Compound Interest: How It Can Make You Wealthy

Imagine turning a modest KiwiSaver contribution into a nest egg that funds your retirement dreams— that's the magic of compound interest. It's not just for the wealthy; it's a powerful tool available...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Imagine turning a modest KiwiSaver contribution into a nest egg that funds your retirement dreams— that's the magic of compound interest. It's not just for the wealthy; it's a powerful tool available to everyday Kiwis looking to build wealth over time.

Whether you're stashing cash in a term deposit, contributing to KiwiSaver, or investing in shares, compound interest works tirelessly in the background, earning you interest on your interest. In this guide, we'll break down how it operates, why it can make you wealthy, and practical steps tailored for New Zealanders in 2026.

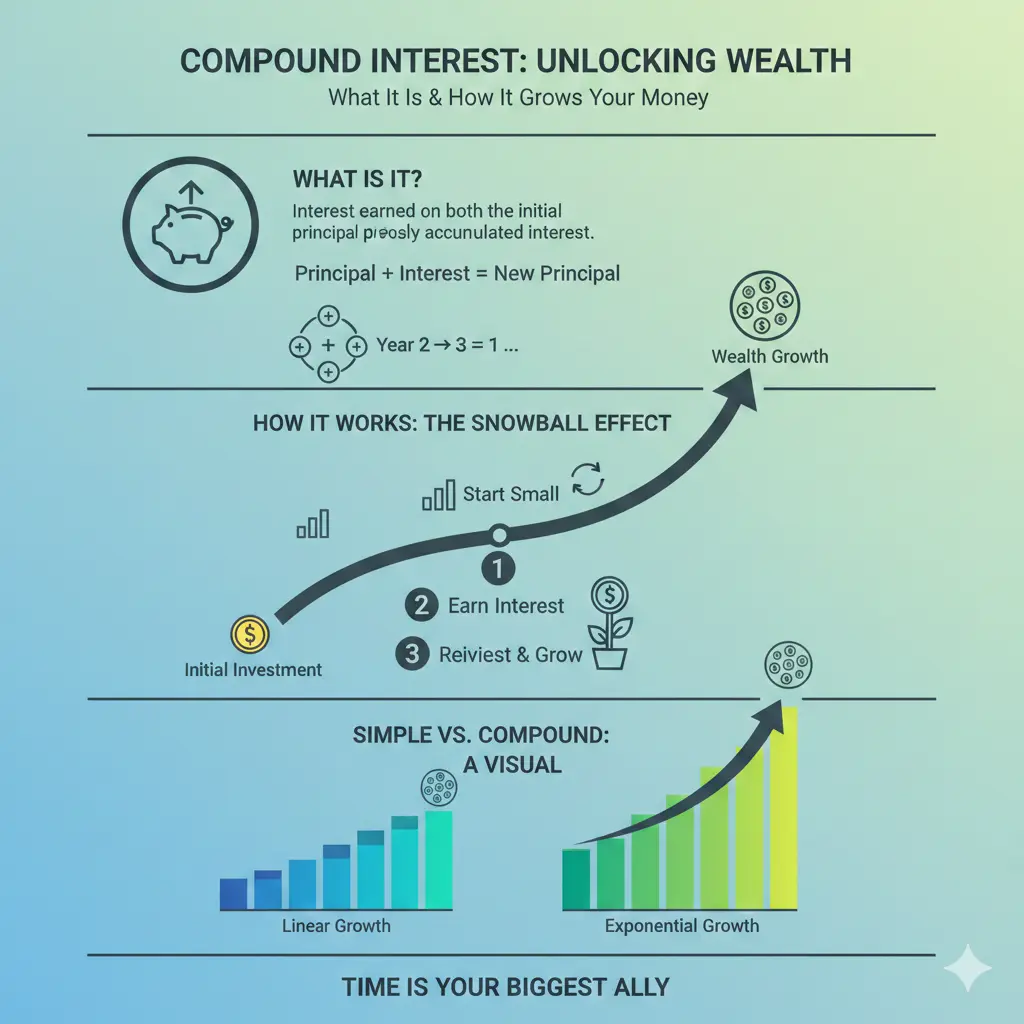

What is Compound Interest?

Compound interest is when interest is added to your principal amount, and then in the next period, you earn interest on that larger sum—including the previously earned interest. It's often called "interest on interest."

Unlike simple interest, which only applies to the original amount, compounding supercharges growth. For Kiwis, this is key in savings accounts, term deposits, and KiwiSaver funds where interest or returns compound frequently—monthly, quarterly, or annually.

Compound vs Simple Interest: A Quick Comparison

Picture investing $10,000 at 5% interest:

- Simple interest: Year 1: $500 (total $10,500). Year 2: another $500 (total $11,000).

- Compound interest (annual): Year 1: $500 (total $10,500). Year 2: $525 (total $11,025).

The difference grows exponentially over time. By year 3, compounding yields $551.25 in interest, pushing your total to $11,576.25.

How Compound Interest Works in Practice

The formula for compound interest is A = P(1 + r/n)^(nt), where:

- A = final amount

- P = principal (starting amount)

- r = annual interest rate (decimal)

- n = compounding frequency per year

- t = time in years

For New Zealanders, banks like ANZ and Westpac offer tools to model this. More frequent compounding (e.g., monthly) beats annual payouts.

Real Kiwi Example: $10,000 Term Deposit

Invest $10,000 in a 5-year term deposit at 5% p.a., compounded annually:

| Year | Opening Balance | Interest Earned | Closing Balance |

|---|---|---|---|

| 1 | $10,000 | $500 | $10,500 |

| 2 | $10,500 | $525 | $11,025 |

| 3 | $11,025 | $551.25 | $11,576.25 |

| 4 | $11,576.25 | $578.81 | $12,155.06 |

| 5 | $12,155.06 | $607.75 | $12,762.81 |

That's $2,762.81 total growth—$762.81 more than simple interest.

The Power of Time and Regular Contributions

Time is your greatest ally. The longer your money compounds, the more dramatic the results. Add regular contributions, and it's game-changing for Kiwis building wealth.

KiwiSaver: Your Compound Interest Superpower

In 2026, KiwiSaver balances grow through employer and government contributions plus investment returns that compound. Start with $1,000 monthly at 5% compounded annually: reach $100,000 in about 8 years 10 months. Simple interest? Over 10 years.

Historical data shows diversified funds averaging 5-7% after fees, far outpacing bank rates of 2-4%. Use Sorted's savings calculator to project your KiwiSaver growth.

Long-Term Projection: $400 Monthly at 10%

Invest $1,000 initially, add $400/month at 10% (S&P 500 average): After 40 years, $2.58 million. Stretch to 50 years? $7.08 million. This highlights why starting young matters for Kiwis.

New Zealand-Specific Opportunities in 2026

With OCR at projected lows and term deposit rates around 4-5%, compound interest shines in KiwiSaver and managed funds. PIE funds (Portfolio Investment Entities) offer tax efficiency—returns taxed at your PIR (10.5%-39%), often lower than personal rates.

Top Kiwi Tools for 2026

- MoneyHub Calculator: Models savings/debt with NZ frequencies.

- Sorted Savings Calculator: Free govt-backed tool for compound projections.

- ANZ Long-Term Savings: Includes interest growth forecasts.

- Interest.co.nz Calculators: Compound gain and DTI tools.

Property? Opes Partners' capital growth calculator shows compounding appreciation. Milford notes compounding boosts returns exponentially.

The Flip Side: Compound Interest on Debt

It's a double-edged sword. Credit cards compound daily at 20%+—a $1,000 unpaid balance balloons fast as interest accrues on interest. Pay minimums? Debt spirals. Prioritise high-interest debt before investing.

Actionable Tip for Kiwis

Use WINZ debt calculators or MoneyHub to model payoffs. Aim for 0% balance transfers or low-rate personal loans from banks like ASB.

Practical Tips to Maximise Compound Interest

- Start Early: A 25-year-old investing $200/month at 7% hits $500,000 by 65. Wait 10 years? Half that.

- Increase Contributions: Bump KiwiSaver via payroll—get employer match up to 3%.[sorted.org.nz]

- Choose High-Compound Options: KiwiSaver growth funds (7-10% historical) over cash (2-4%).

- Reinvest Dividends: In shares/ETFs, let returns compound.

- Review Annually: Adjust PIR with IRD; switch providers if fees drag returns.

- Avoid Withdrawals: First home or hardship aside, let it compound untouched.

Common Myths About Compound Interest

- Myth: You need big money to start. Truth: $50/month compounds mightily over decades.

- Myth: It's guaranteed. Truth: Investments carry risk; past returns (e.g., 10% S&P) aren't future-proof.

- Myth: Too complex for beginners. Truth: Free calculators make it simple.

Start Building Wealth Today

Compound interest isn't a get-rich-quick scheme—it's a wealth-building marathon. As a Kiwi, leverage KiwiSaver, free calculators, and disciplined saving to harness its power. Plug your numbers into a tool like Sorted's calculator, set up auto-contributions, and watch your future grow. Your first step? Open or review your KiwiSaver today—wealth awaits.

Frequently Asked Questions

Sources & References

-

1

Compound Interest Calculator - MoneyHub NZ — www.moneyhub.co.nz

-

2

Interest Rate Calculator | Bizzloans New Zealand — www.bizzloans.co.nz

-

3

Compound Interest Calculator — calculate.co.nz — www.calculate.co.nz

-

4

Compound Interest Calc - App Store — apps.apple.com

-

5

Basics of Compound Interest — westpacnzstaffsuper.co.nz — www.westpacnzstaffsuper.co.nz

-

6

Savings calculator - Sorted — sorted.org.nz

-

7

Calculators - Interest.co.nz — www.interest.co.nz

-

8

Long term savings calculator - ANZ — tools.anz.co.nz

-

9

Capital Growth Calculator [2026] | Opes Partners — www.opespartners.co.nz

-

10

Compounding Returns - Milford Asset Management — milfordasset.com

Useful Tools

Related Articles

Ethical Investing in NZ: Top 5 Sustainable Funds for Kiwis

Ever wondered if you can grow your KiwiSaver or investments while doing good for the planet and people? Ethical investing in New Zealand is booming, with Kiwis pouring billions into funds that priorit...

Beginner's Guide to Investing in New Zealand

Getting started with investing in New Zealand doesn't have to be complicated. Whether you're looking to grow your wealth, save for retirement, or build financial security, there are plenty of accessib...

How to Buy Shares in New Zealand: Step-by-Step Guide

Ever wondered how to dip your toes into share investing without getting overwhelmed? Whether you're saving for a house deposit, retirement, or just want to grow your hard-earned cash, buying shares in...

ETFs vs Managed Funds: Which is Better for Kiwi Investors?

When you're ready to invest your money, you'll likely come across two main options: exchange-traded funds (ETFs) and managed funds. Both offer diversification and professional management, but they wor...