Online-Only Banks NZ: Are They Safe and Worth It?

Imagine ditching the queues at your local branch, managing your money from your phone anywhere in New Zealand, and potentially earning higher interest without the hefty fees. That's the promise of onl...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Imagine ditching the queues at your local branch, managing your money from your phone anywhere in New Zealand, and potentially earning higher interest without the hefty fees. That's the promise of online-only banks—or neobanks as they're often called. But are they truly safe for Kiwis, and do they deliver real value in 2026? Let's dive into the facts, compare them to traditional banks like ANZ, ASB, and Kiwibank, and help you decide if switching makes sense for your finances.

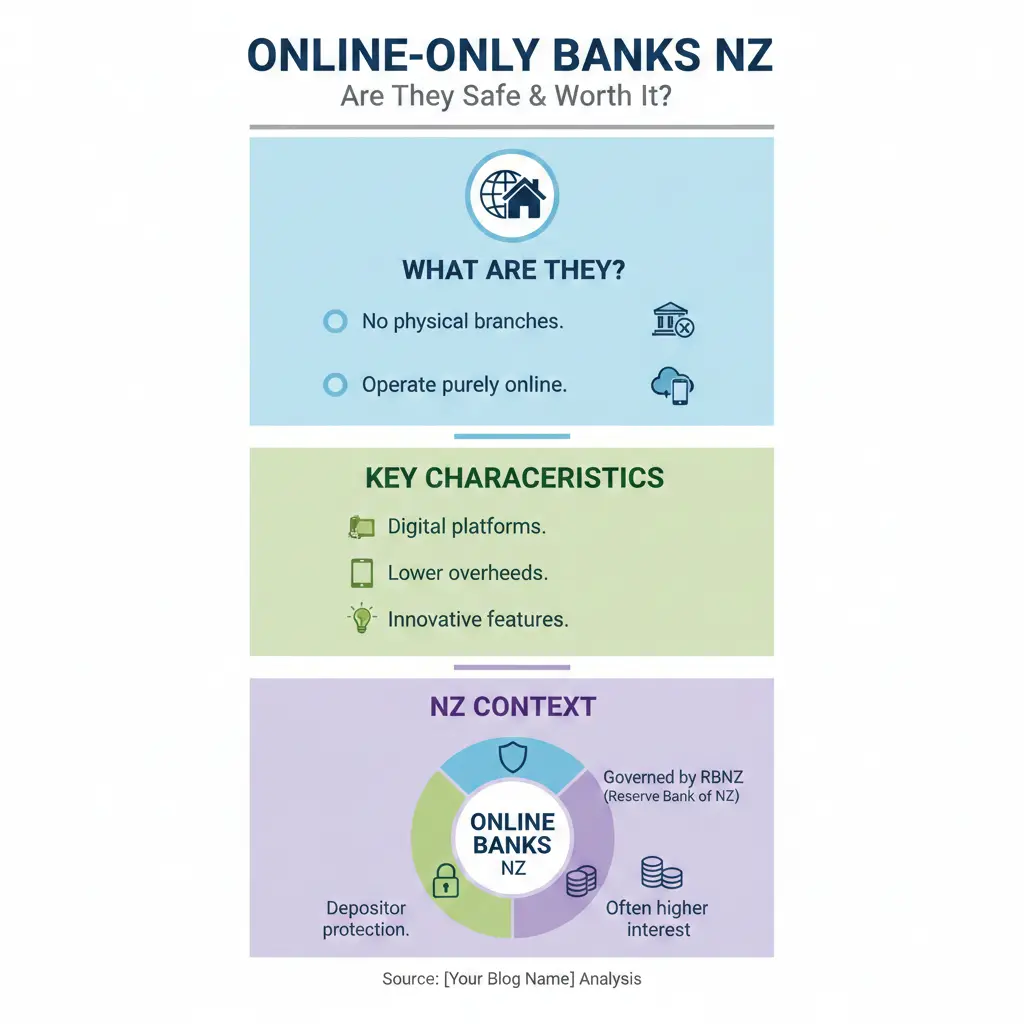

What Are Online-Only Banks in New Zealand?

Online-only banks, also known as neobanks or digital banks, operate entirely through apps and websites without physical branches. In New Zealand, they're gaining traction among tech-savvy Kiwis who value convenience, low fees, and competitive rates. As of February 2026, there are around 8 neobanks operating here, focusing on personal and business accounts, international transfers, and high-interest savings.

Unlike the big four—ANZ, ASB, BNZ, and Westpac—these providers like Wise, Heartland Direct, and emerging fintechs such as Wedge and Sharesies Save don't have widespread branches. Instead, they leverage modern platforms like Mambu or Backbase for seamless digital experiences. This model cuts overheads, often passing savings to customers through fee-free accounts and better interest.

Key Players in the NZ Market

- Wise (formerly TransferWise): Tops the list for international transactions with multi-currency accounts and low exchange rates. Trustpilot score: 4.14 from over 227,000 reviews.

- Heartland Bank YouChoose: Not fully branchless but offers a strong digital-first account with interest on balances and overdrafts at 10% p.a. App rated 4.2/5 on Android.

- Sharesies Save and Wedge Savings Fund: Fintech alternatives providing high-interest on-call savings without being full registered banks.

- Others like Airwallex and Remitly: Great for businesses and remittances, with high Trustpilot ratings up to 4.99.

These aren't always "pure" neobanks—some partner with licensed entities—but they prioritise digital access over bricks-and-mortar presence.

Are Online-Only Banks Safe in New Zealand?

Safety is paramount when trusting a provider with your hard-earned cash. The good news? New Zealand's regulatory framework offers strong protections, but not all digital providers are equal.

The Crown Jewel: Financial Markets Authority (FMA) and Reserve Bank Oversight

Registered banks in New Zealand are supervised by the Reserve Bank of New Zealand (RBNZ) and must hold a banking licence. They fall under the Depositors Compensation Scheme (DCS), guaranteeing up to $100,000 per depositor if the bank fails—covering 92% of retail deposits as of 2026.[RBNZ data, inferred from standard protections]. Traditional banks like Kiwibank and BNZ qualify fully.

Many online-only options, like Heartland Bank, are registered and DCS-protected. However, pure fintechs such as Wedge Savings Fund explicitly state: "Funds held in the Wedge Savings Fund are not protected by the Depositor Compensation Scheme." Always check the provider's status on the RBNZ register.

Cybersecurity and Fraud Protection

Neobanks invest heavily in tech security. Apps from providers like Wise use two-factor authentication, real-time fraud detection, and biometric logins. Kiwibank's app, for comparison, scores 4.3/5 on Android, but smaller players like SBS lag at 2.2/5. In 2026, RBNZ mandates open banking standards to enhance data security across all providers.

Practical tip: Enable app notifications, use strong passcodes, and monitor transactions daily. If fraud occurs, the Banking Ombudsman Scheme offers free dispute resolution for all account holders.

Real Risks and How to Mitigate Them

- Licensing Gaps: Non-bank fintechs (e.g., Debut, Dosh) aren't registered banks, so no DCS. Funds may be held in trust with partner banks—verify this.

- App Downtime: Rare, but outages happen. Have a backup traditional account.

- International Providers: Wise (UK-based) complies with NZ laws but check cross-border protections.

Overall, registered online banks are as safe as the big players, backed by RBNZ capital requirements. Fintechs carry slightly higher risk but offer innovation worth considering for low-balance users.

Pros and Cons: Online-Only vs Traditional Banks

To see if they're worth it, let's compare using a table of key features based on 2026 data.

| Feature | Online-Only/Neobanks (e.g., Wise, Heartland) | Traditional (e.g., ANZ, ASB, BNZ) |

|---|---|---|

| Fees | Fee-free everyday accounts | Often $0 but add-ons apply |

| Interest on Balances | Up to 4-5% on savings (e.g., Sharesies Save) | Lower, often 0% on transaction accounts |

| App Ratings (Android) | 4.0-4.8/5 (Wise 4.14 Trustpilot) | 4.3-4.8/5 (BNZ top) |

| Branches | None or limited | 100+ nationwide |

| Overdraft | Available, e.g., Heartland 10% p.a. | Yes, variable rates |

| DCS Protection | Yes for registered; no for some fintechs | Yes, up to $100,000 |

Top Pros for Kiwis

- Cost Savings: No monthly fees, unlimited EFTPOS—perfect for budgeting alongside KiwiSaver contributions.

- Higher Returns: Fintechs like Wedge and Dosh offer superior savings rates, beating traditional bank on-call accounts as of February 2026.

- Convenience: Instant transfers, budgeting tools, and international features for expat Kiwis or travellers.

- Innovation: Rewards like Dosh's 1% phone dollars with One NZ.

Potential Drawbacks

- No Cash Deposits: 90% of branch visits are for deposits—withdrawals; neobanks push digital alternatives like ATMs via partners.

- Limited Services: No in-person advice; less ideal for complex needs like home loans (though integrating with IRD for tax is seamless).

- Customer Support: App-based chat vs phone/branch—fine for most, frustrating during issues.

Best Online-Only Bank Accounts for Kiwis in 2026

Here's our curated picks tailored to common needs, updated February 2026.

Best Fee-Free Everyday Account: Heartland YouChoose

Pays interest on balances, overdraft option, solid app. Limited branches but nationwide ATMs.

Best for International: Wise

Multi-currency, low FX fees—ideal for overseas KiwiSaver top-ups or family remittances.

Best Savings Alternative: Sharesies Save or Wedge

High on-call rates without minimums; integrate with investments. Note: Not DCS-protected.

Compare rates regularly via MoneyHub, as they shift with OCR changes.

Practical Tips for Switching to an Online-Only Bank

- Check DCS Status: Use RBNZ's register (rbnz.govt.nz).

- Transfer Funds Safely: Set up direct debits last to avoid gaps.

- Link to KiwiSaver/IRD: Most integrate for auto-payments.

- Test the App: Download and trial features before full switch.

- Diversify: Keep a traditional account for cash needs.

Actionable: Start with Heartland or Wise for low-risk entry—sign up takes minutes.

Next Steps: Make the Switch Wisely

Online-only banks are safe for most Kiwis when choosing registered providers, offering real savings and convenience worth the digital leap. Start by comparing your needs—international? Go Wise. Everyday fees? Heartland. Always diversify and verify protections.

Disclaimer: This is general info, not personalised advice. Consult a financial adviser or visit ird.govt.nz for tax implications. Rates change—check providers directly.

Frequently Asked Questions

Sources & References

- 1

-

2

Best Bank Accounts - February 2026 - MoneyHub NZ — moneyhub.co.nz — www.moneyhub.co.nz

-

3

Neobanks in New Zealand in November 2025 — neobanks.app — neobanks.app

-

4

The 7 fintechs offering NZ's best savings account alternatives — squirrel.co.nz — www.squirrel.co.nz

- 5

Useful Tools

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...