Excess Options Explained: Choosing Your Insurance Excess

When a claim hits, the last thing you want is an unexpected bill from your own insurer. That's where insurance excess comes in – it's the amount you pay upfront before your policy kicks in, and choosi...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

When a claim hits, the last thing you want is an unexpected bill from your own insurer. That's where insurance excess comes in – it's the amount you pay upfront before your policy kicks in, and choosing the right one can save you hundreds on premiums or leave you out of pocket when disaster strikes.

For Kiwis, understanding excess options is crucial in a country prone to earthquakes, floods, and everyday mishaps like car dings or burst pipes. With rising living costs in 2026, balancing affordable cover with manageable out-of-pocket expenses is more important than ever. This guide breaks down excess types, how they work across car, home, contents, and health insurance, and actionable steps to pick the best option for your budget.

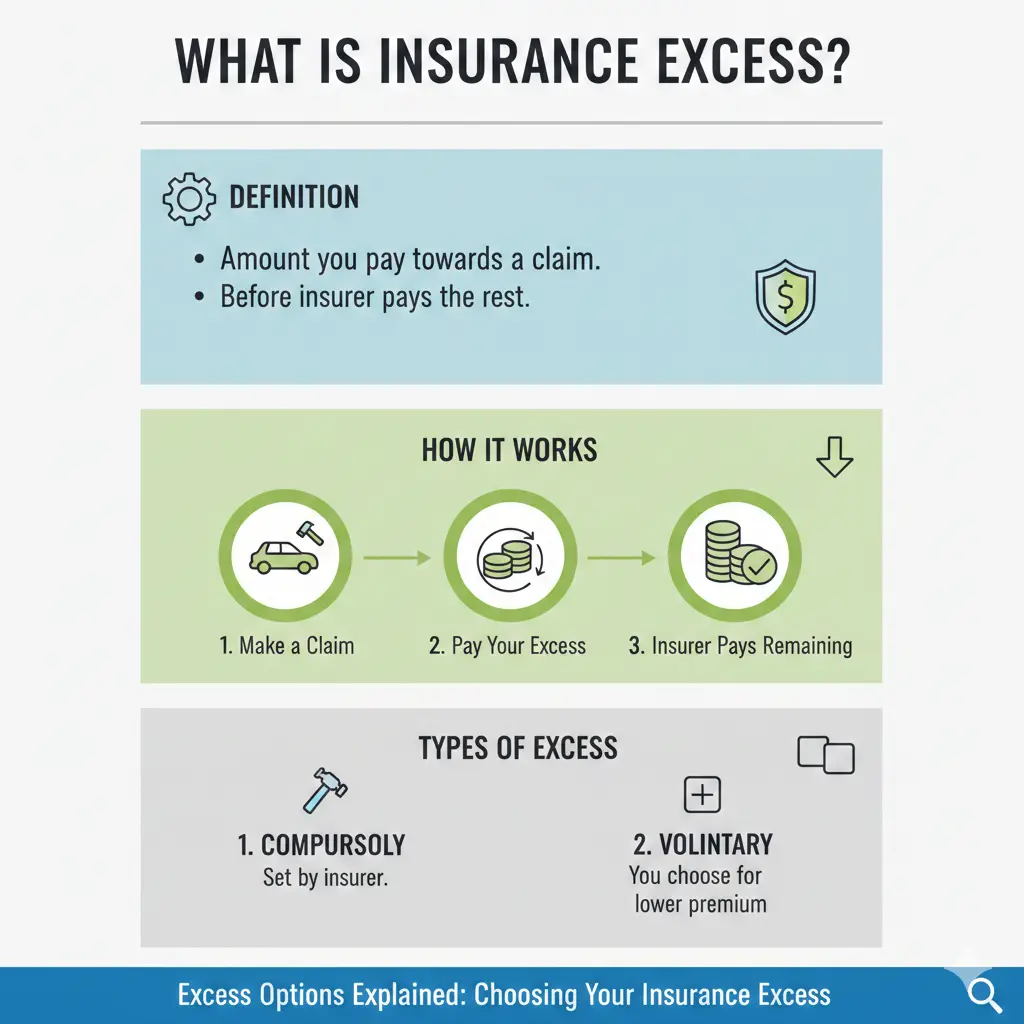

What is Insurance Excess?

Insurance excess is the fixed amount you contribute towards a claim before your insurer pays the rest, up to your policy limit. It's not tied to fault – even if someone else caused the damage, you'll often pay it upfront, though it might be reimbursed later.

Think of it like a co-pay: for a $1,000 car repair with a $400 excess, you pay $400 and your insurer covers $600. Excesses apply per event, not per policy or claim. If a fire damages both your house and contents, you might pay two excesses – unless your insurer applies a "one event, one excess" rule, taking the highest amount.

Why Do Insurers Charge Excess?

Excesses discourage small claims, keeping premiums lower for everyone, and cover administrative costs. They also share risk: higher excesses mean lower premiums, as you're handling minor fixes yourself.

Types of Excess in New Zealand Insurance

New Zealand insurers like AA, Tower, and Vero offer several excess types. Your policy documents list the details, and they're cumulative – meaning they add up.

Standard Excess

This is the minimum set by your insurer, often $400-$500 for car insurance. It varies by policy type: home might be $500, contents $250. You can't go below it without special approval, like for low-risk drivers.

Voluntary Excess

Boost your standard excess voluntarily to cut premiums. Add $100-$1,000 (or more) on top – up to $1,400 for cars or $2,000 for landlord properties. For an Auckland Suzuki Swift (market value $5,000), raising from $400 to $1,000 dropped quotes from $629 to $475 annually across insurers.

| Insurer | $400 Excess | $500 Excess | $750 Excess | $1,000 Excess |

|---|---|---|---|---|

| Example 1 | $629.45 | $595.97 | $529.00 | $475.42 |

| Example 2 | $620.56 | $559.48 | $528.93 | $498.39 |

Higher voluntary excess suits claim-free Kiwis with savings buffers.

Imposed or Additional Excess

Insurers hike excesses for higher risks. Common triggers:

- Young drivers: Tower adds $750 (under 21), $500 (21-24); AA $550 (listed under 25) or $2,500 (unlisted).

- Inexperienced drivers: $500 if 25+ with <2 years' experience.

- At-fault claims: $250+ for two in two years.

- Property types: Extra for rentals or quake-prone areas.

- International licences: $1,000.

Total could hit $1,250 ($500 standard + $750 young driver).

Health and Other Excesses

Health policies let you set excesses for hospital stays or surgery, slashing premiums by sharing risk. Rental car excess is often $1,000-$3,000, covering damage before supplier insurance applies.

How Excess Affects Your Premiums and Claims

Higher excess = lower premiums, but only claim if damage exceeds it. A $10,000 kitchen claim with $2,000 excess ($400 premium saving) nets you $1,100 worse off after paying extra $1,600.

Reimbursement Possibilities

If another party's at fault (e.g., hit-and-run identified), insurers like Vero may recover your excess. Success depends on witnesses, admission, and their insurance – not guaranteed.

Multiple Policies or Events

Separate events mean separate excesses: tenant damages carpet and window? Two payments. Single-event multi-policy claims might cap at the highest excess.

Choosing the Right Excess for You

Match excess to your finances, risk, and claim history. Here's how:

Assess Your Risk Profile

- Low-risk (older drivers, secure homes): Opt for $750-$1,500 voluntary to save 20-30% on premiums.

- High-risk (young drivers, rentals): Stick to standard; imposed extras apply anyway.

- Landlords: $1,150-$2,000 common for portfolios, if you self-fund repairs.

Financial Check: Can You Afford It?

Ensure liquid savings cover 1.5x your excess. IRD data shows median Kiwi household savings at $10,000 (2026), so $500-1,000 is feasible for most. Use emergency funds or KiwiSaver withdrawals (check rules via ird.govt.nz).

Practical Tips for Kiwis

- Review annually: Shop via MoneyHub or Canstar for 2026 quotes.

- Bundle policies: Houses & contents from one insurer might waive one excess.

- Add-ons: Windscreen ($0 excess) or roadside for cars.

- Quake prep: EQC (now part of government scheme) has $1,500 building excess (2026 rates).

- Negotiate: Long no-claims? Ask for excess waivers.

Pro tip: Simulate claims: If average repair is $800, $1,000 excess means self-pay most – ideal if handy.

Common Mistakes to Avoid

- Ignoring policy fine print: Always check PDS for hidden extras.

- Over-volunteering without savings: 30% of claims under $1,000 in 2025 per ICNZ.

- Forgetting per-event rule: Budget for multiples in disasters.

- Not updating for life changes: New teen driver? Adjust now.

Frequently Asked Questions

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...