Managing Money as a Couple: Joint Finance Strategies

Navigating finances together can strengthen your relationship or spark tension—depending on how you approach it. For Kiwi couples, mastering managing money as a couple: joint finance strategies means...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Navigating finances together can strengthen your relationship or spark tension—depending on how you approach it. For Kiwi couples, mastering managing money as a couple: joint finance strategies means blending practicality with open communication, especially amid rising living costs and unique New Zealand financial tools like KiwiSaver and IRD tax rules.

Whether you're saving for a first home deposit, juggling family expenses, or planning retirement, joint strategies help align your goals. This guide breaks down proven approaches tailored for Kiwis, drawing on local banking options and real-world advice to make your money work harder for both of you.

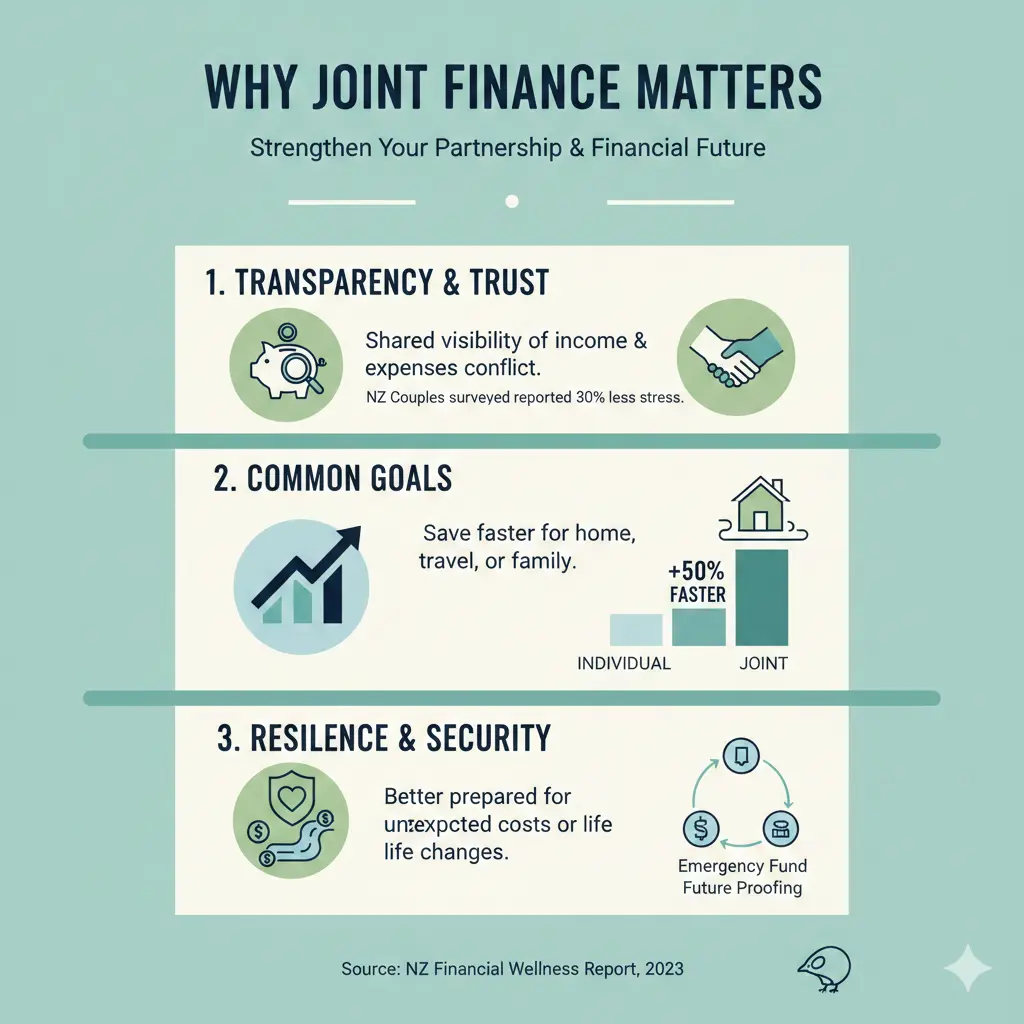

Why Joint Finance Strategies Matter for Kiwi Couples

Combining finances isn't just about pooling cash—it's about building trust and shared purpose. In New Zealand, where household costs like rent in Auckland average over $600 weekly and groceries have risen 5-7% annually, couples who coordinate finances report lower stress and faster progress toward goals like home ownership. A 2026 survey by the Banking Ombudsman Scheme highlights that clear joint account setups reduce disputes during breakups, protecting both parties.

Joint strategies also optimise tax benefits. For instance, contributing to a shared KiwiSaver account can maximise government contributions, while splitting income via IRD rules might lower your combined tax bracket. But success hinges on compatibility: couples with similar spending habits thrive, while mismatches need boundaries.

Benefits of Aligning Your Money Mindsets

- Shared visibility: Track bills and savings in one place via apps like ANZ goMoney or BNZ online banking.

- Efficiency: Automate household payments from a joint account, freeing time for what matters.

- Goal acceleration: Pool funds for big wins, like a house deposit under KiwiBuild schemes.

- Equity: Proportional contributions based on income ensure fairness.

Joint Bank Accounts: The Foundation of Shared Finances

Joint bank accounts are popular among Kiwi couples for handling everyday shared costs. MoneyHub notes they're ideal for rent, groceries, and utilities, with most major banks offering them for transaction, savings, or term deposit purposes. In 2026, options from BNZ, ASB, Kiwibank, ANZ, and Westpac make setup straightforward, often online or in-branch.

How to Open a Joint Account in New Zealand

Opening is simple but requires verification for all holders. Here's the step-by-step:

- Choose your bank: BNZ allows phone or online applications; select "Me and someone else." ASB requires a branch visit for new customers.

- Gather ID: Bring NZ driver's licence, passport, birth certificate, or student ID, plus proof of address like IRD statements or utility bills.

- Verify together: Kiwibank needs both parties in-branch or via app messaging. ANZ offers online for existing customers.

- Fund and set rules: Decide contributions—equal splits or income percentages.

"Dollars in a joint account are owned together. Every account holder is entitled to all the money and liable for all the debt."

Types of Joint Accounts for Couples

| Account Type | Best For | NZ Bank Examples |

|---|---|---|

| Transaction | Daily bills (rent, power, Netflix) | BNZ Everyday, ANZ Visa Debit |

| Savings | Home deposit, holidays | ASB FastSave, Kiwibank Notice Saver |

| Term Deposit | Locked savings for goals | Westpac, ANZ |

Pro tip: Keep personal accounts alongside joint ones for individual spending—MoneyHub recommends this hybrid for flexibility.

Pros and Cons of Joint Accounts

ASB outlines key risks: all holders share liability for debts, even if one partner racks them up. If a relationship ends, you're jointly responsible until settled. On death, funds pass to survivors, bypassing wills in some cases.

Advantages

- Simplified bill splitting and visibility.

- Builds discipline through mutual accountability.

- Tax perks on joint investments via IRD.

Risks and How to Mitigate Them

- Debt liability: Check partner's credit history via Equifax before opening.

- Breakup complications: Banking Ombudsman advises pre-nups or clear agreements.

- Trust issues: Set guidelines: e.g., no withdrawals over $200 without discussion.

- Protection: Never share PINs; monitor via apps.

Advanced Joint Finance Strategies for Kiwis

Beyond basics, integrate NZ-specific tools. For retirement, align KiwiSaver—couples can consolidate providers for better fees, targeting 2026 contribution rates of up to $521 weekly per person.

Budgeting Together: Proportional Contributions

Use the 50/30/20 rule adapted for couples: 50% needs (joint account), 30% wants (personal), 20% savings/debt. Super Advice suggests funding joint accounts proportionally—e.g., if one earns $80k and the other $50k, contribute 60/40. Apps like PocketSmith (NZ-made) sync joint and personal data.

KiwiSaver and Investments as a Couple

Joint KiwiSaver isn't direct, but nominate each other as beneficiaries via IRD. For 2026, couples maximise $521 gov't top-ups by salary sacrificing. Consider joint term deposits yielding 4-5% or ethical funds via Generate.

Handling Debt and Insurance

Joint loans? ACC and insurance like AA cover households—list both partners. For mortgages, split via relationship property laws under the Property (Relationships) Act 1976; seek legal advice.

WINZ benefits for couples (e.g., Jobseeker) calculate combined income—use their calculator for 2026 rates.

Tax Optimisation

IRD's 2026 brackets: 10.5% up to $15,600; 17.5% to $53,500. Couples filing separately might save via Working for Families credits. Track via myIR portal.

Communication: The Glue Holding It All Together

MoneyHub stresses matching attitudes—discuss via monthly "money dates." Capsule NZ reports most couples use hybrid accounts amid cost-of-living pressures.

- Set shared goals: e.g., $50k house deposit in 3 years.

- Use tools: Shared Google Sheets or BNZ alerts.

- Review quarterly: Adjust for life changes like kids or job loss.

Common Pitfalls and How to Avoid Them

- Mismatched habits: Spender/saver? Allocate "fun money" pots.

- No exit plan: Document agreements; close joint accounts amicably.

- Over-reliance: Maintain emergency funds in personal accounts (3-6 months expenses).

- Ignoring inflation: 2026 forecasts 2-3%; prioritise high-interest savings.

Next Steps to Master Your Joint Finances

Start small: Open a joint transaction account this week with BNZ or ANZ. Schedule a money date, list top 3 goals, and run numbers via IRD's tax calculator. Consult a financial adviser for personalised KiwiSaver tweaks—remember, this isn't advice; seek pros for your situation.

Track progress monthly, celebrate wins like clearing a bill, and adjust as life evolves. With these strategies, you'll turn money management into a team sport that builds your future.

Disclaimer: This guide uses 2026 data; tax and rates change. Always verify with IRD, your bank, or a certified adviser for tailored advice.

Frequently Asked Questions

Sources & References

-

1

Best Joint Bank Accounts - MoneyHub NZ — www.moneyhub.co.nz

-

2

Opening a joint account - BNZ — www.bnz.co.nz

-

3

Joint bank accounts in NZ - Guide - ASB — www.asb.co.nz

-

4

Banking Strategies as a couple - Super Advice New Zealand — super-advice.co.nz

-

5

Join Kiwibank - Open your joint account — www.kiwibank.co.nz

-

6

Joint bank accounts | Everyday banking - ANZ — www.anz.co.nz

-

7

$1042 for Couples in 2026: Updated NZ Super Payments Explained — www.artbeat.org.nz

- 8

-

9

2026 Media releases | Banking Ombudsman Scheme — bankomb.org.nz

-

10

Joining your finances together - Westpac — www.westpac.co.nz

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...