How to Get Out of Debt: A Step-by-Step NZ Guide

Debt can feel overwhelming, but you're not alone—many Kiwis are juggling mortgages, personal loans, credit cards, and other financial commitments. The good news is that getting out of debt is entirely...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Debt can feel overwhelming, but you're not alone—many Kiwis are juggling mortgages, personal loans, credit cards, and other financial commitments. The good news is that getting out of debt is entirely possible with the right strategy and mindset. This guide walks you through practical, actionable steps to help you break free from debt and build a more secure financial future.

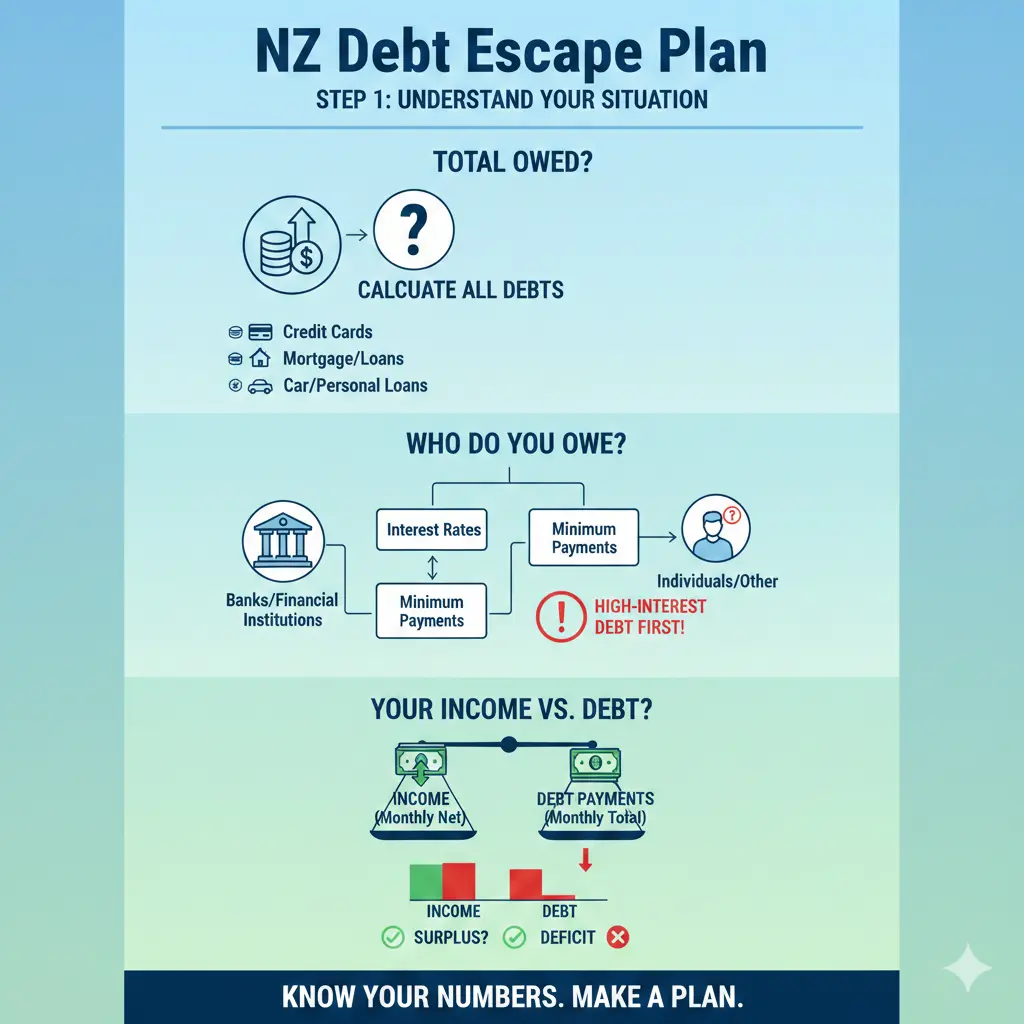

Understanding Your Debt Situation

Before you can tackle your debt, you need to understand exactly what you're dealing with. Start by listing every debt you have: credit cards, personal loans, mortgages, car loans, student loans, and any money owed to family or friends. For each debt, write down:

- The total amount owed

- The current interest rate

- The minimum monthly payment

- The payment due date

This exercise gives you a clear picture of your financial obligations and helps you identify which debts are costing you the most in interest. Understanding how interest rates influence your borrowing costs is crucial for managing debt effectively—fluctuations in these rates can dramatically impact your monthly payments and overall affordability.

Create a Realistic Budget

You can't escape debt without knowing where your money goes each month. Create a detailed budget that tracks your income and all expenses. Be honest about what you spend on groceries, utilities, transport, entertainment, and everything else. Once you've mapped out your spending, identify areas where you can cut back.

Many New Zealanders are struggling with rising costs and financial stress. The key is finding realistic ways to reduce spending without making your life miserable. Small cuts add up: cancelling unused subscriptions, reducing takeaway meals, or finding cheaper insurance can free up money to put towards debt repayment.

Choose a Debt Repayment Strategy

There are two main approaches to paying off multiple debts:

The Snowball Method

Pay off your smallest debts first while making minimum payments on larger ones. This approach builds momentum and gives you quick wins, which can be psychologically motivating. Once you've cleared a small debt, you redirect that payment towards the next smallest debt, creating a "snowball" effect.

The Avalanche Method

Focus on debts with the highest interest rates first, regardless of the balance. This approach saves you the most money in interest over time, making it mathematically efficient. Since interest rates significantly influence the cost of borrowing, targeting high-interest debt first can substantially reduce your total repayment amount.

Choose whichever method keeps you motivated. The best strategy is the one you'll actually stick with.

Explore Refinancing Options

If you have high-interest debts, refinancing could lower your monthly payments. For example, if you have multiple credit cards at high rates, you might consolidate them into a single personal loan at a lower rate. This simplifies your payments and reduces the total interest you'll pay.

Keep an eye on interest rate changes. The anticipated drop in the Official Cash Rate (OCR) to approximately 2.25% by February 2026 may shape future borrowing conditions, potentially creating opportunities to refinance at better rates. A decrease in the OCR can significantly lower monthly payments on credit, making it more attractive to refinance existing debts.

Consider Debt Management Options in New Zealand

If you're struggling to manage your debts, New Zealand offers several formal options:

Debt Management Plans

You can combine your debts into a debt management plan or enter into a proposal with your creditors. This allows you to negotiate more manageable payment terms directly with those you owe money to.

Professional Support

If negotiations aren't working, consider speaking with a financial adviser or contacting a community law centre. Many offer free or low-cost advice to help you understand your options and develop a realistic repayment plan.

Increase Your Income

Paying off debt faster doesn't always mean spending less—it can also mean earning more. Consider:

- Asking for a pay rise at work

- Taking on a side hustle or freelance work

- Selling items you no longer need

- Renting out a spare room

Even an extra $50–100 per week directed towards debt can make a significant difference over time.

Avoid Taking on New Debt

While you're paying off existing debt, it's crucial to avoid accumulating new debt. This means:

- Using cash or debit rather than credit cards

- Avoiding impulse purchases

- Building a small emergency fund so unexpected expenses don't force you back into debt

- Being cautious with buy-now-pay-later services

Breaking the cycle of debt requires changing behaviours and financial habits. By being intentional about your spending, you'll move forward and lower your financial stress.

Track Your Progress

As you pay off debts, celebrate your wins. Whether you're using a spreadsheet, an app, or a simple chart on your fridge, tracking progress keeps you motivated. Seeing your debts shrink over time reinforces that your efforts are working.

If you're using personal loans, tools like loan payback calculators can help you understand your payment alternatives and associated fees, ensuring transparency in your expenses. Understanding exactly what you're paying helps you make informed decisions about your debt repayment strategy.

Your Path Forward

Getting out of debt requires patience, discipline, and a solid plan—but it's absolutely achievable. Start by understanding exactly what you owe, create a realistic budget, and choose a repayment strategy that works for your situation. Remember that small, consistent progress adds up over time.

As you move forward, stay informed about changes in interest rates and refinancing opportunities. Keep your focus on the bigger picture: financial freedom and the peace of mind that comes with being debt-free. You've got this.

Frequently Asked Questions

Sources & References

- 1

-

2

10 Things to Do Differently with Money in 2026 - MoneyHub NZ — www.moneyhub.co.nz

-

3

Debt Management Plans and Proposals — www.insolvency.govt.nz

Related Articles

The "No-Spend" Month: How One Kiwi Saved $2;000 in 30 Days

Imagine looking at your bank account at the end of the month and seeing an extra $2,000 staring back at you—all because you said "no" to impulse buys, takeaways, and those sneaky coffee runs. That's e...

How to Calculate Your Take-Home Pay with the NZ Salary Calculator

Ever wondered why your bank account doesn't match that shiny new job offer? You're not alone—many Kiwis scratch their heads over the gap between gross salary and actual take-home pay. With New Zealand...

Budgeting for Beginners: The "50/30/20 Rule" Adjusted for NZ Salaries

Struggling to make your Kiwi paycheck stretch further? You're not alone—many of us feel the pinch from rising rents, grocery bills, and that tempting flat white habit. But what if a simple rule could...

How to Travel the World on a NZ Salary

Ever dreamed of sipping cocktails on a Thai beach or exploring the ancient ruins of Machu Picchu, all while earning a solid Kiwi wage? With New Zealand's average monthly salary hitting 5,666 NZD in 20...