KiwiSaver Fees Explained: How Much Are You Really Paying?

Ever wondered where your hard-earned KiwiSaver contributions are really going? With fees quietly nibbling at your retirement nest egg, understanding them is crucial—especially as contribution rates ri...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Ever wondered where your hard-earned KiwiSaver contributions are really going? With fees quietly nibbling at your retirement nest egg, understanding them is crucial—especially as contribution rates rise to 3.5% from 1 April 2026.KiwiSaver fees explained reveals the hidden costs, from management charges to membership fees, helping you spot low-fee providers and maximise your savings.

In New Zealand, KiwiSaver is our ticket to a secure retirement, but fees can eat into returns over decades. As of 2026, with minimum employee and employer contributions jumping to 3.5% of gross pay, every dollar counts. This guide breaks down the types of fees, real-world examples from providers like Westpac, Simplicity, and Fisher Funds, and actionable steps to keep more money in your pocket. Whether you're a first-time saver or reviewing your fund, you'll learn how much you're really paying and what to do about it.

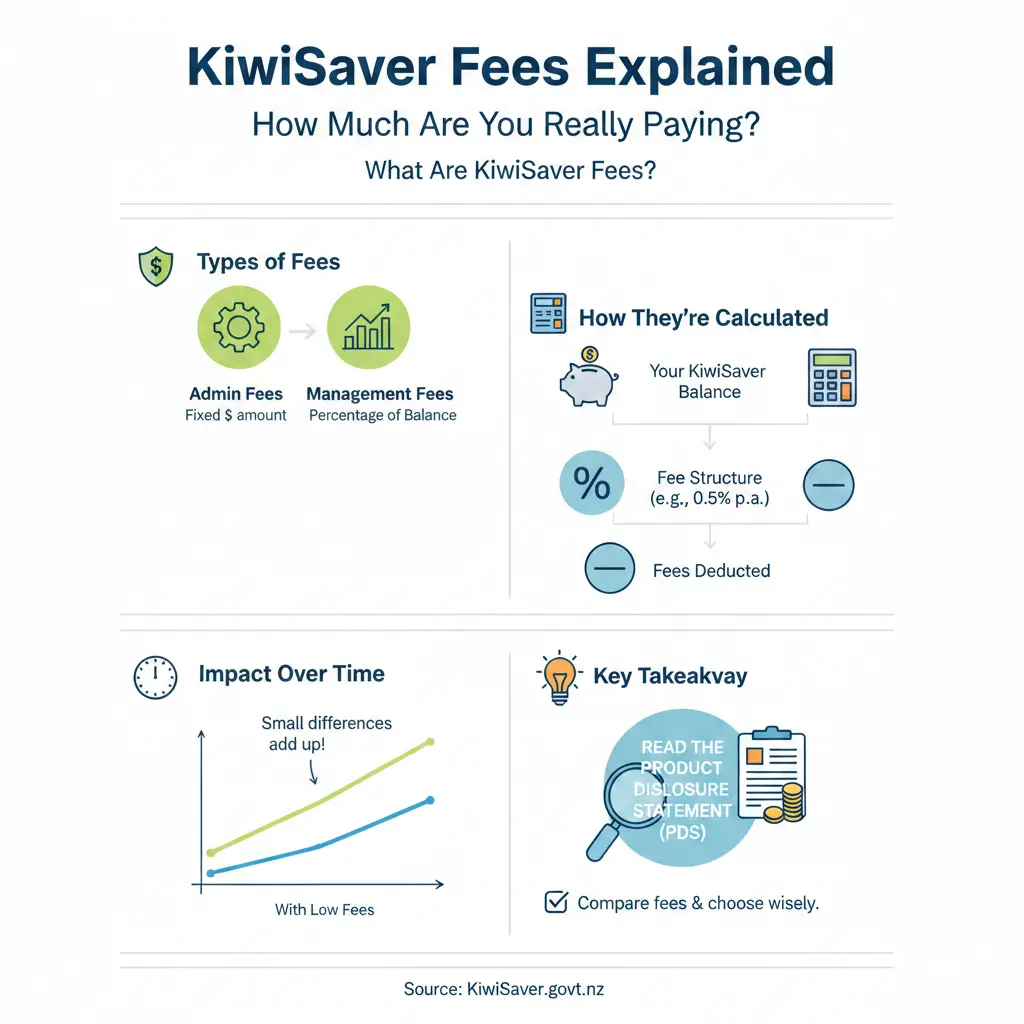

What Are KiwiSaver Fees?

KiwiSaver fees are charges deducted from your account to cover administration, investment management, and other costs. They're not a flat rate—most are a percentage of your balance, so they grow as your savings do. Providers must disclose fees in Product Disclosure Statements (PDS), but comparing them isn't always straightforward.

Regulated by the Financial Markets Authority (FMA), fees impact your long-term growth. For instance, a 1% fee difference on a $100,000 balance costs $1,000 yearly—and compounds massively over 30 years. Key point: lower fees don't always mean better returns, but they're vital for cost-conscious Kiwis.

Main Types of KiwiSaver Fees

- Management or Administration Fees: Cover fund management and daily operations. Typically 0.3%-1.5% p.a., deducted automatically from your balance.

- Membership or Account Fees: Flat fees, often $20-$60/year, sometimes waived for larger balances.

- Performance Fees: Rare in KiwiSaver; a cut of profits above a benchmark (check your PDS).

- Other Expenses: Transaction costs, custody fees, or buy/sell spreads—often bundled into the total fund charge.

- Withdrawal or Transfer Fees: Applied when leaving a fund or accessing savings early (e.g., first home or hardship).

The total annual fund charge combines these, shown in your annual statement. Tools like Sorted.org's Smart Investor compare them apples-to-apples.

How KiwiSaver Fees Are Calculated and Charged

Fees are mostly percentage-based, calculated daily or monthly on your balance, then deducted automatically—no separate transactions appear. For a $10,000 High Growth fund balance at 0.70%, you'd pay about $70/year.

Fee Structures by Provider

Different providers shine in different areas. Here's a snapshot of 2026 fees:

| Provider/Fund | Annual Fund Charge | Membership Fee |

|---|---|---|

| Westpac High Growth | 0.70% | None (one fee covers all) |

| Westpac Cash | 0.25% | None |

| Simplicity Growth/High Growth | 0.29% | None |

| Fisher Funds Cash | 0.45% (0.36% fixed + 0.09% estimated) | Varies |

| ANZ (simple structure) | Up to fund max (e.g., 0.5%-1.0% typical) | One fee covers all |

Average fees per Sorted.org: Growth funds 1.23%, Balanced 1.01%, Conservative 0.90%. Low-fee leaders like Simplicity keep it under 0.30%, passing 15% to charity.

Impact of 2026 KiwiSaver Changes on Fees

While fees themselves aren't changing, higher contributions mean bigger balances—and higher absolute fees. From 1 April 2026, default rates rise to 3.5% (you and employer), then 4% in 2028. You can apply for a temporary 3% reduction from 1 February 2026 via IRD—no hardship proof needed, up to 12 months.

Government contributions halved to 25c/dollar (max $260.72) from 1 July 2025, excluded for $180k+ earners, but now for 16-17-year-olds. More contributions amplify fee drag, so review now.

Real Kiwi Examples: How Much Are You Really Paying?

Let's crunch numbers for typical Kiwis.

Example 1: Sarah, 35, $80k Salary, High Growth Fund

Sarah contributes 3.5% ($233/month pre-tax), employer matches. Balance: $50,000 in Westpac High Growth (0.70%).

- Annual fee: $350 (0.70% of $50k).

- After 10 years (assuming 6% net return): Balance ~$110k, fees ~$770/year.

- Switch to Simplicity (0.29%): Saves $205/year initially.

Example 2: Mike, 50, $120k Salary, Balanced Fund

$350/month each from Mike/employer at 3.5%. $200k balance in average Balanced fund (1.01%).

- Fees: $2,020/year.

- Low-fee option (0.40%): $800/year—saves $1,220 annually.

Over 20 years, that 0.61% difference could cost Mike $50,000+ in fees. Use Sorted's tool for your scenario.

How to Compare KiwiSaver Funds and Minimise Fees

Don't just chase returns—factor fees. Here's your toolkit:

- Check Sorted.org Smart Investor: Compares total fees for $10k investment.

- Review PDS: Look for total annual fund charge, not just headline fees.

- Calculate True Cost: (Management + Membership/Balance) x Balance.

- Switch Providers: Free once every 12 months via your provider or IRD.

- Aim Low: Under 0.50% for growth funds is excellent.

Practical tip: Log into myKIWISaver (ird.govt.nz) for your balance and fees. Compare via FMA register.

Common Myths About KiwiSaver Fees

- Myth: All providers charge the same. Reality: Ranges from 0.20%-3%.

- Myth: Fees are tax-deductible. No—KiwiSaver is pre-tax, but fees reduce taxable income indirectly.

- Myth: Higher fees mean better performance. Data shows low-fee passives often outperform.

"Our fees are among the lowest in the market." — Simplicity KiwiSaver.

Next Steps to Cut Your KiwiSaver Fees

1. Grab your latest statement—spot your total fund charge.

2. Use Sorted.org to benchmark.

3. If over 0.50%, research low-fee options like Simplicity.

4. Adjust contributions pre-1 April 2026 if needed via IRD.

5. Consult a financial adviser (fee-based, not commission) or use free Sorted tools.

Disclaimer: This is general info, not advice. Seek professional financial advice for your situation. KiwiSaver rules per IRD/FMA.

By understanding KiwiSaver fees explained: how much are you really paying?, you'll safeguard your retirement. Start comparing today—your future self will thank you.

Frequently Asked Questions

Sources & References

-

1

KiwiSaver changes - Inland Revenue — www.ird.govt.nz

-

2

Fees | Westpac NZ — www.westpac.co.nz

-

3

Key KiwiSaver changes you need to know for 2026 — www.generatewealth.co.nz

-

4

Understanding KiwiSaver fees - Simplicity — simplicity.kiwi

-

5

New Zealand increases employer and employee contribution rates — Lockton — global.lockton.com

-

6

ANZ-managed KiwiSaver scheme fund performance and fees — www.anz.co.nz

-

7

Kiwisaver - Budget 2025 — www.budget.govt.nz

-

8

Fees and expenses - Fisher Funds — fisherfunds.co.nz

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...