Joint vs Individual Bank Accounts: What Couples Should Know

Imagine this: you're building a life together in New Zealand, splitting rent in Auckland, saving for a KiwiSaver boost towards that first home, or just trying to keep up with rising grocery bills. But...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine this: you're building a life together in New Zealand, splitting rent in Auckland, saving for a KiwiSaver boost towards that first home, or just trying to keep up with rising grocery bills. But when it comes to money, one question looms large—should you merge your finances into a joint bank account, keep them strictly individual, or do a bit of both? For Kiwi couples, the choice between joint vs individual bank accounts isn't just about convenience; it's about trust, legal responsibilities, and protecting your financial future under New Zealand law.

In 2026, with cost-of-living pressures squeezing households from Wellington to Dunedin, more couples are rethinking how they handle shared expenses like power bills, Netflix subscriptions, or even mortgage repayments. This guide breaks it all down—what works, what doesn't, and practical steps tailored for Kiwis. Whether you're de facto, married, or somewhere in between, understanding these options helps you avoid nasty surprises, like joint liability for overdrafts or disputes during separations.

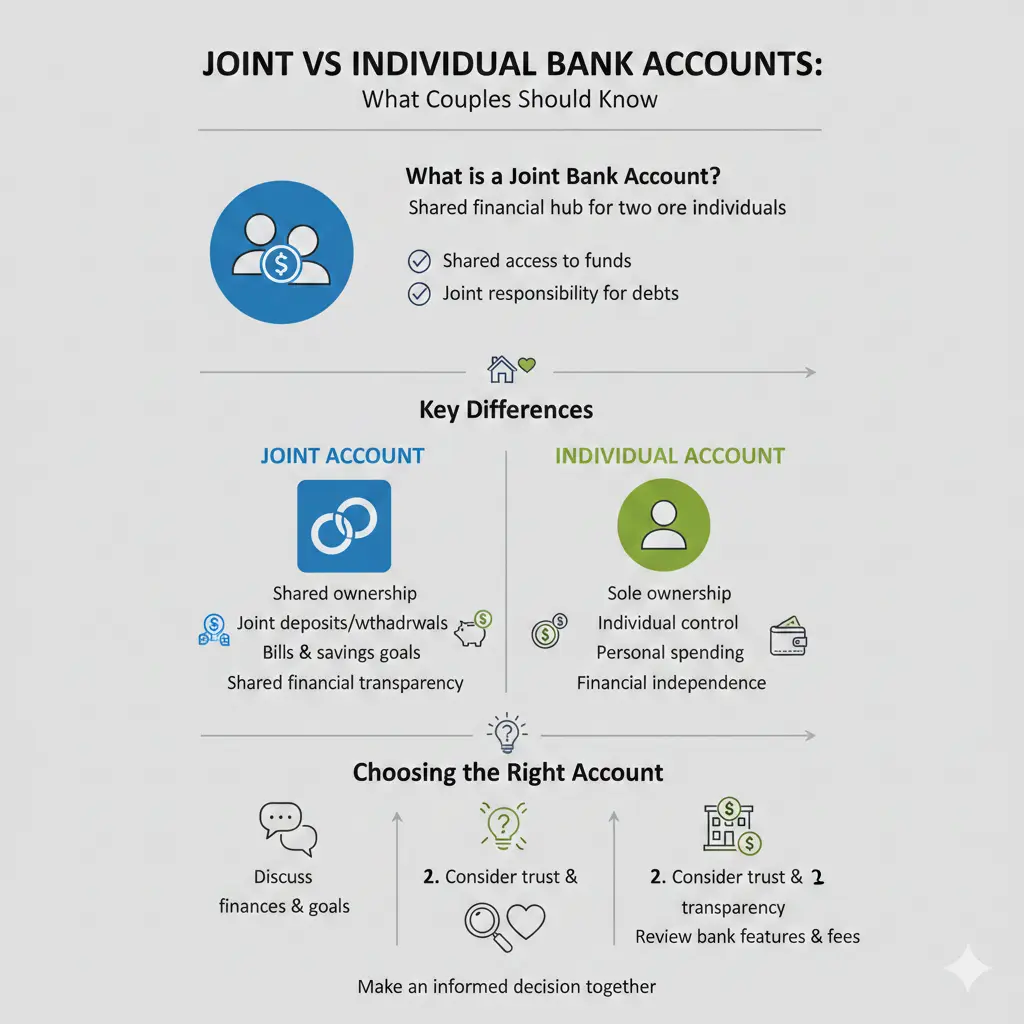

What is a Joint Bank Account?

A joint bank account lets two or more people—typically couples—share ownership of the funds. Everyone named on the account can usually access it fully, whether that's withdrawing cash at an ATM, paying bills via internet banking, or making deposits through the ASB Mobile app or similar tools from other banks. It's common for Kiwis sharing living expenses, saving for a family holiday, or pooling resources for a house deposit.

But it's not all seamless. All owners are individually and jointly liable for any debts, like overdrafts. If one partner racks up fees or an overdrawn balance, the others could foot the bill—even if they didn't authorise it. Plus, upon death, the funds automatically pass to the surviving owner(s), bypassing probate, which can be a pro or con depending on your estate plans.

How Joint Accounts Work in New Zealand Banks

Major Kiwi banks like ASB, ANZ, BNZ, Kiwibank, and Westpac offer joint accounts for transaction, savings, credit cards, and even investments. Here's the nuts and bolts:

- Full Access by Default: Any holder can deposit, withdraw, or transfer funds freely via apps, FastNet, EFTPOS, or branches.

- Optional Restrictions: Some banks let you limit withdrawals or transfers unless all agree—handy for added security. Ask your bank about daily limits to prevent fraud.

- Shared Ownership: Money deposited belongs to everyone; you can't claim "mine" if things go south.

- Joint Liability: Debts are everyone's problem. Even if you're removed from the account, you're liable for prior debts until cleared.

To open one, visit a branch (most require it). Bring two forms of ID—like a NZ driver's licence and passport—plus proof of address, such as an IRD statement or power bill. New customers might need to go together or separately, but everyone must verify identity.

Individual Bank Accounts: Keeping It Personal

With an individual bank account, the money is yours alone. You control deposits, withdrawals, and spending without anyone else's input. This setup suits Kiwis who value financial independence, perhaps one partner on a variable income from freelancing or seasonal work in tourism.

Pros include total privacy—no explanations needed for that impulse buy at The Warehouse—and sole responsibility for debts. But for couples, it means tracking shared bills manually, like splitting the council rates or ACC levies via apps like Splitwise.

Relationship Property Laws in New Zealand

Don't assume separate accounts keep money separate forever. Under the Property (Relationships) Act 1976, individual accounts can still be classified as relationship property if built during the partnership, subject to equal division on separation (after 3+ years de facto or marriage). Talk to a lawyer via the New Zealand Law Society for advice on trusts or contracting out agreements to protect assets.

Joint vs Individual Bank Accounts: Pros and Cons for Kiwi Couples

Choosing between joint vs individual bank accounts depends on your relationship stage, income levels, and goals. Many couples opt for a hybrid: joint for bills, individual for fun money.

Advantages of Joint Accounts

- Simplified Shared Expenses: Pay rent, groceries, or power from one pot—ideal amid 2026's inflation.

- Fee Savings: One account means one set of fees, not two.

- Transparency and Teamwork: Both see the balance, reducing arguments over who's paid the Spark bill.

- Business-Like Efficiency: Great for unequal incomes—contribute proportionally to a joint account for 50/50 expense splits.

Disadvantages of Joint Accounts

- Risk of Abuse: One partner could drain it, leading to financial harm. Set limits and monitor.

- No Privacy: Every purchase is visible.

- Joint Debt Exposure: Overdrafts or credit card debts bind everyone.

- Separation Hassles: Closing requires all to agree; funds split evenly, regardless of contributions.

Advantages of Individual Accounts

- Independence: Spend guilt-free on personal KiwiSaver top-ups or hobbies.

- Protection: Your money stays safe from a partner's poor choices.

- Flexibility: Easier for WINZ benefits or StudyLink payments tied to one person.

Disadvantages of Individual Accounts

- Administrative Burden: Track reimbursements for shared costs like petrol or rates.

- Potential Inequality: One partner might shoulder more, breeding resentment.

- Legal Grey Areas: Still divisible under relationship property rules.

| Feature | Joint Accounts | Individual Accounts |

|---|---|---|

| Access | Full for all holders | Sole owner only |

| Liability | Joint & individual | Personal only |

| Best For | Shared bills, goals | Privacy, independence |

| Separation | Funds split evenly | Potentially relationship property |

Best Practices for Couples in New Zealand

Go hybrid: Keep individual accounts for personal spending (say, 70% of income) and a joint one for bills (30%). Agree upfront—what goes in? Power, internet, groceries? Use auto-payments from the joint account to avoid missed IRD payments or ACC claims.

Practical Tips

- Discuss Contributions: Proportional to income—e.g., if one earns $80k and the other $60k, contribute 57%/43%.

- Set Rules: No withdrawals without notice; use apps like BNZ's for shared visibility.

- Protect Against Harm: Get financial mentoring from Good Shepherd or bank advisors.

- Review Regularly: Annually, or after life changes like a baby or job loss via WINZ.

- Plan for Breakups: Know joint accounts must be closed mutually; shift autos to individuals fast.

Opening and Managing Accounts

Compare banks: ANZ and BNZ allow online apps with RealMe; ASB and Kiwibank prefer branches. Factor in 2026 fees—no-fee options like Kiwibank's basic account suit low-balances.

Legal Considerations for Kiwis

Joint accounts mean shared liability forever on old debts. For separations, freeze joint access and consult Community Law Centres. Relationship property divides equally, but separate accounts aren't immune. Consider KiwiSaver splits too—IRD rules apply.

"Money in individual bank accounts could still be considered relationship property under the law."

Next Steps for Your Finances

Chat with your partner tonight: list shared expenses, pick a bank, and set up accounts this week. Visit ird.govt.nz for tax implications, or good shepherd.org.nz for free advice. Remember, this isn't personalised financial advice—consult a certified adviser or lawyer for your situation. Strong finances build stronger relationships; get it right for your Kiwi dream.

Frequently Asked Questions

Sources & References

-

1

Joint bank accounts in NZ - Guide | ASB — www.asb.co.nz

-

2

Best Joint Bank Accounts - MoneyHub NZ — www.moneyhub.co.nz

-

3

Joint or separate bank accounts - Good Shepherd NZ — goodshepherd.org.nz

-

4

Joint or separate finances? - Good Shepherd NZ — toolkit.goodshepherd.org.nz

- 5

-

6

Five steps to help you through financial separation | Westpac NZ — www.westpac.co.nz

-

7

How couples can play equal roles on different incomes - BNZ — www.bnz.co.nz

-

8

Relationship breakdowns and banking - Bank Ombudsman — bankomb.org.nz

Related Articles

Working Multiple Jobs NZ: Tax and Legal Considerations

Juggling multiple jobs can boost your income, but it's crucial to understand the tax implications and legal requirements that come with working more than one role in Aotearoa. Whether you're a contrac...

Name Changes NZ: Legal Process and Costs

Considering a fresh start with a new name? Whether it's after marriage, divorce, or simply embracing a personal transformation, changing your name in New Zealand is straightforward but requires follow...

Holiday Home Tax Rules NZ: Private Use and Rental

Own a bach in Coromandel or a holiday home in Queenstown? You're not alone—many Kiwis cherish these escapes, but renting them out while enjoying personal use can trip you up on tax rules. Getting the...

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...