How to Invest $1000 in New Zealand

Got $1000 burning a hole in your pocket? You're not alone—many Kiwis are looking to make their first investment move right here in Aotearoa. Whether you're saving for a house deposit, retirement, or j...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Got $1000 burning a hole in your pocket? You're not alone—many Kiwis are looking to make their first investment move right here in Aotearoa. Whether you're saving for a house deposit, retirement, or just want your money to work harder than a term deposit, starting small is smarter than you think. In 2026, with interest rates stabilising and markets opening up, there's never been a better time to dip your toes into investing.

This guide breaks down how to invest $1000 in New Zealand, from KiwiSaver tweaks to shares and managed funds. We'll cover practical steps, risks, and Kiwi-specific tips so you can build wealth without the overwhelm. Let's turn that grand into growth.

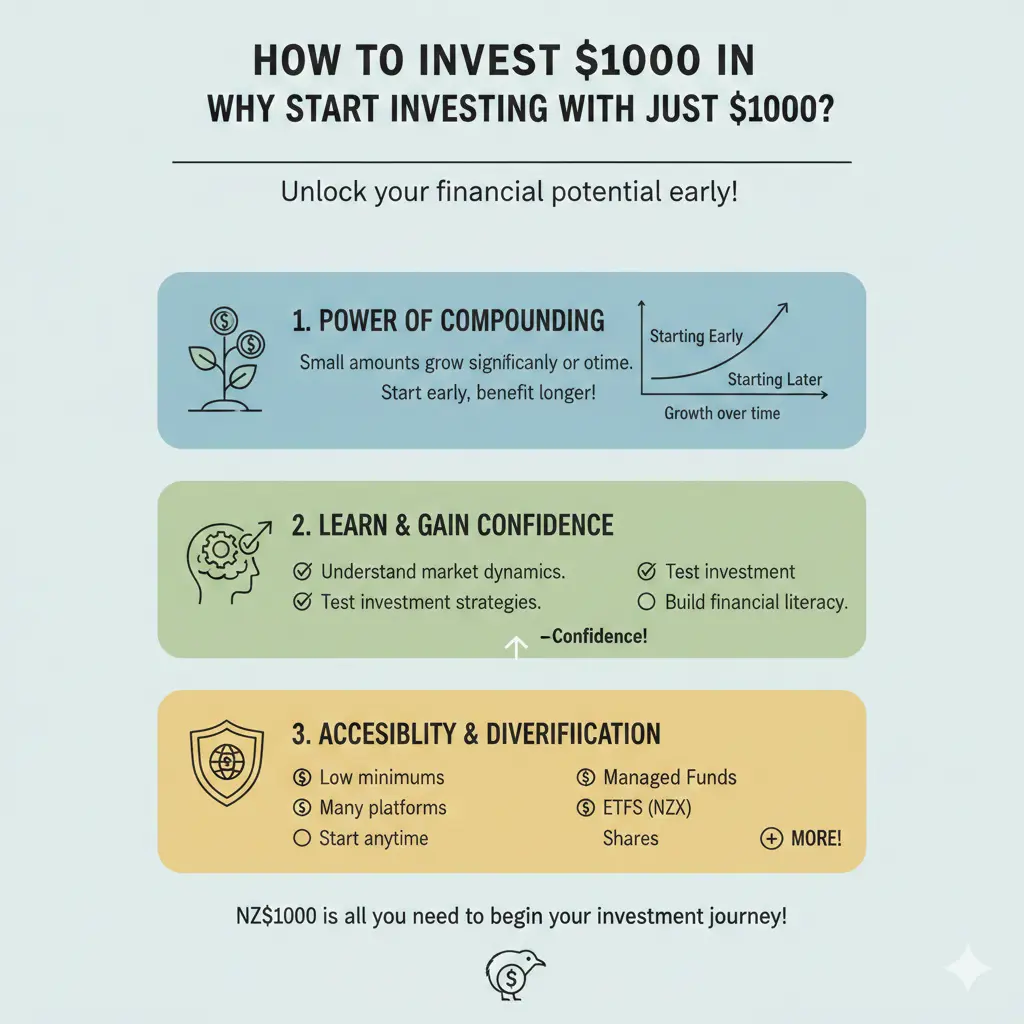

Why Start Investing with Just $1000?

Investing doesn't require a six-figure salary or a fancy advisor. In New Zealand, low-entry options mean anyone can start. Compound interest is your best mate here—$1000 invested at 7% annual return could grow to over $2000 in 10 years, or $7610 in 30 years, thanks to the magic of compounding.

Current 2026 conditions look promising: lower interest rates are boosting demand in housing, business, and tech sectors, while government reforms make NZ more investor-friendly. But remember, all investing carries risk—past performance isn't a crystal ball. Assess your risk tolerance first; if you're new, start conservative.

Key Benefits for Kiwis

- Accessibility: No minimums on many platforms, and apps make it easy.

- Tax perks: PIE funds (Portfolio Investment Entities) tax at your PIR (Prescribed Investor Rate), often lower than your income tax.

- Government support: KiwiSaver contributions get employer and government top-ups.

- Diversification: Spread $1000 across assets to manage risk.

Top 8 Ways to Invest $1000 in New Zealand (2026 Edition)

From Opes Partners' rundown of NZ's best investments to MoneyHub's 10 ways, here's what suits a $1000 starter stack. We've prioritised low-barrier options with real Kiwi examples.

1. Boost Your KiwiSaver

KiwiSaver is the no-brainer for most Kiwis—voluntary, with employer matches up to 3% and government contributions of $521 annually if you put in $1042. With $1000, switch to a growth fund or up your contributions.

How to do it:

- Log into your provider (e.g., Fisher Funds, with 25+ years managing KiwiSaver).

- Choose a growth fund—historically averaging 7-9% long-term.

- Invest $1000 as a lump sum or voluntary contribution.

Pros: Diversified, tax-efficient, locked for retirement (or first home). Cons: Can't access till 65 (unless hardship/home buy). Ideal for hands-off investing.

2. Managed Funds and ETFs

Managed funds pool money like KiwiSaver but without retirement locks. ETFs (Exchange-Traded Funds) track indices like the NZX 50. Platforms like Sharesies or Hatch let you buy from $1.

Example: Invest in Smartshares NZ Top 50 ETF (FNZ) for broad market exposure. In 2026, TMT (tech, media, telecom) and healthcare are hot, driven by AI and ageing population.

Steps:

- Sign up on Sharesies (free trades under $3000/month).

- Buy $1000 in diversified ETFs (e.g., 50% NZ shares, 50% global).

- Set auto-invest for $20/week.

Pros: Low fees (0.3-0.5%), instant diversification. Cons: Market volatility. Returns: 5-10% long-term.

3. Direct Shares on the NZX

Buy shares in Kiwi companies like Auckland Airport or Fisher & Paykel via Sharesies or ASB Securities. No minimum beyond brokerage (~$15-30/trade).

In 2026, focus on resilient sectors: renewables, healthcare. Avoid construction/retail headwinds.

Actionable tip: Allocate $500 to blue-chips (e.g., Contact Energy for green energy) and $500 to growth stocks. Use dividend reinvestment for compounding.

Pros: Ownership in NZ firms, dividends. Cons: Company-specific risk—diversify!

4. Term Deposits or Bonds

For low-risk, park in a term deposit. 2026 rates: around 4-5% for 12 months (check ASB or BNZ). Or government bonds via NZX Debt Market.

Quick start: $1000 in a 6-month term deposit at 4.5% earns ~$22 interest, PIE-taxed.

Pros: Capital guaranteed (under $500k via EGU). Cons: Inflation erodes real returns (currently ~2%). Best for emergency funds.

5. Peer-to-Peer Lending

Platforms like Squirrel or Harmoney let you lend $10+ to Kiwis/businesses, earning 8-12%.

Risk: Borrower defaults (platforms mitigate with provisions). Start with $1000 spread across loans.

6. Robo-Advisors and Index Funds

Hands-off: InvestEngine or Kernel Wealth build portfolios from $1000. They use algorithms for low-cost (0.25% fees) global/NZ mix.

2026 outlook: Strong for diversified index funds amid economic rebound.

7. Property-Related (REITs or Crowdfunding)

Direct property? Tough with $1000. Instead, REITs like Precinct Properties on NZX, or platforms like Fundour for commercial crowdfunding (min $1000).

Pros: Rental yields ~5% + growth. Cons: Property cycles—2026 housing demand rising but watch rates.

8. High-Interest Savings or Bitcoin Tilt (Advanced)

ASB, Kiwibank offer 4-5% savings accounts. For spice, some KiwiSaver like Compound's Global Growth + Bitcoin Tilt (small allocation).

Warning: Crypto volatile—not for $1000 core savings.

Risk, Tax, and Kiwi-Specific Rules

Understand your PIR for PIEs (0.5%, 10.5%, 17.5%, 28%)—check via IRD. No capital gains tax in NZ (yet), but dividends/Foreign Investment Fund (FIF) rules apply for overseas shares over $50k.

Risk levels:

| Option | Risk Level | Expected Return (2026) |

|---|---|---|

| Term Deposits | Low | 4-5% |

| KiwiSaver/Managed Funds | Medium | 6-8% |

| Shares/ETFs | Medium-High | 7-10% |

| P2P/Crowdfunding | High | 8-12% |

Overseas investment? Note Overseas Investment Act—no big changes for farmland, but pro-investment vibe. Golden Visa is for $5m+, not $1000.

Step-by-Step: Invest Your $1000 Today

- Assess goals/risk: Retirement? Home? Use free quizzes (e.g., Compound Wealth).

- Choose platform: Sharesies for shares/ETFs, your KiwiSaver app.

- Fund account: Bank transfer $1000.

- Diversify: E.g., $400 KiwiSaver, $400 ETFs, $200 term deposit.

- Monitor: Review yearly, rebalance.

- Seek advice: Free from Sorted.org.nz or call KiwiSaver provider.

Pro tip: Enable dollar-cost averaging—invest $100/month to smooth volatility.

Common Pitfalls to Avoid

- Chasing hot tips (e.g., avoid 2026's "worst" like retail).

- Ignoring fees—aim under 1% p.a.

- Panic selling—hold 5-10 years.

- Forgetting inflation (target 4%+ real returns).

Next Steps to Grow Your Wealth

Congrats—you're ready! Open a Sharesies account or log into KiwiSaver today. Start small, stay consistent, and watch compounding work. For personalised advice, chat to a financial adviser via Financial Advice NZ. Track progress with apps like PocketSmith. In NZ, we're in this together—happy investing!

Frequently Asked Questions

Sources & References

-

1

Top 8 Best Investments in New Zealand (2026) | Opes Partners — www.opespartners.co.nz

-

2

New Zealand Golden Visa 2026: Residency by Investment — getgoldenvisa.com

-

3

Investing In... 2026 - New Zealand - Chambers Global Practice Guides — practiceguides.chambers.com

-

4

Best Investment Options for Retirement Planning in 2026 — www.compoundwealth.co.nz

-

5

10 Ways to Invest in New Zealand - MoneyHub NZ — www.moneyhub.co.nz

-

6

Active Investor Plus Visa overview - Immigration New Zealand — www.immigration.govt.nz

-

7

The 6 Worst Places to Invest in NZ for 2026 (The Data Is Brutal) — www.youtube.com

-

8

Choices for the next term, pathways for the next decade [PDF] — www.treasury.govt.nz

-

9

New Zealand fixed income outlook 2026 [PDF] — nz.amova-am.com

Related Articles

Ethical Investing in NZ: Top 5 Sustainable Funds for Kiwis

Ever wondered if you can grow your KiwiSaver or investments while doing good for the planet and people? Ethical investing in New Zealand is booming, with Kiwis pouring billions into funds that priorit...

Beginner's Guide to Investing in New Zealand

Getting started with investing in New Zealand doesn't have to be complicated. Whether you're looking to grow your wealth, save for retirement, or build financial security, there are plenty of accessib...

How to Buy Shares in New Zealand: Step-by-Step Guide

Ever wondered how to dip your toes into share investing without getting overwhelmed? Whether you're saving for a house deposit, retirement, or just want to grow your hard-earned cash, buying shares in...

ETFs vs Managed Funds: Which is Better for Kiwi Investors?

When you're ready to invest your money, you'll likely come across two main options: exchange-traded funds (ETFs) and managed funds. Both offer diversification and professional management, but they wor...