Downsizing Your Home: A Financial and Practical Guide

Imagine waving goodbye to the empty bedrooms and sprawling garden of your family home, unlocking a simpler life filled with more travel, hobbies, and financial freedom. For many Kiwis, downsizing your...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Imagine waving goodbye to the empty bedrooms and sprawling garden of your family home, unlocking a simpler life filled with more travel, hobbies, and financial freedom. For many Kiwis, downsizing your home isn't just about shrinking square metres—it's a smart move to align your living space with your current lifestyle while boosting your bank balance. In New Zealand's dynamic property market, this transition can release equity for retirement dreams, but it requires careful planning to maximise financial gains and minimise stress.

Whether you're an empty nester in Auckland eyeing a compact villa or a couple in Christchurch considering a rural cottage, this guide delivers practical steps, Kiwi-specific insights, and 2026 financial realities to make downsizing your home seamless and rewarding.

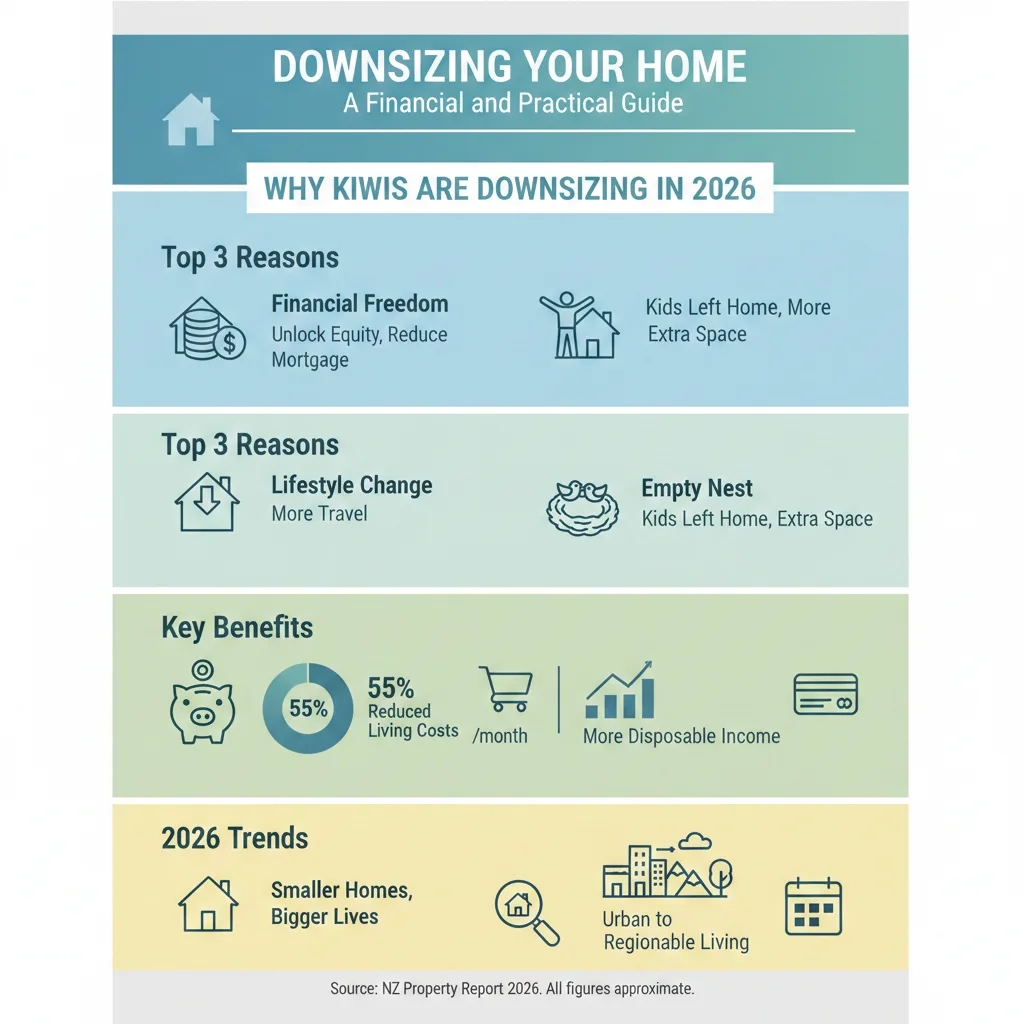

Why Kiwis Are Downsizing in 2026

New Zealand's housing market remains robust, with median house prices hovering around $850,000 nationally, though regional variations apply—Auckland at $1.05 million, Wellington $750,000, and smaller centres like Wānaka offering more affordable options from $600,000. Empty nesters and retirees are leading the charge, driven by rising maintenance costs, council rates averaging $3,500 annually for larger homes, and a desire for low-maintenance living.

Downsizing frees up equity—potentially $300,000–$500,000 after selling a four-bedroom home and buying a two-bedroom unit—ideal for bolstering KiwiSaver or funding adventures abroad. Yet, as experts note, it's not always a windfall; transaction costs can eat 5–10% of proceeds.

Financial Upsides and Hidden Costs

- Equity Release: Sell high, buy low—use proceeds for debt reduction, KiwiSaver top-ups, or income streams via annuities.

- Lower Bills: Expect 20–30% savings on power (around $2,000/year), rates, and insurance in a smaller home.

- Tax Implications: No capital gains tax on your primary residence, but bright-line test applies if you've flipped recently (10 years for post-2021 buys). Consult IRD for personalised advice.

- Costs to Watch: Real estate commissions (2–3% + GST), legal fees ($1,500–$2,500), moving ($2,000–$5,000), and potential repairs.

Step-by-Step Practical Guide to Downsizing

Success hinges on preparation. Start 6–12 months ahead to avoid rushed decisions.

Step 1: Assess Your Needs and New Space

Evaluate lifestyle: Do you crave urban buzz or rural peace? Measure your target home's rooms and doorways—many Kiwis overlook this, leading to oversized furniture woes. Visualise with floor plans; apps like Room Planner help. In NZ, options abound: standalone units, retirement villages like Aspiring in Wānaka, or portable cabins for "downsizing without moving".

Actionable Tip: Tour properties early. For retirement villages, check occupation right agreements—weekly fees average $600–$900 in 2026, covering maintenance.

Step 2: Declutter Ruthlessly

Decluttering is the emotional core of downsizing. Use the "Six-Month Rule": If you haven't used it in six months, it's unlikely you will. Adopt the Four-Box Method: Keep, Donate, Sell, Discard.

- Start Small: Tackle wardrobes first—turn hangers backwards; unworn items after 2 months go.

- Kitchen Hack: Place utensils in a box as used; unclaimed after weeks are gone.

- Sentimentals: Digitise photos/letters for cloud storage, keeping physical favourites.

- Make it Fun: Host a "declutter day" with whānau, bacon and egg pie included.

Platforms like Trade Me, Facebook Marketplace, or Salvos stores turn clutter into cash—Kiwis earn $1,000–$5,000 this way. Donate to Vinnies or SPCA for tax receipts if itemised.

Step 3: Innovative NZ Downsizing Options

Forget cookie-cutter apartments; NZ offers creative paths.

- Retirement Villages: Low-entry villas from $400,000 in regions like The Botanic, with communal facilities.

- Portable Cabins: Install a 60–100sqm insulated cabin in your backyard ($80,000–$150,000). Rent the main house for $600–$900/week, generating $30,000+ annual income without moving.

- Rural Retreats: Farmlets or sleep-outs provide space without upkeep—median $500,000 in Waikato.

- Urban Units: Compact townhouses under $700,000 in Christchurch.

Pro Tip: For cabins, ensure council consents (Resource Management Act compliant); shared facilities work well for family or tenants.

Step 4: Selling and Moving Smartly

Choose agents via REINZ recommendations—expect 4–6 weeks on market in 2026. Pack strategically: label by room, essentials last. Hire movers like Wise Move for senior specials ($3,000 average).

Financial Planning for Maximum Benefit

Downsizing amplifies retirement security. Here's how to optimise:

Equity Management

Post-sale windfall? Allocate wisely:

| Option | Pros | Cons | NZ Example |

|---|---|---|---|

| KiwiSaver Boost | Govt contributions up to $521/year; compounds tax-free | Locked till 65 | Add $100k for 7% growth = $200k by retirement |

| PAYG Income | 4–5% returns; flexible access | Inflation risk | Annuities via AMP: $400k yields $20k/year |

| Travel/Debt Fund | Immediate lifestyle boost | No growth | Clear mortgage, save ACC levies |

Bright-line exemptions apply to main homes; track via myIR. WINZ pensions may adjust if assets exceed $300,000 threshold—seek advice.

Costs Breakdown (2026 Estimates)

- Selling: 2.5% commission + $1,800 marketing = $25,000 on $1m sale

- Buying: $2,000 LIM/RV checks + $2,500 legal

- Moving/Storage: $3,000–$7,000

- Total: 5–8% of equity

Disclaimer: This is general info. Consult a financial adviser or IRD for tailored advice on tax, KiwiSaver, and entitlements.

Overcoming Emotional Hurdles

Leaving your family home stirs emotions—memories in every corner. Start with support: involve whānau or pros like professional organisers ($50–$100/hour). Focus on gains: more time for grandkids, golf, or OE. Many report newfound freedom post-move.

FAQ

1. How much can I save by downsizing?

Typically $20,000–$40,000/year in bills, plus $200k+ equity.

2. Do I pay tax on downsizing profits?

No, for primary residences outside bright-line (10 years post-2021).

3. What's the best way to declutter fast?

Four-Box Method + Six-Month Rule; sell on Trade Me.

4. Can I downsize without selling my home?

Yes, via backyard cabins—rent main house for income.

5. Are retirement villages worth it?

For low-maintenance living, yes—fees cover upkeep, but check exit terms.

6. How do council rules affect cabins?

Need consents; flat site ideal, compliant with RMA.

Next Steps to Downsize Successfully

Ready to act? List three must-keep items, measure dream spaces, and chat with a REINZ agent. Calculate equity via Opes Partners tools, then declutter one drawer today. Your lighter, brighter future awaits—professional advice ensures it's financially sound.

Always seek personalised financial advice from an authorised adviser, IRD, or WINZ before proceeding.

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...