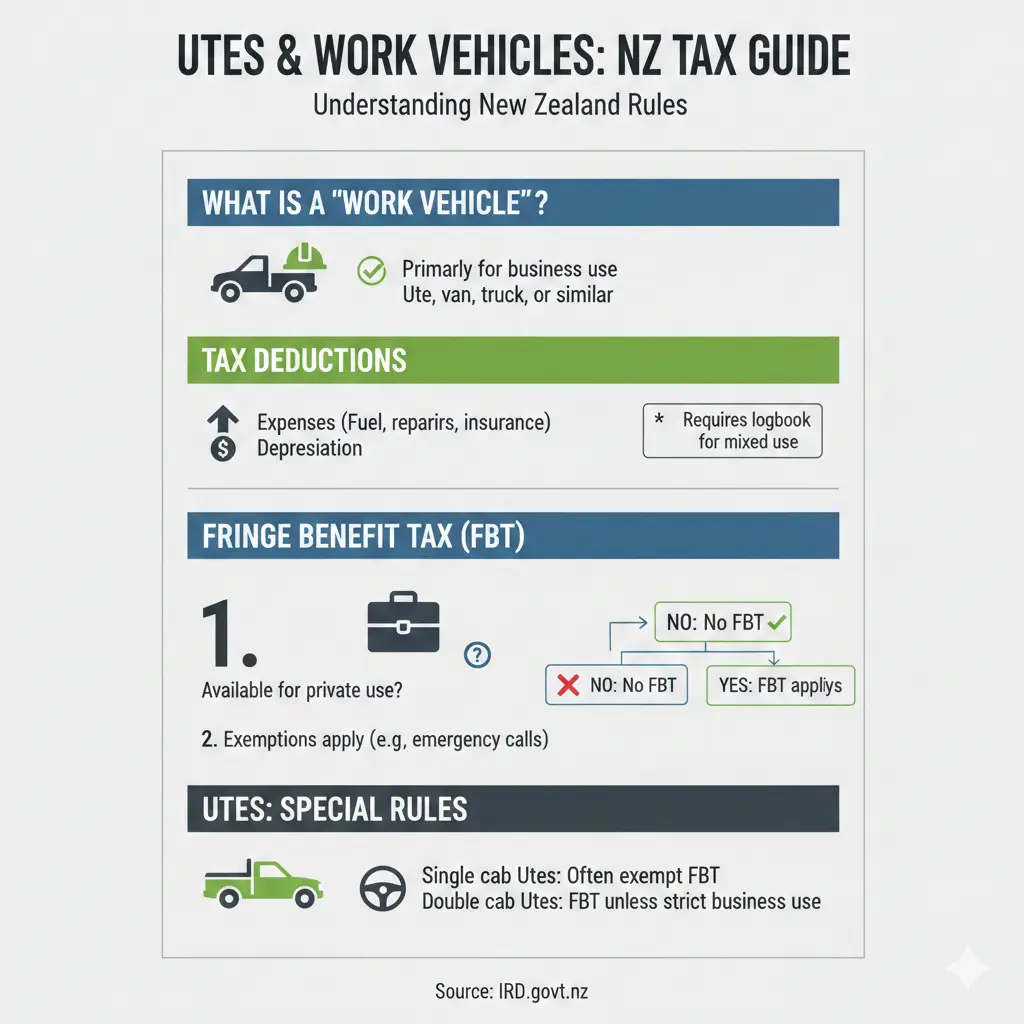

Understanding Utes and Work Vehicles in New Zealand

Utes—think double-cab pickups like the Mitsubishi Triton or Isuzu D-Max—are staples for Kiwi tradies, farmers, and small businesses. But for tax and FBT, not all utes qualify as "work vehicles." IRD defines a car as a motor vehicle with a gross vehicle mass (GVM) under 3,500kg (potentially rising to 4,500kg under proposals), designed to carry more than one person and goods under 1,000kg.

A true work-related vehicle must meet strict criteria for FBT exemption:

- Signwritten prominently with your business name and contact details.

- Private use prohibited, except for commuting to work sites (no weekend trips to the beach).

- Not classified as a "car"—single-cab utes often qualify, but double-cabs rarely do without modifications.

Double-cab utes are a hotspot of confusion. IRD clarifies they're treated like any vehicle: FBT applies unless fully compliant. Spot one at the boat ramp? That's private use, triggering tax.

Tax Depreciation for Utes and Work Vehicles

Good news for buyers: the Investment Boost Incentive accelerates depreciation on new assets, bringing forward tax deductions without changing the total over the asset's life. For a $80,000 ute, you could claim more upfront, boosting cashflow—perfect timing with 2026 rates.

From 2026, expect refined depreciation rules alongside FBT tweaks. Businesses are snapping up new utes now to maximise this.

Current FBT Rules for Work Vehicles

FBT taxes non-cash benefits like company ute private use at 63.93% (flat rate) or alternate rate (actual costs plus employee contributions). It's calculated quarterly, based on availability for private use—not just actual miles driven.

Exemptions hinge on "essential work purposes" per IRD's guide: vehicles used only for business tasks like deliveries or site visits, with logs proving no private jaunts. Commuting might slide if it's to the first job site, but home-to-site-and-back daily? That's taxable.

Common Pitfalls for Kiwi Businesses

- Myth of the FBT-free ute: Many assume all utes dodge FBT. Reality: double-cabs need full compliance.

- Day-counting hassle: Track every day of private availability—miss it, face penalties.

- Sole traders and partners: If you're paying yourself via the ute, FBT still applies unless exempt.

Real example: A Waikato farmer's signwritten single-cab ute hauling hay? Likely exempt. But his family's double-cab for school runs? Full FBT on private days.

Upcoming FBT Changes from 1 April 2026

Draft legislation eyes a revenue-neutral overhaul to slash compliance costs, ditching day-counts for a "close enough is good enough" vibe—ignoring incidental private use like grabbing milk post-job.

Key shifts include:

- New vehicle categories: Solely business (no FBT), predominantly business (65% discount), or unrestricted private (full tax).

- Deemed value rates: 26% for petrol/diesel utes (up from 20%), 22.4% hybrids, 19.4% EVs—reflecting running costs. A $50,000 ute? $13,000 taxable benefit yearly.

- Weight threshold up: Cars now to 4,500kg GVM, capturing more utes.

- No ute-specific rollback: Government ditched some radical ute proposals post-consultation, but core changes proceed.

Small businesses gripe: No discounts on vehicles over $80,000 could hit hard, unlike corporates. Implementation's tight—legislation might pass March 2026, so prep now.

Impact on Double-Cab Utes

No special treatment: They'll slot into categories based on use. Predominantly work? Discounts apply. Parked at the rugby? Full whack.

Tax Deductions and Strategies for Utes

Claim actual costs (fuel, repairs, rego) or logbook method for mixed use. For FBT, employee contributions (e.g., $50/week) reduce liability.

Practical tips:

- Log mileage religiously—apps like MilesTrackNZ simplify IRD audits.

- Signwrite boldly: "Joe's Plumbing – 021 123 456" on doors and tailgate.

- Prohibit private use in writing—employee handbook clause.

- Buy electric? Lower 19.4% rate from 2026 sweetens the deal.

- Time purchases: Grab now for boosted depreciation.

For fleets, alternate rate pooling cuts admin. Check IRD's IR409 guide for calculations.

Compliance Checklist for Kiwi Businesses

Stay IRD-proof with this 2026-ready checklist:

| Action | Why It Matters | Resource |

|---|---|---|

| Assess vehicle classification (ute vs car) | Avoids mis-exemption | IRD website |

| Implement logbooks or odometers | Proves business km | IR409 |

| Review employee contracts for use rules | Blocks private claims | Employment NZ |

| Calculate provisional FBT quarterly | Spreads payments | myIR portal |

| Plan for 26% diesel rate | Budgets new liability | Consult drafts |

Next Steps to Master Your Ute Tax Game

Don't let FBT blindside your business. Audit your vehicles today: classify them, log use, and model 2026 scenarios. Consult your accountant or use IRD's free tools—quarterly returns via myIR keep you ahead. With changes live soon, buying or tweaking now locks in benefits. Remember, this isn't advice—chat to a pro for your setup. Drive smart, stay compliant, and keep more in your pocket.

Disclaimer: Tax rules evolve; seek personalised advice from a qualified advisor or IRD. Rates current as of 2026.

Frequently Asked Questions

Sources & References

-

1

Utes & Fringe Benefit Tax - Leech & Partners Limited — www.leech.co.nz

-

2

No change to FBT rules for double cab utes - Inland Revenue — www.ird.govt.nz

-

3

FBT changes aim to cut compliance costs - CPA Australia — www.cpaaustralia.com.au

-

4

FBT Changes - McIsaacs — www.mcisaacs.co.nz

-

5

FBT changes, again. The confusion continues. - Cleaver Partners — cleaverpartners.co.nz

-

6

2025 NZ SME Tax Recap: Key Changes & 2026 Planning Guide - Andersen NZ — nz.andersen.com

-

7

Fringe benefit tax guide (IR409) - Inland Revenue — www.ird.govt.nz

-

8

Overview of FBT rules and exemptions relating to utility vehicles - Tax at Hand — www.taxathand.com

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...