Unconditional Offers NZ: Risks of Going Unconditional

Imagine spotting your dream home in a heated Auckland market, heart racing as you craft an offer to outbid the competition. In a rush of excitement, you go unconditional, only to discover weeks later...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Imagine spotting your dream home in a heated Auckland market, heart racing as you craft an offer to outbid the competition. In a rush of excitement, you go unconditional, only to discover weeks later that the bank won't lend on it—or worse, hidden defects emerge that turn your dream into a nightmare. This scenario plays out too often for Kiwi buyers, costing tens of thousands in deposits and legal fees.

In New Zealand's competitive property landscape of 2026, unconditional offers are a double-edged sword. They're a powerful tool to secure a property at auction or against multiple bidders, but they come with steep risks of going unconditional. Without protective conditions, you're legally bound, potentially facing financial ruin if things go wrong. This guide breaks down the pitfalls, real-life examples, and practical steps to protect yourself when navigating Unconditional Offers NZ.

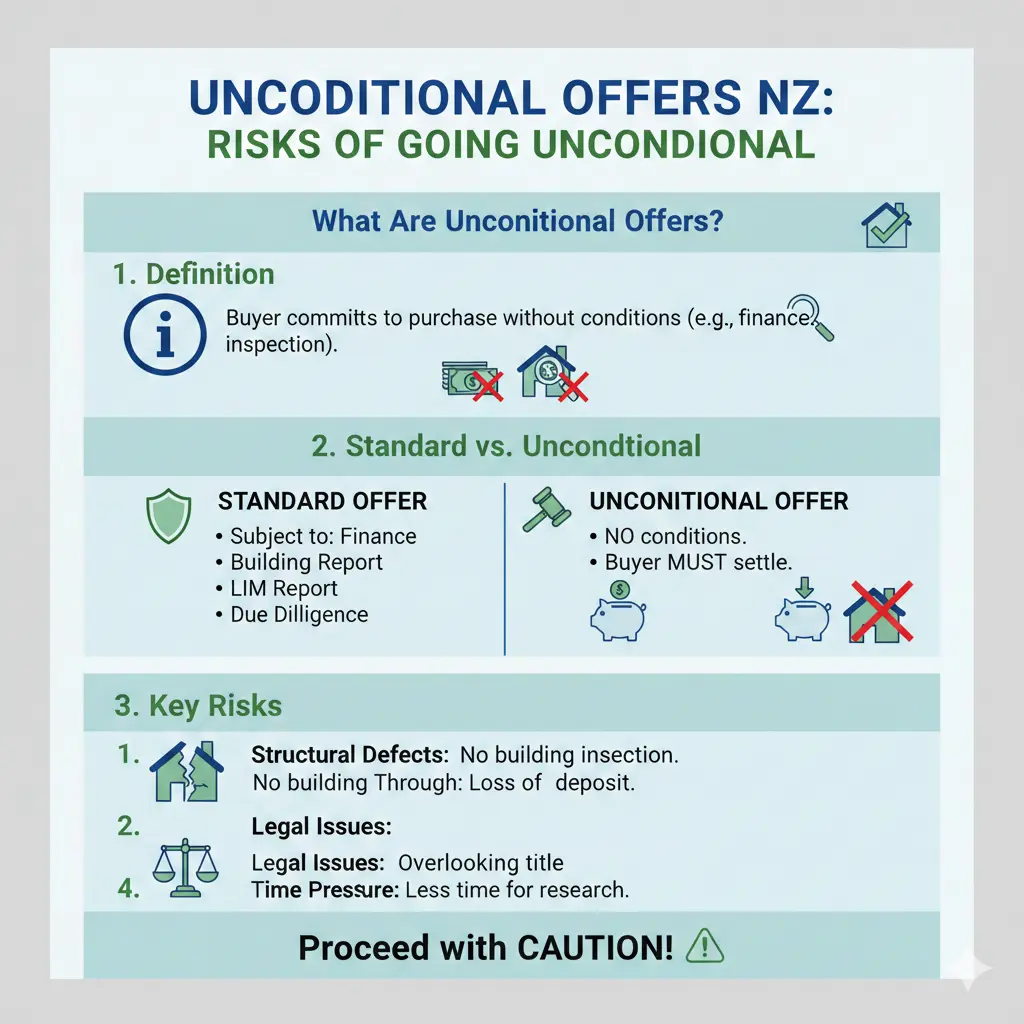

What Are Unconditional Offers in New Zealand?

Unconditional offers, also known as "clean" offers, contain no escape clauses or "subject to" conditions. Once the seller accepts, the Sale and Purchase Agreement (SPA) becomes binding, committing you to complete the purchase regardless of unforeseen issues.

In contrast, conditional offers include safeguards like finance approval, building inspections, or LIM reports, typically with 10-15 working days to satisfy them. If unmet, you can withdraw and reclaim your deposit—usually 10% of the purchase price.

Why Do Buyers Make Them?

- Auctions: Bidding at auction is always unconditional; the highest bid wins immediate commitment, with a 10% deposit due on the spot.

- Competitive markets: In hot spots like Wellington or Christchurch suburbs, sellers prioritise unconditional offers to avoid delays.

- Cash buyers or investors: Those with funds ready skip conditions for speed.

While tempting, rushing unconditional without preparation exposes you to severe risks, as we'll explore next.

The Major Risks of Going Unconditional

Skipping due diligence in an unconditional offer can lock you into a bad deal. Here's what Kiwis need to watch for in 2026's market.

1. Finance Falls Through

Many buyers mistake pre-approval for full approval. Pre-approvals are conditional on factors like the specific property's suitability as security. If the bank rejects the home—due to location, condition, or valuation—you're still obligated to settle or forfeit your deposit.

Real example: Client "Mr A" skipped pre-approval for an auction, bid high on his dream home, and went unconditional. When the bank wouldn't lend fully and he refused to settle, he lost his $200,000 deposit—a brutal lesson in haste.

In 2026, with interest rates hovering and lending criteria tightened by the Reserve Bank, banks scrutinise properties more than ever. Always get written confirmation that the exact property is acceptable security before going unconditional.

2. Undiscovered Property Defects

Without a builder's report, you might inherit leaky buildings, subsidence, or weathertightness issues common in older Kiwi homes. Unconditional means no backing out, even if repairs cost $100,000+.

LIM reports from councils reveal zoning, flooding risks, rates, and consents—but miss structural problems or meth contamination. At $200-$400 per LIM, it's cheap insurance, yet many skip it.

"The risk of going unconditional without doing this homework is significant—you could be locked into buying a property with hidden defects."

3. Low Bank Valuation

If the bank's valuation comes in below your offer, you'll need to cover the gap from your pocket. In a cooling 2026 market, overbidding at auction amplifies this risk.

4. Legal and Financial Penalties

Can't settle? Sellers can sue for "specific performance" (forcing the sale) or keep your deposit. Disputes head to the Disputes Tribunal or High Court, adding lawyer fees.

Deposits are held in trust by lawyers until settlement, but unconditional means no refunds without mutual agreement or court intervention—rarely buyer-friendly.

Real-Life Case Studies: Lessons from Kiwi Buyers

Stories from the front lines highlight the stakes.

Case Study 1: Mr A's $200,000 Nightmare

Too busy for pre-approval, Mr A found his ideal property and bid at auction the next day. Initial assessments flagged risks—like bank security rejection—but he proceeded unconditional. Post-acceptance, finance failed, and unwilling to settle, he forfeited $200,000. Key takeaway: Complete borrowing checks first.

Case Study 2: Hidden Defects in Wellington

A buyer in 2025 (similar to 2026 trends) went unconditional to win a tender, skipping the builder's report. Post-purchase, asbestos and foundation cracks surfaced, costing $150,000 in fixes. A conditional offer with a 10-day inspection clause would have saved them.

These aren't outliers. REINZ data shows rising disputes over unconditional failures amid 2026's steady but selective market.

How to Protect Yourself: Practical Steps Before Going Unconditional

Don't let FOMO cloud judgement. Follow these actionable tips tailored for New Zealand buyers.

Step 1: Secure True Finance Approval

- Get pre-approval, then confirm the specific property in writing with your lender.

- Share this with your lawyer before signing.

- Avoid relying on calculators—bank outcomes vary.

Step 2: Complete Due Diligence Upfront

- LIM Report: Order from your council (e.g., Auckland Council at aucklandcouncil.govt.nz). Check for hazards and consents.

- Builder's Report: Hire a licensed inspector (~$800-$1,200) for structural checks.

- Title Search: Via Land Information New Zealand (LINZ) for caveats or restrictions.

- Meth Test: Essential for pre-2000s homes (~$500).

Step 3: Use a Skilled Lawyer and Agent

Engage a property lawyer early. They review the SPA and advise on conditions. In auctions, brief them on your limits. Real estate agents must disclose known issues under the Real Estate Agents Act 2008.

Step 4: Consider Alternatives to Unconditional

In tenders, propose short conditions (5 days). For cash offers, verify funds liquidity. If competing, a strong conditional offer with quick deadlines can win.

Pro Tip: Budget 1-2% of purchase price for due diligence—far cheaper than a lost deposit.

Unconditional Offers in 2026: Market Context

With house prices stabilising post-2025 peaks, competition eases in some regions, reducing unconditional pressure. However, Auckland and Queenstown remain fierce. Reserve Bank lending rules (LVR restrictions) make finance trickier for investors.

Official advice from the Real Estate Authority (REA) urges due diligence always. Check rea.govt.nz for buyer guides.

Next Steps: Buy Smarter, Not Faster

Thrilled by a property? Pause. Prioritise pre-approval, LIM, and inspections before any unconditional move. Consult your lawyer, broker, and a trusted agent. In 2026's market, informed buyers win without the risks.

Disclaimer: This is general advice. Property purchases involve risks; seek professional financial and legal advice tailored to your situation from qualified experts like those registered with the REA or Financial Markets Authority.

Frequently Asked Questions

Sources & References

- 1

-

2

Making an Offer on a House NZ | Buyer Guide 2026 — haydenroulston.co.nz — www.haydenroulston.co.nz

-

3

The risks of unconditional agreements for a buyer of residential property — harknesshenry.co.nz — www.harknesshenry.co.nz

-

4

Buying property in New Zealand in 2026 — smartcurrencyexchange.com — www.smartcurrencyexchange.com

- 5

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...