Split Mortgages NZ: Combining Fixed and Floating Rates

Imagine locking in peace of mind for most of your home loan while keeping the door open to savings if rates drop—that's the power of a split mortgage in New Zealand. For Kiwis navigating 2026's mortga...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Imagine locking in peace of mind for most of your home loan while keeping the door open to savings if rates drop—that's the power of a split mortgage in New Zealand. For Kiwis navigating 2026's mortgage market, combining fixed and floating rates offers a smart way to balance stability with flexibility, especially as economists predict moderate rate stability early in the year before potential upward pressure.

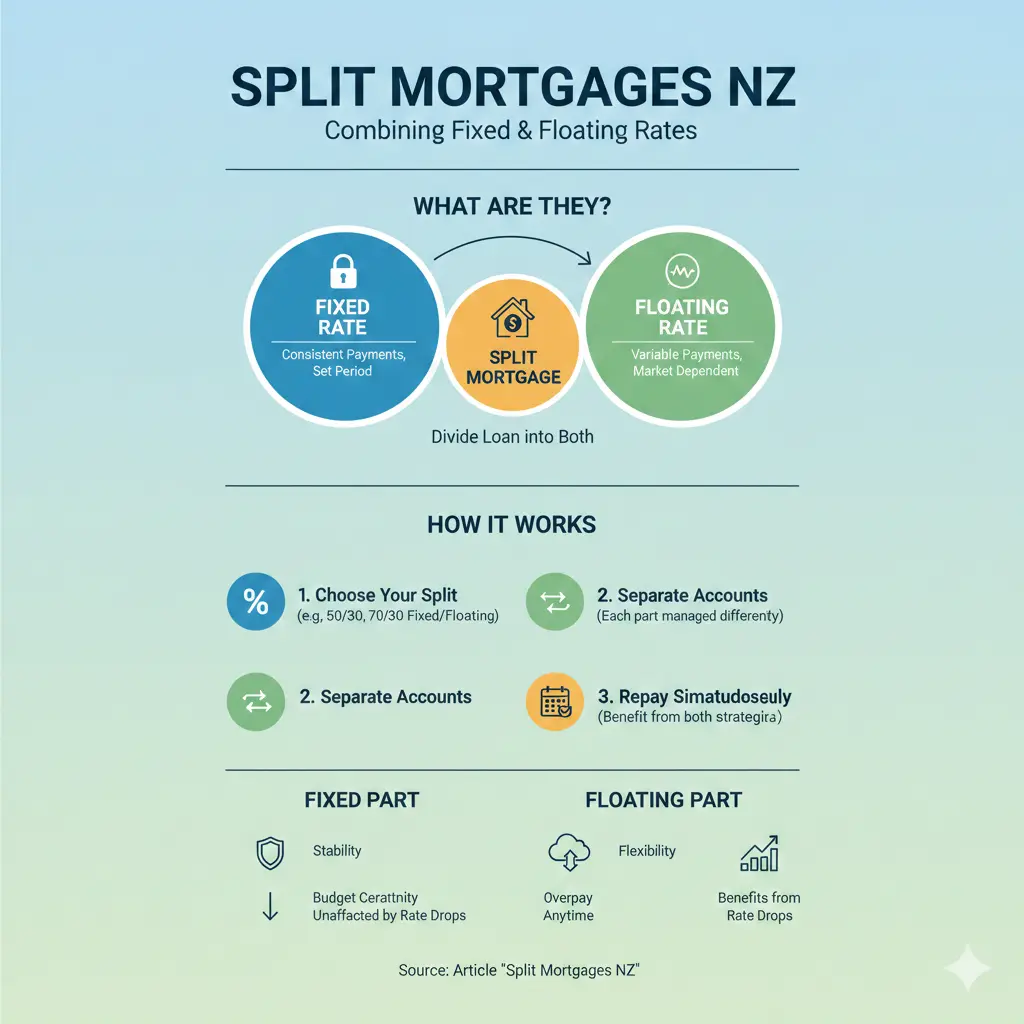

What Are Split Mortgages in NZ?

A **split mortgage** divides your total home loan into portions with different interest rate types, typically fixed and floating, allowing you to customise risk and repayments to your needs. This hybrid approach lets you, say, fix 60% of your $800,000 mortgage at a stable 5.5% for two years while leaving 40% ($320,000) on a floating rate around 6.2%, hedging against market shifts.

Unlike a fully fixed loan with predictable payments or a pure floating one that fluctuates with the Official Cash Rate (OCR), a split mortgage combines both worlds. The fixed portion shields you from rate hikes—crucial if the Reserve Bank tightens policy later in 2026—while the floating part lets you make extra repayments without penalties and benefit if rates fall.

In New Zealand, most major banks like Westpac, ANZ, and Kiwibank offer split options, often with fixed terms from six months to five years. This structure suits families budgeting on one income or investors juggling cash flow, providing certainty for essentials like school fees while allowing opportunistic paydowns.

How Split Mortgages Differ from Traditional Loans

- Full Fixed: Locked rate for stability, but break fees apply for early repayment.

- Full Floating: Flexible extras, but vulnerable to OCR changes—currently around 5.25% influencing floating rates.

- Split: Best of both; no prepayment costs on floating, fixed peace for the set term.

Pro tip: Use your bank's online calculator to model splits—Westpac's tool shows how a 70/30 fixed/floating split could save $5,000 over two years if rates drop 0.5%.

How Do Split Mortgages Work in Practice?

Setting up a split is straightforward: when refinancing or buying, tell your lender the percentages. For a $600,000 loan, you might allocate $360,000 (60%) fixed for three years at 5.4%, and $240,000 (40%) floating at 6.1%. Each portion runs independently—fixed payments stay put, floating adjusts quarterly with market rates.

Repayments are calculated separately but combined into one weekly or fortnightly payment for simplicity. If floating rates rise to 6.5%, only 40% of your loan feels it, keeping overall costs manageable. Many banks allow rebalancing annually without fees, so review post-OCR announcements.

Common Split Ratios for Kiwis

| Split Ratio | Best For | Example Scenario (2026 Rates) |

|---|---|---|

| 70% Fixed / 30% Floating | Risk-averse families | Stability for mortgage stress tests; flexibility for KiwiSaver boosts. |

| 50% Fixed / 50% Floating | Balanced cash flow | Even exposure; ideal if expecting rate cuts mid-year. |

| 30% Fixed / 70% Floating | Aggressive savers | Max extra repayments; suits high earners targeting pay-off by 2030. |

You can layer further—split into multiple fixed terms (e.g., 20% one-year, 40% three-year) plus floating—for a 'laddered' strategy reducing refix shock in 2026, when one-year rates may edge up.

Benefits of Combining Fixed and Floating Rates

Split mortgages shine in NZ's volatile market, mitigating risks while unlocking opportunities. Key wins include:

- Rate Rise Protection: Fixed portion caps exposure—if OCR climbs 0.75% in late 2026, only your floating slice rises, potentially saving $200-600 monthly vs full floating.

- Flexibility for Extras: Pay lump sums on floating without fees—perfect for bonuses or inheritance—while fixed ensures budgeting.

- Lower Refix Stress: Staggered maturities mean not all your loan refixes at once, avoiding payment jumps.

- Custom Savings: If rates fall (as some predict early 2026), floating drops faster than fixed specials.

For a Kiwi couple on $150,000 combined income, a 60/40 split could stabilise payments at $3,200 fortnightly, versus $3,500+ if fully floating during hikes.

Real Kiwi Example

"We split 65% fixed for security with kids' school costs, 35% floating to smash extras—saved $15k in two years when rates dipped." – Auckland homeowner, via adviser feedback.

Potential Drawbacks and Risks

No strategy is perfect. Fixed portions limit extras (fees up to 3% for breaks), and if rates plummet, you're stuck higher. Floating exposes you to hikes—though splits minimise this. Also, low equity (under 20% deposit) may trigger margins from lenders.

In 2026, with inflation lingering, longer fixes (3-5 years) cost more upfront but protect against refix shocks. Always check LVR restrictions via the Reserve Bank.

Is a Split Mortgage Right for You in 2026?

Consider your horizon: families or near-retirees favour 70%+ fixed; young professionals or investors lean floating-heavy. If refixing soon, split to avoid full exposure—advisers push this amid stable-but-iffy forecasts.

Run numbers: for $500k loan at 5.8% average, 50/50 split yields $2,800 fortnightly vs $2,950 full floating if rates +0.5%. Factor ACC levies, council rates, and KiwiSaver contributions too.

Actionable Steps to Set Up

- Assess Finances: Use MoneyHub's comparator for rates.

- Model Splits: Bank calculators or advisers simulate 2026 scenarios.

- Shop Around: Compare Westpac, ASB—negotiate 0.1-0.3% off.

- Get Advice: Free from mortgage brokers; check registered via NZMBA.

- Review Annually: Rebalance post-RBNZ meetings.

Disclaimer: This isn't personalised financial advice. Consult a licensed adviser or your bank for your situation, considering IRD tax implications for investors.

Next Steps for Your Mortgage

Don't leave refixing to chance in 2026—grab your latest statements, hit up a broker via NZMBA, and model splits today. Pair with a budget review incorporating WINZ supports if needed. Secure your slice of stability now, and you'll sleep better knowing you've hedged smartly.

Frequently Asked Questions

Sources & References

-

1

Split Home Loans – Achieving Flexible Rates in NZ — mortgagemanagers.co.nz

-

2

Split home loan — Westpac NZ — www.westpac.co.nz

- 3

-

4

Fixed vs Floating Mortgage: What's Better in NZ This Year? — Look Ahead — www.lookahead.co.nz

-

5

Compare Mortgage Options and Types — MoneyHub — www.moneyhub.co.nz

-

6

Why Now Could Be the Time to Reconsider Fixing Your Mortgage Rate — Eureka Financial — www.eurekafinancial.co.nz

-

7

Refixing in 2026: A Decision Framework — New Zealand Mortgages — www.newzealandmortgages.co.nz

-

8

Mortgage Refix Shock NZ 2026 — Artbeat — www.artbeat.org.nz

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...