Property Valuations & LVR Explained

When you're buying a property in New Zealand, two terms you'll hear constantly are "property valuation" and "LVR" (Loan-to-Value Ratio). While they sound technical, understanding how they work togethe...

James writes about the New Zealand property market, renting, home ownership, and housing costs. He breaks down complex property topics into practical advice for renters and buyers.

When you're buying a property in New Zealand, two terms you'll hear constantly are "property valuation" and "LVR" (Loan-to-Value Ratio). While they sound technical, understanding how they work together is crucial—they directly affect how much you can borrow, what deposit you'll need, and whether your mortgage gets approved. Let's break down what these mean for Kiwi home buyers and investors.

What Is a Property Valuation?

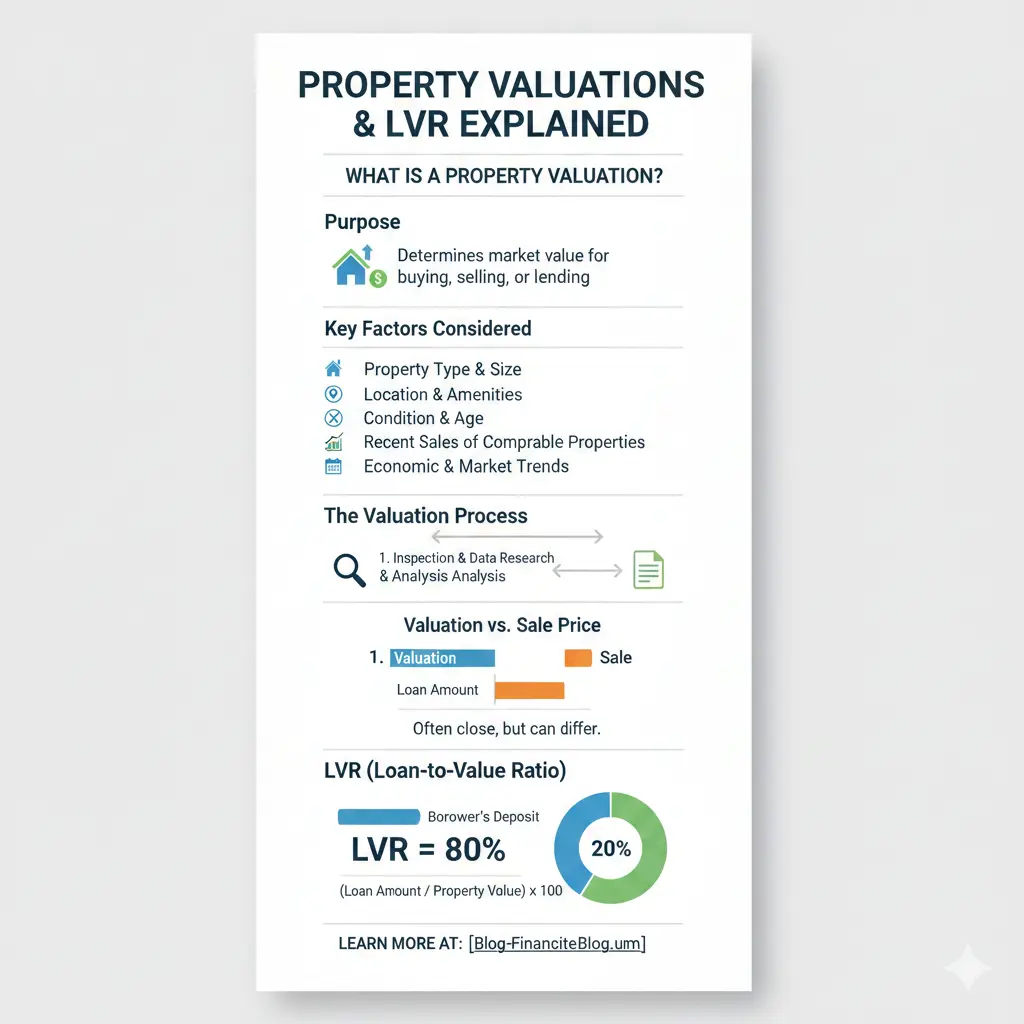

A property valuation is an independent assessment of what a property is worth. When you apply for a mortgage, your lender won't just take your word for it—they'll commission a registered valuer to assess the property and determine its market value. This valuation protects both you and the bank by ensuring the property is worth what you're paying for it.

The valuer will examine the property's condition, location, comparable sales in the area, and market trends. If you're buying a $700,000 home but the valuation comes back at $650,000, that's a red flag. The bank will only lend based on the lower valuation, which means you'll need a bigger deposit than you originally planned.

Understanding LVR (Loan-to-Value Ratio)

Your LVR is simply the percentage of a property's value that you're borrowing. The Reserve Bank sets limits on how much banks can lend relative to the property's value, depending on whether you're an owner-occupier or investor.

Current LVR Requirements in 2026

The Reserve Bank eased LVR restrictions from 1 December 2025, giving banks more flexibility. Here's what you need to know:

For Owner-Occupiers (buying your own home):

- You'll typically need a 20% deposit for both existing properties and new builds

- This means you can borrow up to 80% of the property's value

- Banks can now lend up to 25% of their new lending to borrowers with less than a 20% deposit (up from 20%)

- If you're a first-home buyer with a 5-19% deposit, you may qualify for special low-deposit options

For Property Investors:

- You'll need a 30% deposit for existing properties

- This means you can borrow up to 70% of the property's value

- For new builds, there are no LVR restrictions—you may be able to borrow with just a 20% deposit

- Banks can now lend up to 10% of their new lending to investors with less than a 30% deposit

How Property Valuation and LVR Work Together

Here's where it gets practical. Let's say you're buying an existing property valued at $700,000 as your first home.

Your 20% deposit = $140,000. You can then borrow up to 80% of the valuation = $560,000. Total purchase power: $700,000.

But what if the property is valued at only $680,000? Now your borrowing power drops to $544,000 (80% of $680,000). You'd need to either find an extra $16,000 for your deposit or negotiate a lower purchase price. This is why the valuation matters so much—it directly affects your borrowing capacity.

For investors, the impact is even more significant. With a 30% deposit requirement, the valuation determines exactly how much you can borrow. A $700,000 investment property valued at $650,000 means you can only borrow $455,000 instead of $490,000.

The LVR Formula: Calculate Your Purchasing Power

You can work out your maximum purchasing power using this simple formula:

Your Deposit ÷ Deposit Required % = Maximum Purchasing Power

Example for an owner-occupier:

If you have a $200,000 deposit and need 20%, then: $200,000 ÷ 0.20 = $1,000,000 purchasing power. You can spend up to $1 million on a property.

Example for an investor:

If you have a $200,000 deposit and need 30%, then: $200,000 ÷ 0.30 = $666,667 purchasing power. You can spend up to $667,000 on an existing investment property.

Notice how the same deposit gives owner-occupiers more purchasing power than investors? That's because owner-occupiers are seen as lower-risk borrowers.

Why These Rules Exist

The Reserve Bank introduced LVR restrictions back in October 2013 because it was concerned about rapidly rising house prices and the risks of low-deposit lending. The rules serve two purposes: they help keep the financial system stable, and they ensure borrowers have a decent financial buffer if property values fall.

The December 2025 easing of LVR rules reflects the fact that the financial system is in good shape. House prices are within a sustainable range, mortgage growth is moderate, and high-risk lending remains low. This gives banks a bit more flexibility to lend, particularly to first-home buyers.

What Happens When Valuations Don't Match Your Expectations

Property valuations can sometimes be lower than you expected. If this happens:

- You'll need a bigger deposit: If you budgeted for a 20% deposit but the valuation is lower, you might need to find extra cash or look at a cheaper property

- Your offer may be rejected: If you've made an unconditional offer based on a higher valuation, you could be in trouble

- You can challenge the valuation: If you believe the valuation is unfairly low, you can request the valuer reconsider, though this is rare

- Negotiate with the seller: You might ask the seller to reduce the price to match the valuation

This is why it's smart to get a pre-purchase inspection and research comparable properties before making an offer. Know the market value before you commit.

Special Cases and Exceptions

New Build Properties: There are no LVR restrictions for new builds, which means banks have more flexibility. In practice, you might be able to buy a new investment property with just a 20% deposit instead of 30%. This can be a significant advantage for investors.

Healthy Homes Compliance: If an existing property needs work to meet Healthy Homes Act standards, your bank may lend extra funds to bring it up to code, which can ease your borrowing constraints.

Debt-to-Income Limits: Since July 2024, the Reserve Bank also uses Debt-to-Income (DTI) ratios alongside LVRs. Even if you meet the LVR requirements, your overall debt commitments (including mortgage, car loans, credit cards, and other debts) can't exceed a certain multiple of your income. This is another layer of protection for borrowers.

Practical Tips for New Zealand Buyers

- Get pre-approved: Before you start looking, talk to your bank about your borrowing capacity based on your deposit and income. They'll factor in both LVR and DTI limits

- Budget for the valuation: Property valuations typically cost $400–$600 in New Zealand. Budget for this in your buying costs

- Don't rely on asking price: The asking price isn't the valuation. Research comparable sales in the area to get a realistic sense of value

- Make offers conditional on valuation: Unless you're in a hot market, try to make your offer conditional on the property valuing at or above your offer price

- Understand your DTI limits: With DTI rules now in place, your bank will look at your total debt picture, not just the mortgage. Pay down other debts if you can before applying

- Consider the new flexibility: The eased LVR rules from December 2025 mean slightly more low-deposit lending is available. If you're close to qualifying, it's worth talking to multiple banks

Next Steps

Understanding LVR and property valuations puts you in control of your home-buying journey. Before you start looking for properties, chat with your bank or mortgage broker about your specific situation. They'll work out your exact borrowing capacity considering both LVR and DTI limits, and they can explain any special schemes you might qualify for.

The eased LVR rules from December 2025 mean there's slightly more flexibility in the market right now, particularly for first-home buyers. If you've been saving for a deposit, this could be a good time to get serious about your property search. Get pre-approved, understand your limits, and you'll be ready to move quickly when the right property comes along.

Frequently Asked Questions

Sources & References

-

1

Loan-to-Value Ratio (LVR) Restrictions in New Zealand — www.opespartners.co.nz

-

2

New Zealand Reserve Bank to ease loan-to-value ratio restrictions — english.news.cn

-

3

Understanding loan-to-value ratio — www.kiwibank.co.nz

-

4

News in Focus: What the New LVR Rules Mean for First-Home Buyers — blog.healthcareplus.org.nz

-

5

LVR rules are loosening: What does this mean for borrowers? — www.christchurchinsurance.co.nz

-

6

LVR Rules Explained: Deposits, Low-Equity Lending, and What Changed from 1 December 2025 — www.newzealandmortgages.co.nz

Related Articles

First Home Grant NZ: How to Get Up to $10000

Buying your first home is one of the biggest financial decisions you'll make, and the New Zealand government wants to help. The First Home Grant puts up to $10,000 directly towards your deposit, makin...

Why 2026 is the Hardest Year to Buy a Home (and How to Beat the Odds)

Imagine standing at the edge of the property ladder in 2026, eyeing your dream home while prices hover stubbornly high, listings pile up, and buyer confidence wavers. For Kiwis, this year feels toughe...

Buying Your First Home in 2026: A Step-by-Step NZ Checklist

Imagine standing in your own Kiwi bach or cosy family home, keys in hand, after years of renting. In 2026, with interest rates stabilising and first-home schemes still strong, buying your first home i...

Selling Your Home? 10 Low-Cost Renovations That Add $50k in Value

If you're planning to sell your home in New Zealand, you don't need to break the bank with a complete renovation to attract buyers and boost your sale price. The good news? Some of the most effective...