Tax Planning for Freelancers and Contractors NZ

As a freelancer or contractor in New Zealand, you're your own boss, but that freedom comes with the responsibility of managing your taxes effectively. Smart tax planning for freelancers and contractor...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

As a freelancer or contractor in New Zealand, you're your own boss, but that freedom comes with the responsibility of managing your taxes effectively. Smart tax planning for freelancers and contractors NZ can save you thousands, help you avoid IRD penalties, and keep more cash in your pocket for the things that matter.

Whether you're a graphic designer juggling gigs in Auckland, a consultant based in Wellington, or a tradie working across the South Island, understanding the 2026 tax rules is crucial. With updated income tax brackets, new deductions like the 20% Investment Boost, and opportunities like the early payment discount, there's plenty to leverage this year. This guide breaks it down into practical steps tailored for Kiwis, so you can optimise your tax position without the headache.

Understanding Your Tax Obligations as a Freelancer or Contractor

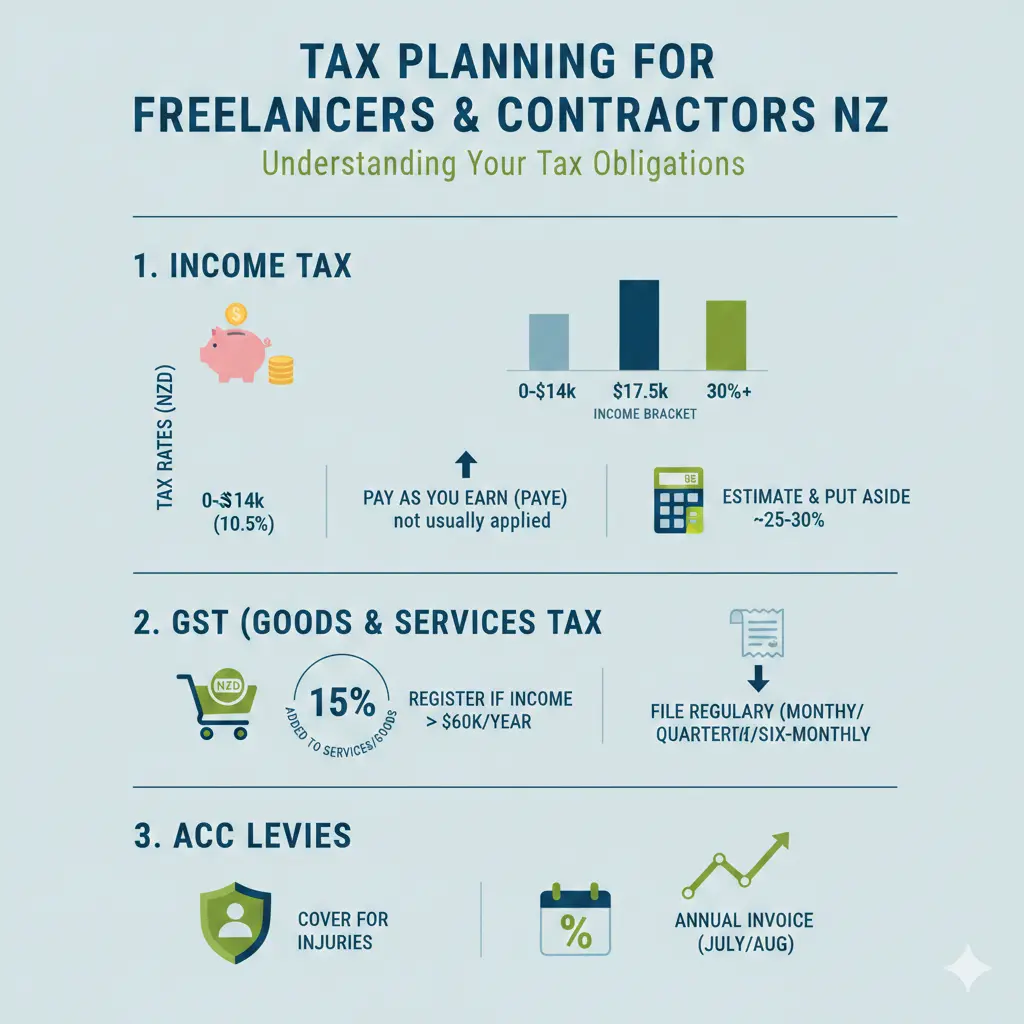

In New Zealand, freelancers and contractors typically operate as sole traders, meaning your business income is taxed at personal income tax rates. You'll file an IR3 return at the end of your financial year (usually 31 March), reporting your net profit after deducting allowable expenses.

2026 Income Tax Rates

For the 2025/26 tax year (1 April 2025 to 31 March 2026), the rates are:

| Income Range | Tax Rate |

|---|---|

| $0 – $15,600 | 10.5% |

| $15,601 – $53,500 | 17.5% |

| $53,501 – $78,100 | 30% |

| $78,101 – $180,000 | 33% |

| Over $180,000 | 39% |

These rates apply to your taxable income after deductions. Use IRD's online tax calculator to estimate your liability.

Provisional Tax and When It Kicks In

If your residual income tax (RIT) exceeds $5,000, you'll enter the provisional tax system. This means paying tax in instalments throughout the year—standard, ratio, or estimation methods are available. New freelancers often start with standard provisional tax based on prior years, but if you're truly new to self-employment, you might avoid it initially.

- Threshold: RIT over $5,000 triggers provisional tax.

- GST Registration: Mandatory if turnover exceeds $60,000 annually. Charge 15% GST on invoices, file returns every 1, 2, or 6 months depending on turnover (under $500,000 usually 6-monthly).

- ACC Levies: Cover Earner's Levy, Work Levy (industry-rated), and Working Safer Levy. Expect your first invoice post-year-end.

Student Loans and Other Deductions from Income

If you have a StudyLink debt, repayments start once earnings exceed $24,128 for 2026 (adjusted net income). For example, on $40,000 adjusted net income, you'd owe around $1,905 annually (12% on amount over threshold). Pay voluntarily throughout the year to manage cash flow, or settle with your year-end tax.

Don't forget KiwiSaver contributions (voluntary for self-employed) or the Independent Earner Tax Credit (IETC) if eligible—up to $10 weekly for incomes $24,000-$66,000, but it phases out with KiwiSaver.

Maximising Deductions: What You Can Claim in 2026

Deductions lower your taxable income, so track everything. IRD allows claims for expenses wholly and exclusively for business.

Everyday Business Expenses

- Home Office: Portion of rent, power, internet, and rates based on space used (e.g., 15% of floor area).

- Vehicle Costs: Logbook method (track business km) or kilometre rate (83 cents/km for 2026, confirm with IRD).

- Marketing & Subscriptions: Ads, website hosting, software like Xero.

- Travel & Meals: Client meetings, but keep receipts and logs.

- Professional Fees: Accountant, lawyer, insurance.

New for 2026: 20% Investment Boost

From 22 May 2025, claim a one-off 20% deduction on new assets, accelerating depreciation for your 2026 return. Choose between this, the $1,000 immediate write-off, or standard depreciation—expert advice helps pick the best.

Prepayments to Front-Load Deductions

Buy equipment or prepay expenses before 31 March:

- Insurance: Up to $12,000 (12 months).

- Rent: Up to $26,000 (6 months).

Pro tip: Time purchases to align with cash flow and deduction limits.

Early Payment Discount: A Must-Know for New Freelancers

If you're in your first year of self-employment (sole trader, partnership, or look-through company) with no provisional tax obligation in the last 4 years (FY22-FY26), grab the 6.30% early payment discount for FY26.

How it works:

- Make voluntary payments or use tax pooling before 31 March 2026.

- Apply when filing your IR3 by 31 March 2027.

- Discount applies to the lesser of your tax liability or payments made.

Example: $180,000 taxable income = ~$49,300 tax. Prepay by deadline, save $3,100 (6.3%). Tax pooling extends to 18 June 2027 with low interest.

"For the 2026 income year (FY26), this discount is 6.30%, which can meaningfully reduce your tax burden if you plan your cashflow well."

Provisional Tax Strategies for Ongoing Contractors

Once provisional tax applies, choose your method:

- Standard: Based on prior year.

- Ratio: 105% of current GST.

- Estimation: Forecast your income—best for variable gigs.

Pay in instalments (e.g., 28 August, 15 November, etc., for 31 March balance). Use tax pooling to smooth payments and avoid UOMI penalties.

Cash Flow and Record-Keeping Tips

Poor financial management stresses 67% of Kiwi small businesses. Use Xero or MYOB for automated tracking, invoice promptly, and set aside 30% of income for tax/ACC/GST.

- Separate business bank account.

- Weekly reconciliation.

- Accountant review quarterly.

- Budget for levies: ACC first invoice hits post-year.

Common Pitfalls and How to Avoid Them

- Missing GST Threshold: Register early if approaching $60k.

- Inadequate Records: No receipts = no deduction.

- Late Payments: UOMI and penalties add up.

- Overlooking Discounts: Check early payment eligibility yearly.

Next Steps for Smarter Tax Planning

Start by reviewing your 2025 numbers to forecast 2026. Grab free IRD tools, set up accounting software, and book a chat with an accountant via bookkeepers.org.nz or your local network. Prepay where possible, claim every deduction, and apply for discounts—your future self (and wallet) will thank you. Head to ird.govt.nz for personalised calculators and guides tailored to freelancers.

Frequently Asked Questions

Sources & References

- 1

-

2

Maximise your 2026 tax return with the right small business deductions — www.prospa.co.nz

-

3

Tax basics for sole traders — www.business.govt.nz

-

4

Self-Employment - The Complete New Zealand Guide — www.moneyhub.co.nz

- 5

Related Articles

The "No-Spend" Month: How One Kiwi Saved $2;000 in 30 Days

Imagine looking at your bank account at the end of the month and seeing an extra $2,000 staring back at you—all because you said "no" to impulse buys, takeaways, and those sneaky coffee runs. That's e...

How to Calculate Your Take-Home Pay with the NZ Salary Calculator

Ever wondered why your bank account doesn't match that shiny new job offer? You're not alone—many Kiwis scratch their heads over the gap between gross salary and actual take-home pay. With New Zealand...

Budgeting for Beginners: The "50/30/20 Rule" Adjusted for NZ Salaries

Struggling to make your Kiwi paycheck stretch further? You're not alone—many of us feel the pinch from rising rents, grocery bills, and that tempting flat white habit. But what if a simple rule could...

How to Travel the World on a NZ Salary

Ever dreamed of sipping cocktails on a Thai beach or exploring the ancient ruins of Machu Picchu, all while earning a solid Kiwi wage? With New Zealand's average monthly salary hitting 5,666 NZD in 20...