Motorcycle Insurance NZ: Complete Guide for Riders

Motorcycle insurance in New Zealand isn't legally required, but it's absolutely worth having—especially when basic third-party cover can cost as little as a few dollars a week. Whether you're commutin...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Motorcycle insurance in New Zealand isn't legally required, but it's absolutely worth having—especially when basic third-party cover can cost as little as a few dollars a week. Whether you're commuting on a learner bike or touring the country on a high-powered machine, understanding your insurance options could save you thousands of dollars and protect you from serious financial risk.

Why Motorcycle Insurance Matters in New Zealand

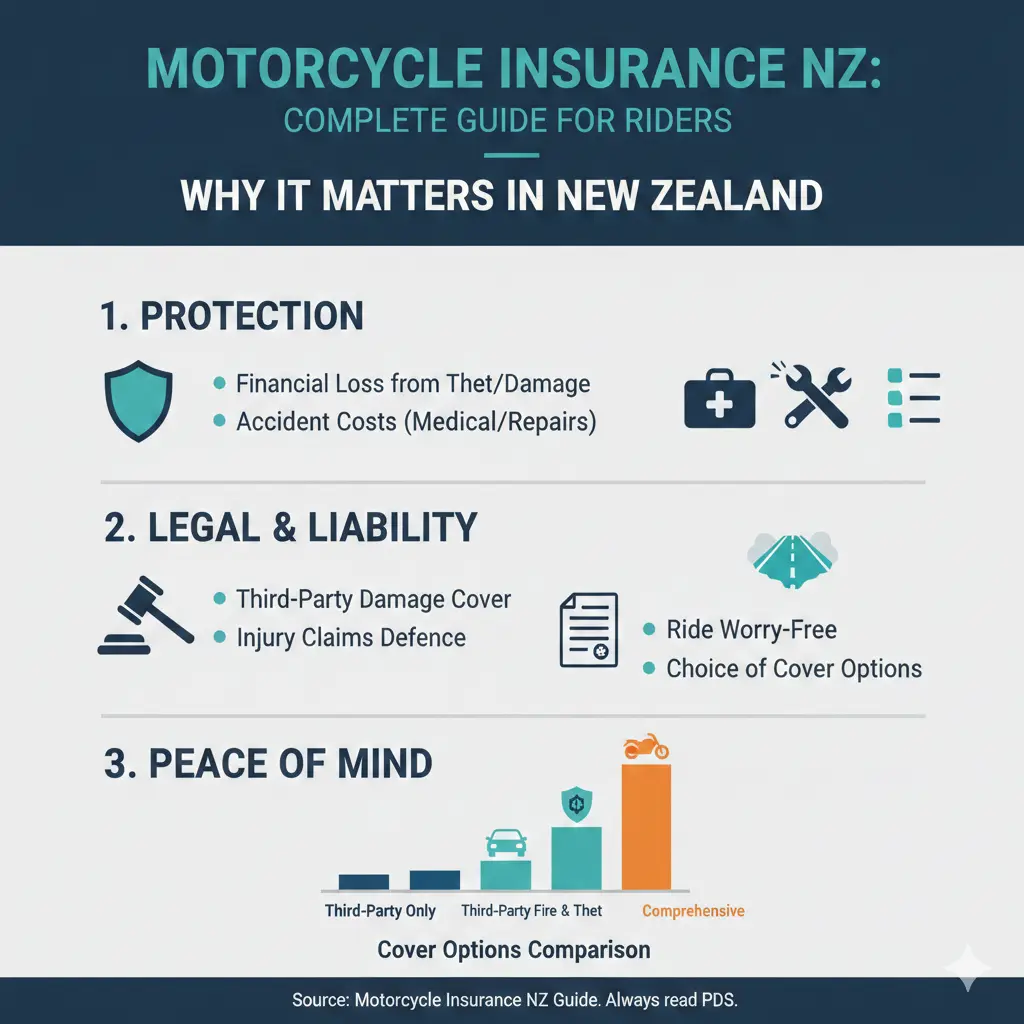

Unlike car insurance, motorcycle coverage isn't compulsory on New Zealand roads. However, riding without insurance is a risk that simply isn't worth taking. If you're involved in an accident and cause damage to someone else's property or injure another person, you could be liable for substantial costs—potentially tens of thousands of dollars.

It's also important to understand the difference between motorcycle insurance and ACC (Accident Compensation Corporation). While ACC covers personal injury from motorcycle accidents through levies included in your registration fee, motorcycle insurance covers property damage, theft, fire, and liability to others—not your own medical treatment.

Registration for motorcycles in New Zealand must include the ACC levy, which ranges from $420 to $600 annually depending on your bike's engine capacity. This provides injury coverage, but you'll still need separate motorcycle insurance to protect your bike and cover your liability to others.

Understanding Your Motorcycle Insurance Options

Motorcycle insurance in New Zealand typically comes with three main coverage levels, each offering different trade-offs between cost and protection.

Third-Party Only

This is the most basic and cheapest option, costing as little as $150 per year. Third-party insurance covers damage you cause to another person's property or vehicle, but provides no protection for your own bike. This option leaves you fully exposed if your motorcycle is damaged, stolen, or involved in an accident.

Third-party only makes sense if you're riding an older, low-value bike and can afford to replace it out of pocket if something goes wrong.

Third-Party Fire and Theft (TPFT)

This middle-ground option balances cost and core protection. TPFT covers damage to other people's property, plus protection if your bike is stolen or damaged by fire. It's a popular choice for riders who want more security than third-party alone but don't want to pay for comprehensive coverage.

TPFT is particularly valuable if your bike is stored outside or in an unsecured location, as theft and weather damage are real risks in New Zealand.

Comprehensive Cover

Comprehensive insurance offers the highest level of protection, covering accidental damage, vandalism, theft, fire, and liability to others. It typically includes extras like towing costs, helmet and riding gear replacement, lost key cover, and road clearing costs.

Comprehensive insurance ranges from $500 to $1,500 annually, depending on your bike's value, your age, and your riding history. For most riders in New Zealand, annual comprehensive motorcycle insurance ranges from $400 to $900 for a $10,000 bike.

Comprehensive cover is worth considering if your bike is newer than five years old or valued above $8,000. Some insurers also offer a two-year replacement guarantee—if your new motorbike is written off within the first two years, they'll replace it with a brand-new bike of the same make, model, and variant.

Factors That Affect Your Motorcycle Insurance Cost

Several factors influence how much you'll pay for motorcycle insurance in New Zealand:

- Your age and experience: Riders under 25 typically pay significantly higher premiums, as do those with less riding experience.

- Your bike's value and engine capacity: High-CC bikes and newer, more valuable motorcycles attract higher premiums.

- Your location: Urban areas with higher theft rates may result in higher premiums than rural locations.

- Your riding history: A clean record with no accidents or claims will keep your premiums lower.

- Security measures: Secure storage, alarms, and GPS trackers can reduce your premium.

- Safety training: Completing an approved rider training course like Rider Forever may lower your premiums with certain insurers such as AA or Star Insurance.

- Excess amount: Choosing a higher voluntary excess will lower your premiums, but means you'll pay more if you make a claim.

Choosing the Right Coverage for Your Situation

The best insurance option depends on your specific circumstances. Here's how to think through your decision:

If You're a New Rider Under 25

Start with third-party fire and theft (TPFT) rather than jumping straight to comprehensive. This keeps your costs down while you build your riding history and experience. Once you've got a few years of clean riding under your belt, you can reassess and potentially move to comprehensive if your bike's value justifies it.

If You're an Experienced Rider Over 40 with a Clean Record

You'll likely qualify for the lowest premium rates available. Compare comprehensive versus TPFT pricing—you may find that comprehensive cover doesn't cost much more than TPFT, making it the better value.

If Your Bike Is Stored Outside or Unsecured

Prioritise theft and fire coverage. Consider combining TPFT with a portable lock and GPS tracker combo for added security and potential premium discounts.

If You Commute Daily

Your higher exposure to risk makes a stronger case for comprehensive coverage. The extra protection is worth the additional cost when you're relying on your bike for regular transport.

Important Legal and Safety Considerations

Warrant of Fitness (WoF)

Your motorcycle's WoF must be up to date. A lapsed WoF can invalidate your insurance coverage in some cases, so make sure you stay on top of your annual inspections.

Modifications

Any performance or cosmetic modifications to your bike must be declared to your insurer. Failing to disclose modifications could result in claim denial, even if the modification wasn't related to the incident.

Safety Training

Completing an approved course like Rider Forever may reduce your premiums with certain insurers. Even without a discount, improved skills reduce your accident risk—the best long-term cost saver.

ACC Levies

ACC levies are paid annually through your registration fees and are higher for motorcycles due to injury risk. This is separate from your motorcycle insurance but is a mandatory cost of bike ownership.

Getting the Best Quote

Follow these steps to find the right motorcycle insurance at the best price:

- Determine your bike's current market value using TradeMe Motors as a reference.

- Select your preferred coverage level based on your bike's age and how you use it.

- Gather at least three quotes from different insurers to compare options and pricing.

- Confirm whether ACC levies are included in your registration or billed separately.

- Ask about discounts for secure storage or completion of approved rider training courses.

- Review excess amounts—understand that a higher voluntary excess will lower your premiums but means you'll pay more out of pocket if you need to claim.

- Double-check policy exclusions, particularly around track use or modified parts.

Major New Zealand insurers offering motorcycle cover include AA Insurance, Tower, AMI, State, Protecta Insurance, Swann Insurance, and Kiwibike. Taking time to compare their offerings will help you find the best fit for your needs and budget.

Your Next Steps

Protecting your motorcycle and managing your liability doesn't have to be complicated. Start by determining your bike's current value, deciding what level of coverage makes sense for your situation, and gathering quotes from at least three insurers. Remember that the cheapest option isn't always the best—make sure your coverage actually protects you against the risks that matter most.

If you're new to motorcycling, consider investing in a Rider Forever course. The improved skills could save you from an accident far more effectively than any insurance policy, while potentially lowering your premiums at the same time.

Disclaimer: This article provides general information about motorcycle insurance in New Zealand. Insurance policies vary between providers, and your circumstances are unique. We recommend comparing quotes from multiple insurers and seeking professional financial advice before making a decision about your motorcycle insurance coverage.

Frequently Asked Questions

Sources & References

-

1

Is Motorcycle Insurance Different From Car Insurance? — Canstar — www.canstar.co.nz

-

2

How Much Is Motorbike Insurance in NZ? A Practical Guide — Alibaba — carinterior.alibaba.com

-

3

The Cost of Motorcycling in New Zealand - THE BIKER GUIDE — www.thebikerguide.co.uk

-

4

Motorbike Insurance — MoneyHub NZ — www.moneyhub.co.nz

-

5

Motorbike & Motorcycle Insurance — Tower Insurance NZ — www.tower.co.nz

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...