Contents Insurance for Students: Protecting Your Stuff at Uni

Moving into your first flat or uni hall feels like freedom—until something goes wrong. A flatmate spills red wine on your laptop during a late-night study session, or your phone vanishes from the laun...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Moving into your first flat or uni hall feels like freedom—until something goes wrong. A flatmate spills red wine on your laptop during a late-night study session, or your phone vanishes from the laundry in a shared house. For Kiwi students, these mishaps are all too common, and replacing essentials like tech gear or textbooks can wipe out your part-time job earnings in a flash. That's where contents insurance for students steps in, offering peace of mind without breaking the bank.

In New Zealand's rental-heavy student scene, protecting your stuff isn't a luxury—it's a smart financial move. With average premiums for 18-24-year-olds hitting around $901 annually as of late 2024, and costs varying widely from $644 to $1312 depending on the provider, there's affordable cover out there if you know where to look. This guide breaks down everything you need to know about contents insurance for students: protecting your stuff at uni, from costs and coverage to tips for getting the best deal in 2026.

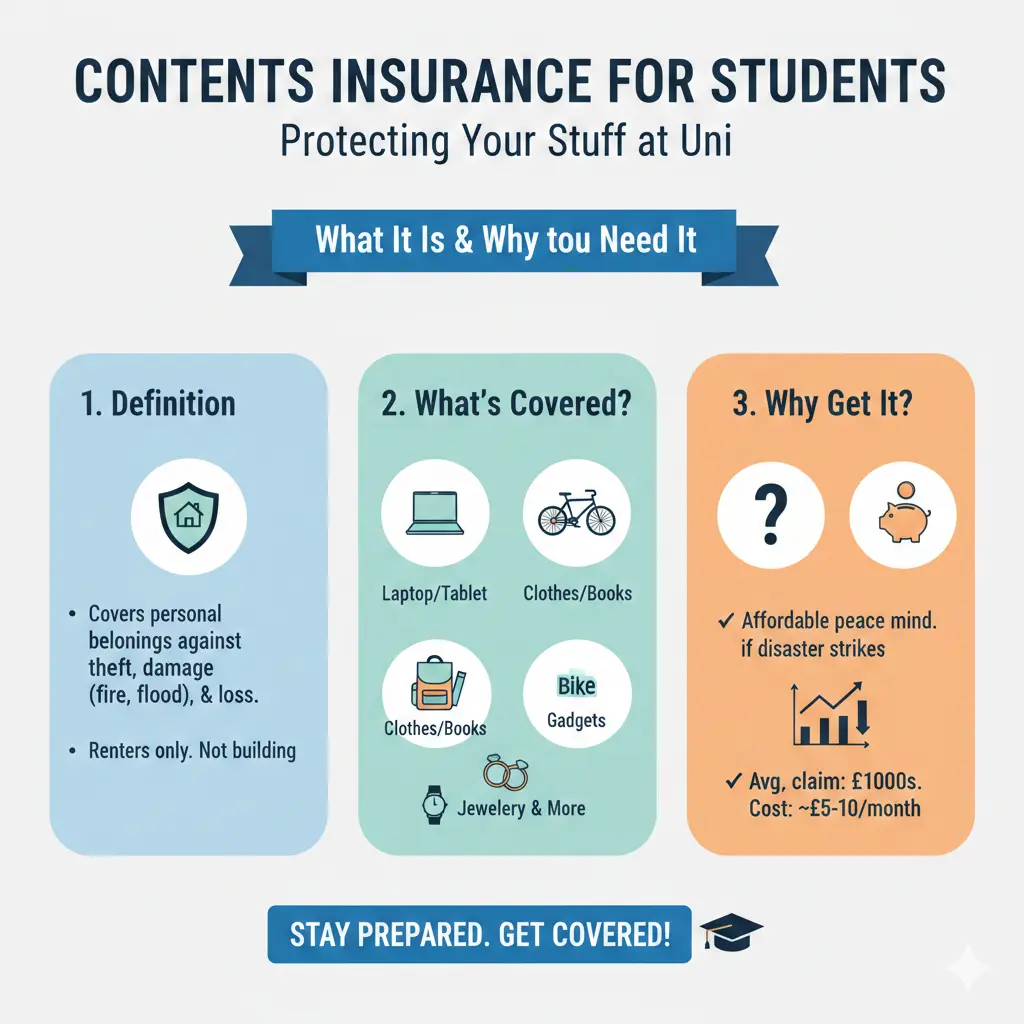

What is Contents Insurance for Students?

Contents insurance for students—often just called student insurance—is a policy that covers your personal belongings against theft, damage, fire, or loss while you're living away from home. It's not the same as your landlord's insurance, which typically only protects their fixtures like beds or whiteware in furnished rentals.

Whether you're in a noisy hall of residence at the University of Auckland, flatting in Dunedin, or renting near Victoria Uni in Wellington, this cover safeguards what you own: laptops for assignments, phones for staying connected, bikes for getting around campus, and even textbooks that cost a fortune.

Why Students Need It More Than You Think

Shared living amps up the risks. Flatmates might "borrow" without asking, parties lead to accidents, and unsecured bikes get nicked outside the library. Insurers like MAS report phones as the top claim item for students, followed by laptops and bikes—items that are pricey to replace on a student budget.

- Theft from unlocked flats or drying rooms.

- Accidental damage, like dropping your tablet or a spill on your gaming console.

- Fire or water damage in communal kitchens.

- Loss during travel between home and uni.

Without cover, you're out of pocket. A new laptop could set you back $1,500+, draining your KiwiSaver or WINZ student allowance.

Does Your Parents' Policy Cover You at Uni?

Before buying standalone cover, check if you're already protected under your parents' or guardians' home contents insurance. Many policies extend coverage for students living away, as long as you're studying full-time and not working full-time.

Key conditions to verify:

- Are you defined as a "student" under 25 living away for education?

- Does it include portable cover for items taken to uni across New Zealand?

- Is the sum insured high enough for your gear?

If it works, this can be cheaper. But limitations apply—some policies cap portable items or exclude shared housing risks. Always get written confirmation from the insurer, and list high-value items like your MacBook separately.

When to Get Your Own Policy

Opt for standalone contents insurance for students if:

- Your parents' policy doesn't cover flats or has low limits.

- You're an international student (note: medical/travel insurance is separate and often mandatory).

- You want specified cover for expensive items like musical instruments or sports gear over standard limits (e.g., $5,000 per electronic item).

What Does Student Contents Insurance Typically Cover?

A good policy protects the essentials of student life. Standard cover includes up to $10,000-$20,000 total, with sub-limits for specifics. Here's what to expect:

| Item/Category | Typical Coverage | Examples |

|---|---|---|

| Electronics | $1,000-$5,000 per item | Laptops, phones, tablets, gaming consoles |

| Study Materials | Up to policy limit | Textbooks, notes, desk |

| Clothing & Personal Items | Up to 20% of sum insured | Clothes, jewellery, bike |

| Sports/Instruments | $8,000 for bikes; specify extras | Guitar, javelin, stethoscope |

Look for policies covering accidental damage (e.g., cracked phone screens), theft (even from unlocked cars in some cases), and portable benefits anywhere in NZ. Providers like AMP's Everyday Contents Insurance target students with tech-focused protection.

"We've paid claims for snapped javelins, lost stethoscopes, and even a stolen spa pool from a flat."

Tenant's liability (often $20,000+) is a bonus, covering accidental damage to the landlord's property—like flooding the kitchen.

How Much Does Contents Insurance Cost for Students in 2026?

Costs have risen, but bargains exist. For Kiwis aged 18-24, the average annual premium was $901 in Q4 2024, up 38% from $651 in 2022. Recent quotes from MoneyHub peg student policies at $400-$600 per year, depending on location and cover level.

Factors influencing your premium:

- Location: Higher in cities like Auckland due to theft rates.

- Sum Insured: $15,000 cover costs more than $10,000.

- Excess: Higher excess (e.g., $500) lowers premiums.

- Discounts: Student deals, no-claims history, or bundling with other policies.

In 2026, expect slight increases due to inflation and claims trends, but shopping around reveals gaps of $668 between cheapest and priciest options. Use comparison sites like Quashed for real-time quotes.

Real Costs Breakdown (2024-2026 Estimates)

- Basic policy ($10k cover): $400-$644

- Mid-range ($20k + portable): $700-$900

- Premium (high limits): $1,000-$1,312

Pro tip: Download a contents calculator spreadsheet to value your stuff accurately—avoid underinsuring.

How to Choose the Best Contents Insurance for Students

Don't just pick the cheapest. Prioritise these features for uni life:

Key Features to Look For

- Portable Cover: Protects gear anywhere in NZ—vital for library trips or holidays home.

- Accidental Damage: Covers spills, drops—not all policies include this.

- Specified Items: List valuables exceeding limits (e.g., drone or e-bike).

- Excess Options: Choose $200-$500 to fit claims to your budget.

- Claims Process: Easy online apps, 24/7 support.

Top Tips for Saving Money

- Compare at least 3-5 quotes via sites like Quashed.

- Increase excess to drop premiums by 20-30%.

- Bundled student deals from AMP or MAS.

- Pay annually for discounts.

- Build no-claims bonus over time.

For international students, add Studentsafe for medical/travel (e.g., $899/year for full academic cover), but it's separate from contents.

Common Mistakes to Avoid with Student Contents Insurance

Students often undervalue contents or skip reading the fine print. Here's how to dodge pitfalls:

- Underinsuring: List everything—use Suncorp's calculator.

- Ignoring Exclusions: Floods, wear-and-tear, or unlocked theft might not be covered.

- Not Declaring High-Value Items: Bikes over $8k need specifying.

- Forgetting Tenant Liability: Essential for rentals under the Residential Tenancies Act.

Next Steps: Get Protected Today

Don't wait for disaster—value your gear, check parents' cover, and compare quotes now. Tools like Quashed make it quick, potentially saving hundreds. Remember, this isn't financial advice; consult a licensed adviser or insurer for your situation. With the right contents insurance for students, you can focus on acing exams, not stressing over spills.

Grab a spreadsheet, list your valuables, and shop smart. Your future self (and wallet) will thank you.

Frequently Asked Questions

Sources & References

-

1

Protect Your Stuff: Contents Insurance for Students - Quashed — quashed.co.nz

-

2

Contents Insurance for Students | AMP New Zealand — www.amp.co.nz

-

3

Insurance for Students - Cover and Policy Costs - MoneyHub NZ — www.moneyhub.co.nz

- 4

-

5

Insurance for international students - Massey University — www.massey.ac.nz

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...