Property Syndication NZ: Pooled Property Investment Explained

Ever dreamed of owning a slice of prime commercial real estate in Auckland or Christchurch, but baulked at the multi-million-dollar price tag? Property syndication in New Zealand makes it possible for...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Ever dreamed of owning a slice of prime commercial real estate in Auckland or Christchurch, but baulked at the multi-million-dollar price tag? Property syndication in New Zealand makes it possible for everyday Kiwis to pool resources and invest in high-value properties that would otherwise be out of reach. This pooled property investment approach offers steady income streams and potential capital growth, all while spreading risk across multiple investors.

In 2026, with the property market stabilising after years of flux, syndicates are gaining traction as a smart alternative to solo buying or shares.Property Syndication NZ lets you dive into commercial, industrial, or even residential assets with investments starting around $25,000 to $50,000. But like any investment, it's not without risks—think illiquidity and extra calls for cash. We'll break it down step by step, with practical tips tailored for Kiwi investors.

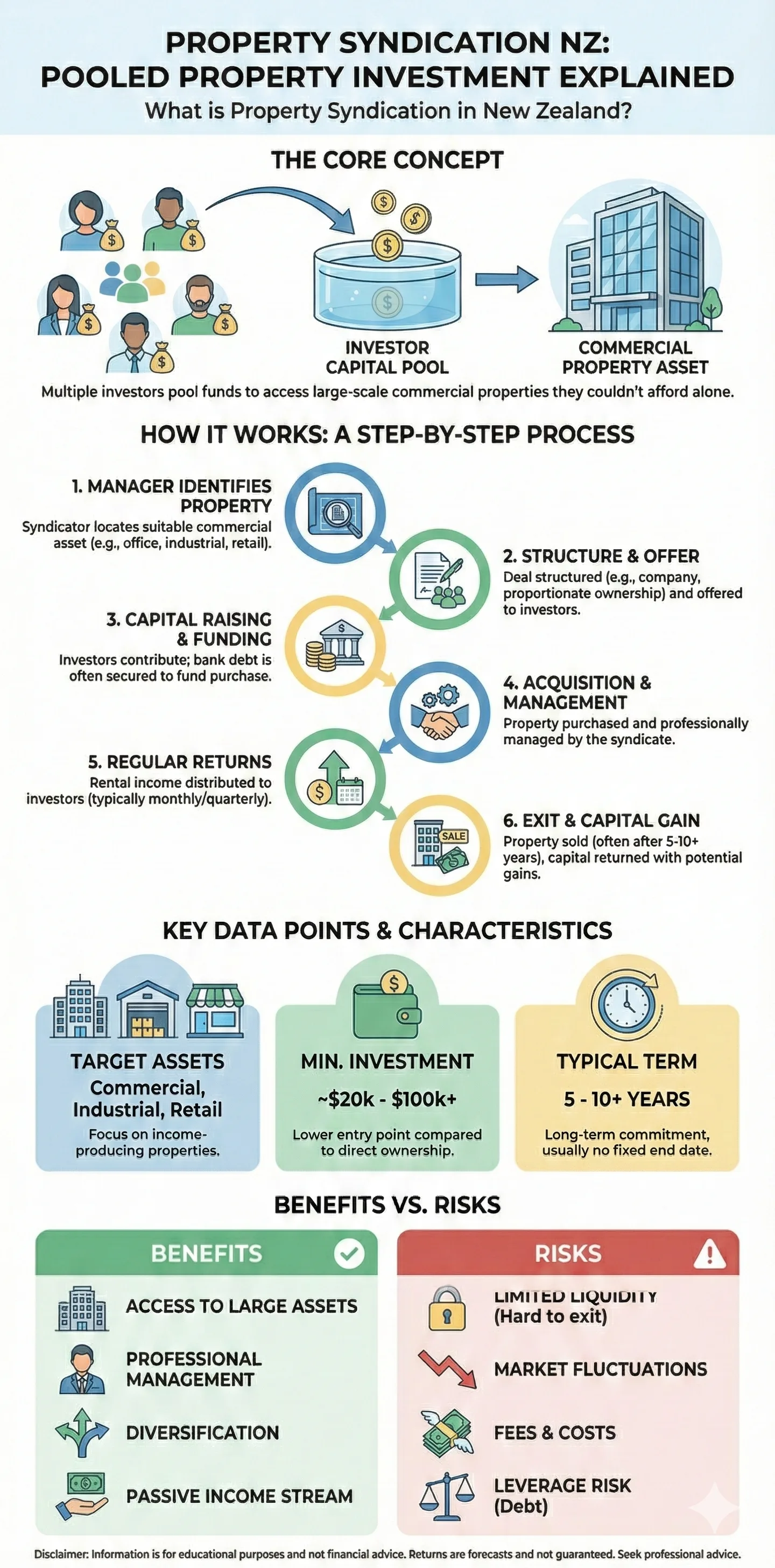

What is Property Syndication in New Zealand?

At its core, property syndication NZ involves a group of investors combining funds to purchase and manage a property, sharing both the rewards and responsibilities. A syndication company identifies a suitable asset—say, a $9.5 million office block in Wellington—secures a mortgage for part of it (e.g., $4 million), and raises the rest from investors. Each investor buys "interests" or shares, often registered on the property title, giving proportional ownership.

Syndicates target commercial, industrial, residential, or agricultural properties, including developments or established buildings. Unlike buying a family home, these are typically income-focused assets like retail centres or warehouses, generating rent to cover costs and distribute profits monthly—a welcome feature for retirees or those seeking passive income.

How Property Syndicates Are Structured

New Zealand syndicates operate under two main legal frameworks, each with distinct protections and disclosure requirements:

- Managed Investment Schemes (MIS): Run by an FMA-licensed manager, these offer units to retail investors. You'll get a Product Disclosure Statement (PDS) detailing operations, fees, and risks, plus a governing document and valuation report.

- Companies (Equity Syndicates): Investors buy shares in a company that owns the property. Disclosure is via a prospectus or investment statement, but oversight might be lighter unless it's wholesale-only.

Proportionate ownership schemes register each investor's share on the title, which can hike legal costs but mirrors direct ownership closely. Most syndicates focus on one property, though some hold portfolios, and involve 2 to 250 wholesale investors contributing $25,000 to $100,000+ per unit.

Historical players like Stride Property started in syndicates before listing, showing how these can evolve.

How Does Pooled Property Investment Work in Practice?

Here's a real-world example: XYZ Syndications spots a $9.5 million industrial warehouse in Christchurch. They secure a $4 million bank loan at current commercial rates (around 6-7% in 2026 amid stabilising conditions). The remaining $5.5 million comes from 220 investors at $25,000 each.

Post-purchase, rent covers the mortgage, management fees (typically 1-2% of gross rent), and distributions. Investors might see 5-8% annual yields from monthly payouts, net of costs. No fixed end date—syndicates run indefinitely until 75% vote to sell, returning capital after debts.

Income and Returns from Syndicates

- Rental Distributions: Monthly cash flow from tenants, often 80-90% of net rent paid out.

- Capital Gains: Profits from eventual sale, shared proportionally.

- Tax Treatment: Income is taxable; IRD treats syndicate interests like direct property ownership. Use KiwiSaver for diversification, but syndicates aren't eligible inside it. Bright-line test applies if sold within 10 years (2026 rules).

In 2026's balanced market, with more listings and steady incomes, syndicates shine for yield without the hassles of solo landlording.

Benefits of Property Syndication for Kiwi Investors

Pooled property investment democratises access to trophy assets:

- Affordability: Own part of a $10m+ building with $50k, versus saving millions alone.

- Passive Income: Professional managers handle tenants, maintenance—freeing you for KiwiSaver top-ups or family time.

- Diversification: Commercial properties often yield better than residential amid 2026's supply balance.

- Inflation Hedge: Rents and values rise with CPI, protecting against rising costs.

For wholesale investors (net assets $1m+ or income $200k+), minimums hit $100k, suiting high-net-worth Kiwis.

Risks and Downsides of NZ Property Syndicates

No rose-tinted glasses here—syndicates carry pitfalls, as seen in past flops like Maat Group or Nido warehouse.

- Illiquidity: Can't sell easily; stuck until majority votes to wind up. Unlisted status means no stock exchange exit.

- Extra Capital Calls: As part-owner, you might fund repairs or debts. Governing docs outline this—refusal could forfeit your stake and still owe money.

- Fees and Governance: Management fees erode returns; related-party directors may lack independence.

- Market Risks: Vacancies, interest rate hikes (e.g., post-2026 stimulus), or development delays.

- Wholesale Limits: Retail access only via licensed MIS; others for pros only.

Overseas Investment Act tweaks in 2026 ease some foreign buys but lock out farmland without big benefits—impacting syndicate targets.

Steps to Invest in a Property Syndicate in NZ (2026 Guide)

Ready to join? Follow these actionable steps:

- Check Eligibility: Wholesale? Prove via FMA questionnaire. Retail? Stick to licensed MIS.

- Research Syndicates: Review PDS, governing doc, valuation. Verify manager's FMA licence at fma.govt.nz.

- Assess the Property: Location, tenants, yield (aim 6%+ net). Get independent advice.

- Crunch Numbers: Factor fees, taxes, scenarios via IRD's property calculator.

- Diversify: Limit to 10-20% of portfolio; balance with KiwiSaver or term deposits.

- Sign Up: Minimum $25k-$50k; funds go to purchase.

Key Documents to Scrutinise

- Product Disclosure Statement: Ops, fees, risks.

- Governing Document: Capital calls, voting.

- Valuation Report: Fair market value.

Consult a financial adviser registered with FMA—don't go solo.

Property Syndication vs Other NZ Investments

| Investment Type | Minimum | Liquidity | Yield (2026 Est.) | Risk Level |

|---|---|---|---|---|

| Syndicate | $25k-$50k | Low | 5-8% | Medium-High |

| Direct Buy-to-Let | $800k+ (20-40% deposit) | Medium | 4-6% | High |

| KiwiSaver Property Funds | $1k | High | 4-5% | Medium |

| Listed REITs (e.g., Stride) | $500 | High | 5-7% | Medium |

Syndicates suit patient income-seekers; REITs for liquidity.

Tax Implications for Syndicate Investors

IRD views syndicate income as property-derived: rental shares are taxable at your marginal rate (10.5-39% in 2026). Deduct expenses proportionally. Capital gains on sale may trigger bright-line if under 10 years. Track via myIR; consider PIE status for some syndicates to cap tax at 28%.

Disclaimer: This isn't advice. See ird.govt.nz or a tax pro for your situation.

FAQ: Property Syndication NZ Questions Answered

Q: What's the typical minimum investment for property syndication NZ?

A: $25,000 to $50,000 for most, up to $100,000 for wholesale.

Q: Are property syndicates safe in 2026?

A: Regulated via FMA for MIS, but risks like illiquidity persist. Past issues highlight due diligence needs.

Q: Can I get monthly income from pooled property investment?

A: Yes, many distribute net rent monthly.

Q: How do I exit a syndicate?

A: Vote to sell (75% needed); no quick sales.

Q: Do syndicates qualify for KiwiSaver?

A: No, they're direct property—not fund-eligible.

Q: What's the FMA's role?

A: Licenses managers, enforces disclosure for retail schemes.

Is Property Syndication Right for You? Next Steps

If you're a Kiwi chasing yields above term deposits without full-time landlording, property syndication NZ merits a look—especially in 2026's steadier market. Start by visiting fma.govt.nz for licensed operators, chat with an authorised adviser, and run scenarios with your financial goals.

Remember, all investments carry risk. Diversify, seek pros, and never invest more than you can lose. Head to lifetimes.co.nz for more Money & Finance guides, or check IRD and FMA sites today.

Disclaimer: This article provides general information only. Property syndication involves significant risks, including loss of capital. Consult a licensed financial adviser and tax professional before investing. Rates and rules current as of 2026; verify with official sources.

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...