Negative Gearing Removal NZ: What It Means for Investors

When New Zealand's Labour Government phased out negative gearing for residential investment properties, it fundamentally changed the landscape for property investors across the country. If you're cons...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

When New Zealand's Labour Government phased out negative gearing for residential investment properties, it fundamentally changed the landscape for property investors across the country. If you're considering investing in rental property or already have investment properties, understanding how this policy works—and how it affects your tax position—is essential. Let's break down what negative gearing removal means for you as a Kiwi investor.

What Is Negative Gearing?

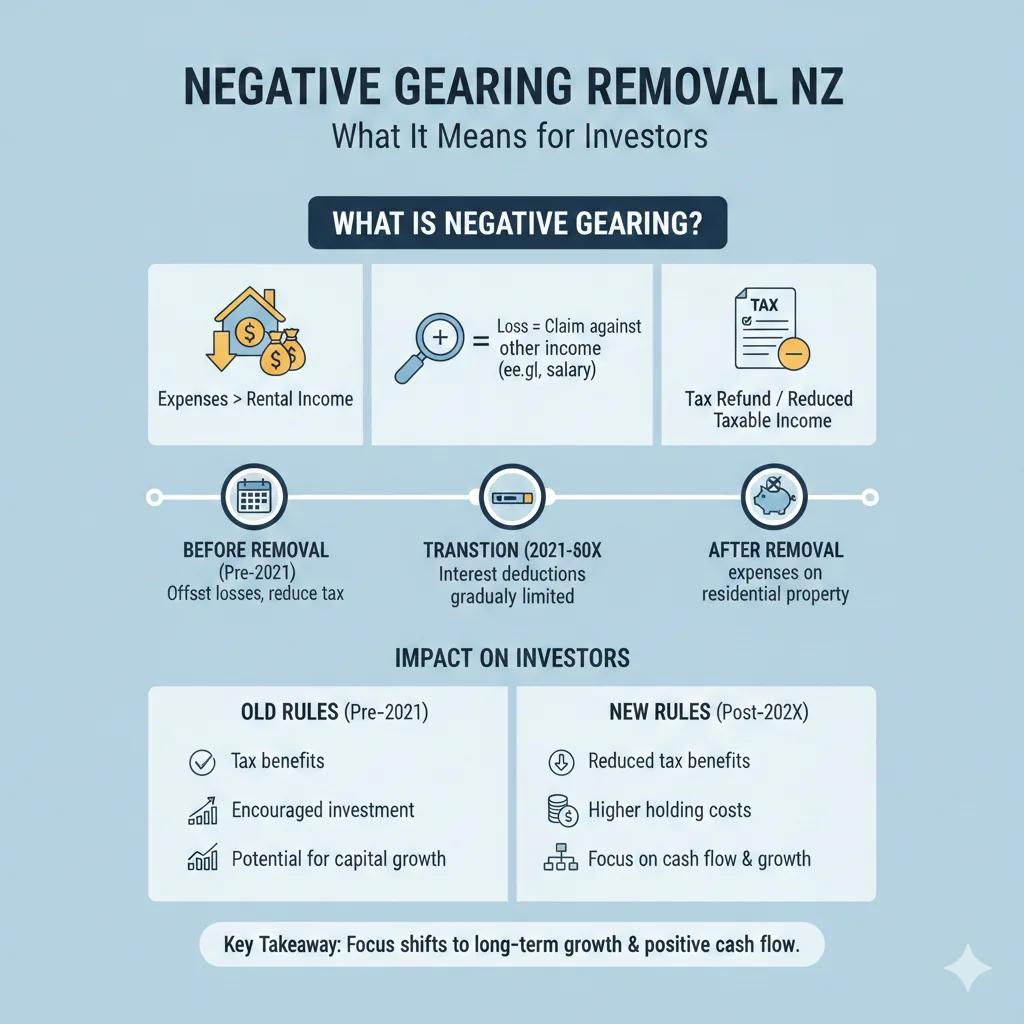

Negative gearing is when the costs of maintaining a rental property exceed the income you receive from rent. Before the law changed, investors could use this shortfall to claim a tax deduction against their other income—such as wages or salary. This meant you could reduce your overall tax bill by offsetting investment losses against your earned income.

For example, if you earned $80,000 per year and your rental property generated a $10,000 loss, you could previously deduct that loss from your salary, reducing your taxable income to $70,000. This was seen as a significant financial advantage for property investors compared to first-home buyers saving to enter the market.

When Did Negative Gearing End in New Zealand?

New Zealand's ring-fencing of losses law came into effect on 1 April 2019. However, the government introduced a phased approach for properties acquired before the policy change was announced on 27 March 2021.

Here's the timeline you need to know:

- Properties acquired before 27 March 2021: Interest deductions were phased out between 1 October 2021 and 31 March 2025.

- Properties acquired on or after 27 March 2021: Interest cannot be claimed from 1 October 2021 onwards.

- New loans drawn down on or after 27 March 2021: Interest deductions for new borrowings aren't allowed from 1 October 2021 onwards.

By now in 2026, the phasing out period has concluded, and the rules are fully in effect for all investment properties.

How Ring-Fencing Works Now

Instead of disappearing entirely, your rental losses are now "ring-fenced"—meaning they're separated from your personal income and can only be offset against future rental income from your investment properties.

Here's what this means in practice:

- You can't claim rental losses against your wages or salary

- Losses can only be deducted from future rental income you earn

- Losses can be carried forward indefinitely until you have enough rental income to offset them

- When you sell the property, remaining losses cannot be applied to your capital gain

The government's stated aim was to "level the playing field" between property investors and first-home buyers. The thinking was that negative gearing gave investors a significant tax advantage that homeowners couldn't access, making it harder for ordinary Kiwis to compete in the property market.

What Properties Are Affected?

The ring-fencing rules apply to residential investment properties only. Your main family home is not affected—you've never been able to claim losses on your primary residence anyway.

Importantly, new builds are exempt from some of these rules, though the specifics depend on when the property was acquired and when loans were drawn down. This exemption was designed to encourage new housing construction, which the government saw as crucial for addressing housing shortages.

What This Means for Your Investment Strategy

Cash Flow Considerations

Without negative gearing deductions, your cash flow becomes more critical. You can't offset rental losses against your salary to reduce your tax bill, so you need to ensure your rental income covers your expenses—or have other funds to cover the shortfall.

This has made property investment less attractive for some investors, particularly those in the early years of ownership when mortgage interest is high relative to rental income. You'll need to carefully calculate your expected returns before purchasing an investment property.

Long-Term Rental Properties

If you're planning to hold a property long-term and expect it to become cash-flow positive eventually, ring-fencing is less of a concern. Your losses simply accumulate until your rental income exceeds your costs, at which point you can offset those accumulated losses.

Impact on the Rental Market

Removing negative gearing has reduced the incentive for private investors to purchase rental properties. This has constrained rental stock in some areas, potentially affecting renters through reduced availability and higher rents. The government has acknowledged this through increased funding for social and affordable housing initiatives.

Key Exemptions and Special Cases

Main Family Home

Your primary residence is completely unaffected by ring-fencing rules. You've always been unable to claim losses on your family home, so nothing changes for you as a homeowner.

New Build Properties

There's a transitional exemption for new builds, though this has specific criteria around when the property was acquired and when loans were drawn down. If you're investing in new construction, check with the IRD or a tax professional about your specific situation.

Other Investment Types

Ring-fencing applies specifically to residential rental properties. If you invest in commercial property, shares, or other assets, different rules may apply.

The Bright-Line Test: Another Tax Consideration

While negative gearing removal affects ongoing rental losses, you should also be aware of the Bright-Line Test—a separate rule that taxes capital gains on property sold within a certain timeframe.

Currently, the Bright-Line Test operates on a 2-year window. This means if you buy and sell a residential property within 2 years, you'll pay income tax on any profit. Properties held longer than 2 years are generally not subject to this tax (though there are exceptions if the IRD considers you to be in the business of trading properties).

This is an important consideration when planning your investment strategy, as it affects both short-term flipping strategies and your overall tax position.

Practical Tips for Property Investors Today

- Run the numbers carefully: Before purchasing an investment property, calculate whether your expected rental income will cover your mortgage interest, rates, maintenance, and other costs. Don't rely on negative gearing deductions to make the numbers work.

- Consider your cash position: Ensure you have sufficient reserves to cover shortfalls between rental income and expenses, especially in the early years of ownership.

- Track accumulated losses: Keep detailed records of any rental losses you incur. These can be offset against future rental income, so they're not entirely lost.

- Seek professional advice: Tax rules for property investors are complex. Consider consulting with an accountant or tax adviser familiar with New Zealand property investment to optimise your position.

- Understand the Bright-Line Test: If you're considering selling a property, be aware of the 2-year window. Holding properties beyond this period can significantly improve your after-tax returns.

- Explore KiwiSaver Home Withdrawal: If you're a first-home buyer, remember you can withdraw KiwiSaver funds for your primary residence. This might be a better investment vehicle than rental property investment in some circumstances.

Frequently Asked Questions

Can I still claim any deductions on my rental property?

Yes, you can claim legitimate business expenses such as rates, insurance, maintenance, property management fees, and depreciation on chattels (though not the building itself). What you can't do is offset these losses against your personal income. Losses are ring-fenced and can only be deducted from future rental income.

What happens to losses I accumulated before the rules changed?

If you had rental losses before the ring-fencing rules took effect, you can still offset these against your rental income going forward. However, you can't go back and claim deductions against your personal income for prior years.

Does this affect my KiwiSaver investment property?

KiwiSaver funds are generally invested in shares, bonds, and managed funds rather than direct property ownership. If you have a self-directed KiwiSaver scheme investing in property, the ring-fencing rules would apply. Seek advice from your KiwiSaver provider about your specific situation.

If I sell my rental property, can I use accumulated losses against the capital gain?

No. Ring-fenced losses cannot be applied to capital gains when you sell the property. They can only be offset against future rental income from other properties.

Are commercial property investments affected by ring-fencing?

Ring-fencing rules apply to residential rental properties. Commercial property investments have different tax treatment. If you're investing in commercial real estate, consult a tax professional about the rules that apply to you.

Should I still invest in rental property given these changes?

This depends on your individual circumstances, investment goals, and risk tolerance. Property can still be a good long-term investment if the rental income covers your costs and you expect capital growth. However, you need to ensure your cash flow works without relying on negative gearing deductions. Many investors now focus on properties that are positively geared (where rental income exceeds costs) or expect to become positively geared over time.

Moving Forward: What Investors Need to Know

The removal of negative gearing represents a significant shift in New Zealand's approach to property investment taxation. The policy was designed to improve housing affordability for first-home buyers by removing a tax advantage that investors previously enjoyed.

If you're considering property investment, the key is to ensure your investment makes financial sense without relying on negative gearing deductions. This means focusing on properties with strong rental yields, or properties you expect to become cash-flow positive over time.

For existing investors, understanding ring-fencing and tracking accumulated losses is essential for tax planning. The IRD has detailed information about property interest rules on their website, and it's worth consulting a tax professional to ensure you're optimising your position.

Property investment can still be a valuable part of a diversified investment portfolio, but it requires careful analysis and realistic expectations in the post-negative gearing era.

Related Articles

Working Multiple Jobs NZ: Tax and Legal Considerations

Juggling multiple jobs can boost your income, but it's crucial to understand the tax implications and legal requirements that come with working more than one role in Aotearoa. Whether you're a contrac...

Name Changes NZ: Legal Process and Costs

Considering a fresh start with a new name? Whether it's after marriage, divorce, or simply embracing a personal transformation, changing your name in New Zealand is straightforward but requires follow...

Holiday Home Tax Rules NZ: Private Use and Rental

Own a bach in Coromandel or a holiday home in Queenstown? You're not alone—many Kiwis cherish these escapes, but renting them out while enjoying personal use can trip you up on tax rules. Getting the...

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...