Automatic Payments vs Direct Debits NZ: Understanding the Difference

If you've ever set up a regular payment for rent, power, or gym fees, you've likely encountered two terms: automatic payments and direct debits. While they might sound similar—and both involve money l...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

If you've ever set up a regular payment for rent, power, or gym fees, you've likely encountered two terms: automatic payments and direct debits. While they might sound similar—and both involve money leaving your account regularly—they work quite differently. Understanding the distinction is crucial because it affects your control over payments, how much flexibility you have, and your rights if something goes wrong. Let's break down what separates these two payment methods and help you choose the right one for your situation.

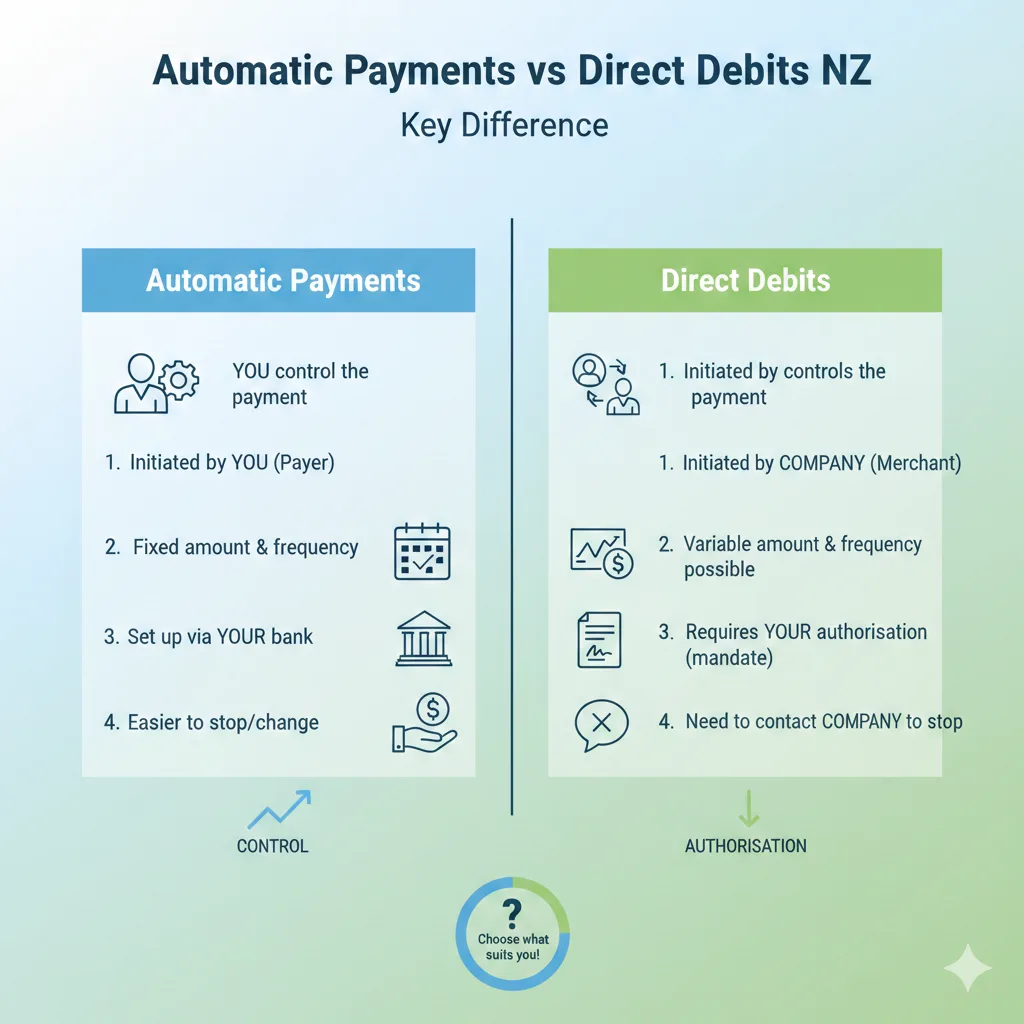

What's the Key Difference?

The fundamental difference comes down to control. An automatic payment is a regular payment that you set up and control—you're in charge of the amount and timing. A direct debit, on the other hand, is a payment arrangement that you approve but the business controls. The business can adjust the amount with each payment, and they handle the administration on their end.

Think of it this way: with an automatic payment, you're pushing money out of your account. With a direct debit, you're giving someone permission to pull money from your account.

Understanding Automatic Payments

How Automatic Payments Work

Automatic payments are set up entirely by you through your bank's online banking platform. You decide the amount, the frequency, and the date the payment should be made. This gives you complete control over your outgoings.

You might set up an automatic payment to go out every second Thursday because that's when you get paid—ensuring you'll have funds available. You can change the amount or cancel the payment whenever you like, and you don't need anyone's permission to do so.

Your Rights with Automatic Payments

Since you're controlling automatic payments, you're responsible for keeping them accurate. If the amount you're paying changes—say your rent increases or your child's childcare fees go up—you'll need to manually update the payment amount yourself.

If you don't have enough money in your account when an automatic payment is due, it typically won't process. Your bank might attempt the payment a few times, but if it fails, you could be charged a penalty fee. It's your responsibility to ensure sufficient funds are available.

You can change or cancel an automatic payment at any time through your online banking, with no need for approval from the business you're paying.

When Automatic Payments Make Sense

Automatic payments work well when:

- The payment amount stays the same each time

- You want full control over the payment

- You prefer to manage your payments yourself

- The amount rarely changes

Understanding Direct Debits

How Direct Debits Work

A direct debit is an agreement between you and a business that allows them to take regular payments from your bank account. You give your approval upfront—usually by signing an authorisation form—and the business handles the rest.

The amount can stay the same each time (like a gym membership) or vary with each payment (like a power bill). Because you're not doing anything, a direct debit significantly reduces the chance of missing a payment.

Your Rights with Direct Debits

When you set up a direct debit, the business must notify you in advance about the amount and date of each payment. This gives you visibility into what's coming out of your account.

One of the key advantages of direct debits is that the business adjusts variable amounts automatically and notifies you at least 10 working days before the amount changes. For example, if your power company needs to adjust your bill, they'll let you know in advance.

You can cancel a direct debit at any time by contacting your bank—you don't need permission from the business, though you should let them know. However, you're still responsible for paying any money you actually owe through another method.

If there aren't sufficient funds in your account when a direct debit is due, your bank can either make the payment and charge overdraft fees, or dishonour it and charge a dishonour fee.

When Direct Debits Make Sense

Direct debits work well when:

- The payment amount changes regularly (like utility bills)

- You want the business to manage payment administration

- You prefer not to manually update amounts

- You want advance notice of payment changes

Direct Debits vs Automatic Payments: A Practical Comparison

| Feature | Automatic Payment | Direct Debit |

|---|---|---|

| Who controls it? | You | The business (with your approval) |

| Who sets it up? | You, through online banking | The business, with your signed authorisation |

| Fixed or variable amount? | Fixed—you pay the same amount each time | Can be fixed or variable |

| Who updates the amount? | You must manually update it | The business updates it and notifies you |

| Cancellation | You can cancel anytime through your bank | You can cancel anytime through your bank |

| Advance notice of changes? | No—you need to monitor the bill yourself | Yes—at least 10 working days' notice |

| Best for | Fixed, regular payments | Variable or frequently changing payments |

Real-World New Zealand Examples

Example 1: Power Bills

Your power company sends you a bill each month for varying amounts depending on your usage. A direct debit works perfectly here because the amount changes regularly, and the power company will notify you of increases in advance. If you used an automatic payment, you'd need to manually update the amount each month—and if you forget, you might fall behind on payments.

Example 2: Gym Membership

Your local gym charges a fixed $25 per week. Either payment method works, but an automatic payment gives you more control. You can easily cancel it whenever you like through your online banking. With a direct debit, you'd still need to contact your bank to stop it (though you don't need the gym's permission).

Example 3: Council Rates

If you're paying Bay of Plenty Regional Council rates, they recommend setting up a direct debit rather than an automatic payment. With a direct debit, the council calculates your payments across the year to 30 June, and you don't have to worry about manually monitoring your rates account or ensuring you clear your balance by specific deadlines.

Important: 7-Day Payment Processing in New Zealand

Since 26 May 2023, New Zealand banks have enabled 7-day payment processing for domestic electronic payments. This means both automatic payments and direct debits can now be processed on weekends and public holidays—not just business days.

This is important because you need to ensure you have sufficient funds in your account on the due date, including Saturdays, Sundays, and public holidays. If a direct debit or automatic payment is due on a Saturday, the money will be deducted that day, not on the following Monday.

Frequently Asked Questions

Can I cancel a direct debit without the business's permission?

Yes. You can ask your bank to cancel a direct debit at any time, and the bank must act on your instructions. You don't need approval from the business you're paying. However, you should notify the business so they know the payment arrangement has ended, and remember that you're still responsible for paying any money you actually owe them.

What happens if I don't have enough money for a direct debit?

Your bank has two options: they can process the payment anyway and charge you overdraft fees or interest, or they can dishonour the payment, in which case you'll need to arrange payment separately and may be charged a dishonour fee. Make sure you have sufficient funds on the due date.

Can I change an automatic payment amount?

Yes, absolutely. You can change the amount of an automatic payment at any time through your online banking. There's no need to contact the business you're paying or your bank—you have full control.

Which is better for bills that change regularly?

A direct debit is better for variable bills like power or phone because the business adjusts the amount and notifies you in advance. With an automatic payment, you'd need to manually update the amount each time, which is easy to forget.

Do I need a signed form for an automatic payment?

Your bank will need a signed form from you (or someone authorised to sign on your behalf) to set up an automatic payment. However, once it's set up, you can manage it entirely through your online banking.

Can a business change a direct debit amount without telling me?

No. A business must notify you in advance of the amount and date of each direct debit payment. For variable amounts, they must give you at least 10 working days' notice before the amount changes.

Making Your Choice

Choosing between automatic payments and direct debits depends on your situation:

Choose an automatic payment if: You're paying a fixed amount regularly and want complete control. You prefer managing everything through your online banking and don't mind updating amounts when they change.

Choose a direct debit if: The payment amount varies regularly. You want the business to handle administration and notify you of changes. You prefer a "set and forget" approach with advance notice of any changes.

For most New Zealand households, direct debits are ideal for utilities, insurance, and subscription services where amounts change. Automatic payments work well for fixed-amount payments like rent or gym memberships where you want maximum control.

Whatever you choose, remember to monitor your bank account regularly, ensure you have sufficient funds on payment dates (including weekends), and keep your bank informed of any changes to your bank account details. Both payment methods are secure and convenient—the key is picking the right one for your needs.

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...