KiwiSaver Contribution Holiday: Taking a Break from Payments

Feeling the pinch with KiwiSaver deductions eating into your paycheck? A KiwiSaver contribution holiday could be the relief you need, letting you pause those compulsory payments without derailing your...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Feeling the pinch with KiwiSaver deductions eating into your paycheck? A KiwiSaver contribution holiday could be the relief you need, letting you pause those compulsory payments without derailing your long-term savings goals. Whether you're facing financial hardship or simply want a breather after years of steady contributions, understanding how to take a break from payments is key for Kiwis navigating 2026's changing rates.

In this guide, we'll break down everything you need to know about applying for a KiwiSaver contribution holiday, from eligibility and the process to what happens during and after your break. With employer contributions rising to 3.5% from 1 April 2026, and further changes ahead, timing your holiday right can help manage your cash flow effectively.

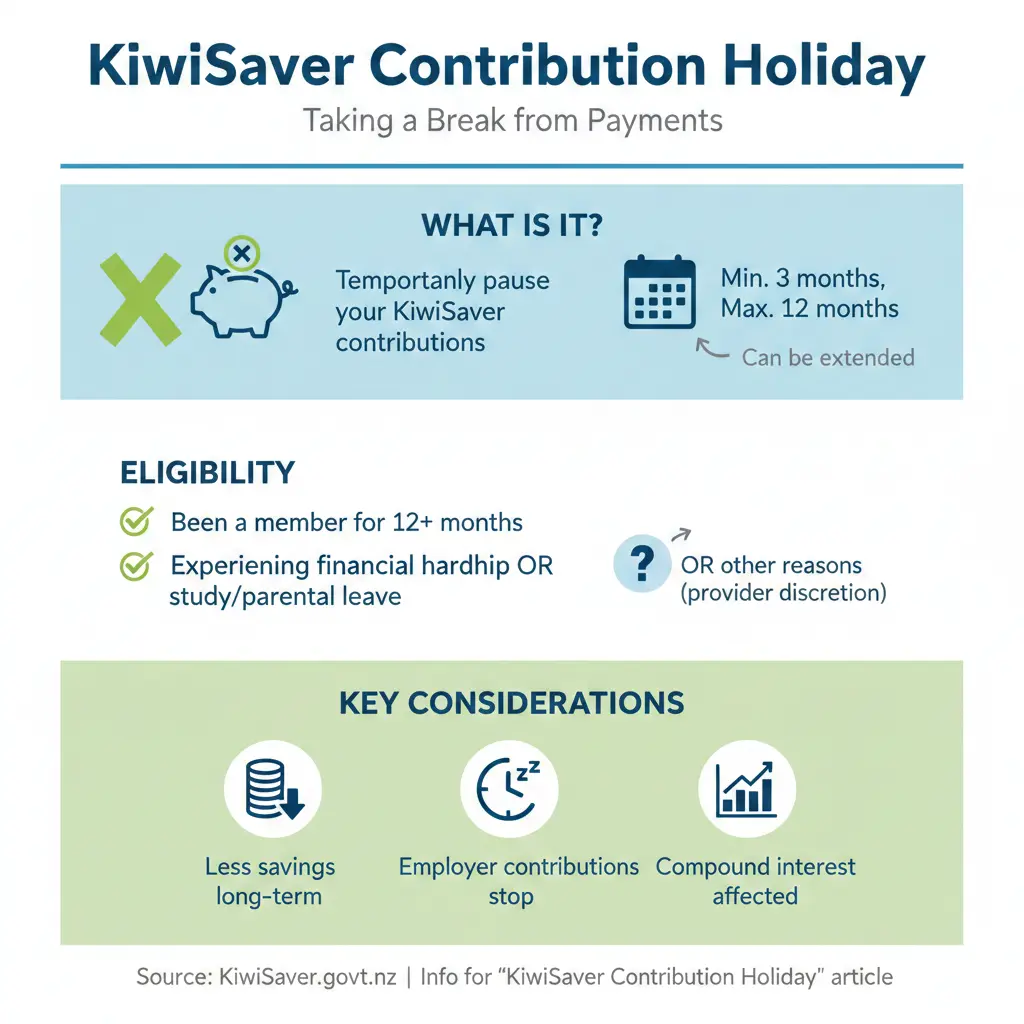

What is a KiwiSaver Contribution Holiday?

A KiwiSaver contribution holiday, also called a savings suspension, allows eligible members to temporarily stop compulsory deductions from their salary or wages. This means no more employee contributions coming out of your pay packet during the holiday period, giving you immediate relief on everyday expenses like rent, groceries, or unexpected bills.

Importantly, while your contributions pause, your employer must still make their compulsory contributions—rising to 3.5% of your gross salary from 1 April 2026 (and 4% from 1 April 2028). Government contributions also continue if you make any voluntary top-ups, though the rate drops to 25 cents per dollar from 1 July 2026, with a maximum of $260.72 annually.

Key Benefits of Taking a Break

- Cash flow boost: Free up 3-10% of your gross pay (depending on your rate) for other priorities.

- Flexibility: Ideal during job changes, family expansions, or economic squeezes.

- No penalty on growth: Your existing balance keeps growing with investment returns and employer/government contributions.

- Multiple holidays allowed: You can apply for several, as long as each meets the minimum three-month term.

Real Kiwi example: Joyce, a part-time worker with two jobs, took a one-year holiday after two years of contributions. Her employers stopped deductions, easing her budget without losing employer super top-ups.

Who is Eligible for a KiwiSaver Contribution Holiday?

Not everyone can hit pause straight away. Under the KiwiSaver Act 2006 (Part 3, Subpart 4), you must meet specific timelines and criteria.

Standard Eligibility

- At least 12 months since your first KiwiSaver contribution was received by Inland Revenue (IRD) or your provider.

- No active holiday already in place—you can't stack them.

Financial Hardship or Serious Illness

If you're suffering (or likely to suffer) financial hardship, you can apply immediately after your first contribution. IRD provides guidelines on what qualifies, such as job loss, high medical costs, or debt pressures. Serious illness also fast-tracks approval.

Note: From 1 February 2026, if you're on a temporary rate reduction due to the upcoming 3.5% hike (effective 1 April), you can't take a holiday simultaneously.

How to Apply for a KiwiSaver Contribution Holiday

Applying is straightforward via IRD. You can submit by any accepted method, like online through myIR, post, or phone.

Step-by-Step Application Process

- Gather details: Your name, address, IRD number, employer names/addresses, desired holiday length, and hardship details (if applicable).

- Submit to IRD: Log into myIR or contact IRD directly. No specific form needed—just the required info.

- Wait for approval: IRD must grant if criteria are met, usually quickly.

- Receive notices: IRD notifies you, your employer(s), and KiwiSaver provider. Employers stop deductions from your next pay.

Example: Jin, facing hardship, showed his employer the IRD letter, and deductions halted immediately, with a refund for any overpaid contributions.

Duration Rules

- Financial hardship: Minimum 3 months; longer if IRD agrees.

- Standard holiday: 3 months minimum, up to 5 years maximum (or as requested, whichever shorter).

- No less than 3 months: Unless your employer consents to a shorter period.

Providers like AMP note holidays typically last 3-12 months, but IRD rules allow longer.

What Happens During Your Contribution Holiday?

Once approved:

- Your employee contributions stop—no deductions from wages.

- Employers continue compulsory contributions at 3.5% (from April 2026).

- Your KiwiSaver balance invests as usual, potentially growing.

- You can still make voluntary contributions via direct debit or lump sums to snag government top-ups.

Pro tip: Use the extra cash wisely—pay down high-interest debt or build an emergency fund with ACC or WINZ support if needed.

Ending or Revoking Your KiwiSaver Contribution Holiday

Holidays don't auto-renew forever. Here's how it wraps up:

Automatic End

IRD sends notice to you and your employer(s) before expiry, specifying the restart date. Deductions resume on the next calculated pay after notice.

Example: Mohammad's three-year holiday ended with IRD notice; he applied for another seamlessly.

Early Revocation

- Notify your employer directly with a KS2 form or written request.

- Deductions start next pay cycle.

- Can't revoke below 3 months without employer OK.

If switching jobs, provide new employer your IRD holiday letter or KS2.

2026 KiwiSaver Changes and Contribution Holidays

Big shifts are here: Default rates rise to 3.5% for employees and employers from 1 April 2026, then 4% from 1 April 2028.

Temporary Rate Reductions

Can't swing 3.5%? Apply via myIR from 1 February 2026 for a temp drop to 3% (effective 1 April). Show employer the certificate. Employers match at reduced rate initially but must hit 3.5% on rate hikes.

But no holidays during rate reductions—choose one or the other.

Government Contribution Tweaks

From 1 July 2026: 25c per $1 (max $260.72/year), down from 50c/$521.43. Eligibility extends to 16-17-year-olds.

Practical Tips for Kiwis Considering a Holiday

- Assess impact: Use IRD's KiwiSaver calculator to model balance growth sans your contributions.

- Voluntary top-ups: Aim for $1,042.88/year pre-1 July to max government contrib.

- Multiple employers: List all in application—holiday applies across them.

- Hardship proof: Keep records like bills or medical notes.

- Review regularly: Reassess at holiday end; consider rate changes via KS2.

For nannies or casual workers, holidays pair well with family discussions on pay impacts.

"A contribution holiday lets you temporarily stop making contributions for 3-12 months... apply with a valid reason, such as financial hardship."

Next Steps: Manage Your KiwiSaver Wisely

Ready to apply? Log into myIR today or call IRD on 0800 775 247. Compare providers via sorted.org.nz, and chat with a financial adviser—especially with 2026 changes looming. Remember, pausing contributions is a tool, not a full stop; balance it with voluntary saves for retirement security.

Disclaimer: This is general info, not personalised advice. Consult a licensed adviser or IRD for your situation. Rates current as of 2026.

Frequently Asked Questions

Sources & References

-

1

Subpart 4 - Contributions holidays - Tax Technical - Inland Revenue — www.taxtechnical.ird.govt.nz

-

2

KiwiSaver Contributions | AMP New Zealand — www.amp.co.nz

-

3

Changes to the KiwiSaver contribution rate - Inland Revenue — www.ird.govt.nz

-

4

What is the NZ KiwiSaver Employer Contribution? | LegalVision NZ — legalvision.co.nz

-

5

KiwiSaver - key features for employees and employers - SuperLife — www.superlife.co.nz

-

6

Changes to KiwiSaver - Teesdale Associates — teesdaleassociates.com

-

7

KiwiSaver changes - Inland Revenue — www.ird.govt.nz

-

8

KiwiSaver Contribution Rate Hits 4% in 2026 — What It Means for... — www.exclusivechauffeur.co.nz

-

9

KiwiSaver Changes Coming: What Nannies and Families Need to... — paythenanny.nz

-

10

KiwiSaver contributions holiday - MAS - Medical Assurance — www.mas.co.nz

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...