The 50/30/20 Budget Rule: Does It Work in NZ?

Ever feel like your paycheque vanishes before you can say "KiwiSaver"? You're not alone. With rising living costs in New Zealand, from Auckland's sky-high rents to grocery bills that keep climbing, ma...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Ever feel like your paycheque vanishes before you can say "KiwiSaver"? You're not alone. With rising living costs in New Zealand, from Auckland's sky-high rents to grocery bills that keep climbing, many Kiwis are searching for a simple way to take control of their finances. Enter the 50/30/20 budget rule – a straightforward method that's gained traction worldwide. But does it work in NZ? In this guide, we'll break it down, test it against real Kiwi realities, and show you how to make it fit your life in 2026.

What Is the 50/30/20 Budget Rule?

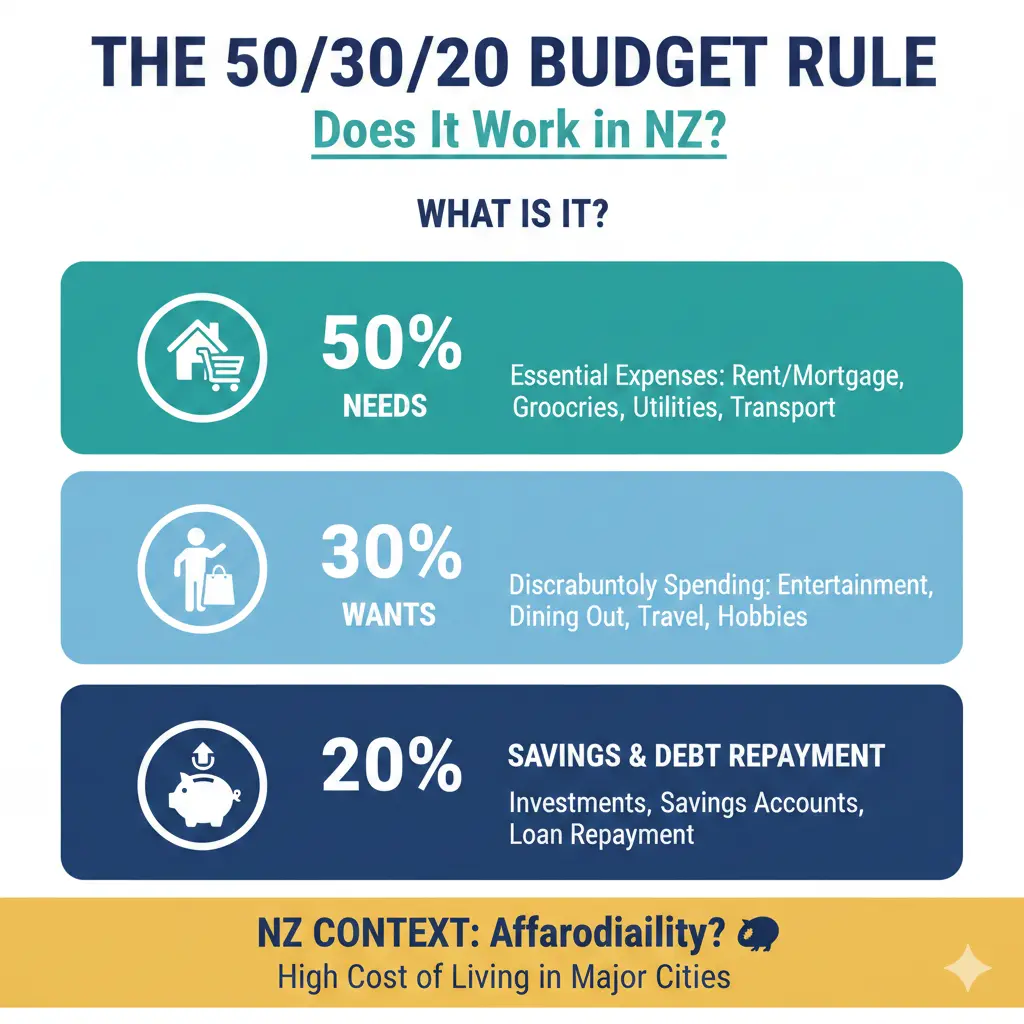

The 50/30/20 rule is a popular budgeting framework that divides your after-tax income into three buckets: 50% for needs, 30% for wants, and 20% for savings and debt repayment. Popularised by US Senator Elizabeth Warren in her book All Your Worth, it's designed to balance essentials, enjoyment, and future security without complex spreadsheets.

It's not a rigid law but a flexible guideline. As MoneyHub notes, it's more of a goal than an absolute rule, helping you build savings habits even if you start smaller, like 10% to savings. In NZ, where median household incomes hover around $120,000 gross (translating to roughly $85,000-$90,000 after tax for many), this rule offers a starting point amid our unique costs like high housing and utilities.

Breaking Down the Categories

- 50% Needs: Non-negotiable essentials for survival – think rent or mortgage, groceries, power bills, transport, insurance, and minimum debt payments.

- 30% Wants: Fun stuff that makes life enjoyable, like dining out, holidays, gym memberships, or All Blacks tickets.

- 20% Savings & Debt: Building your future – KiwiSaver contributions, emergency funds, extra debt repayments, or investments.

How the 50/30/20 Rule Works in Practice

To apply it, start with your take-home pay (after tax, ACC, KiwiSaver, and student loans). Track spending for a month using apps like PocketSmith or the free MoneyHub 50/30/20 calculator. Then allocate:

Step-by-Step Guide for Kiwis

- Calculate Net Income: Use the IRD's tax calculator for accuracy. For a $70,000 salary in 2026, expect around $4,500 monthly after tax.

- Track Expenses: Categorise last month's bank statements. Tools like Xero or Excel work well.

- Allocate Buckets: For $4,500 net: $2,250 needs, $1,350 wants, $900 savings.

- Adjust and Review: Monthly check-ins keep you on track.

Here's a Kiwi example for a single Auckland renter earning $75,000 gross ($4,800 net monthly):

| Category | % | Amount | NZ Examples |

|---|---|---|---|

| Needs | 50% | $2,400 | Rent $1,800, groceries $400, power $150, bus pass $50 |

| Wants | 30% | $1,440 | Coffee runs $200, Netflix/gym $100, weekend brunch $300, clothes $200 |

| Savings/Debt | 20% | $960 | KiwiSaver $300, emergency fund $400, credit card payoff $260 |

This setup prevents debt while enjoying life.

Does the 50/30/20 Budget Rule Work in New Zealand?

Short answer: Yes, but with tweaks. NZ's high cost of living – especially housing at 40-50% of income in cities – often pushes needs over 50%. Lifetimes NZ suggests adjusting to 70/20/10 in pricey spots like Auckland. Bricks and Mortgages calls it one of the most effective rules for Kiwis, balancing essentials like insurance and utilities with savings.

In regional areas like Christchurch or Dunedin, it fits better, with lower rents allowing more for wants and savings. Nectar Money recommends it as a straightforward NZ budgeting method. Recent Budget 2025 changes boost its viability: KiwiSaver defaults rise to 3.5% from April 2026 (then 4% in 2028), adding to your 20% savings bucket without extra effort.

Real Kiwi Challenges and Success Stories

Auckland rents average $600/week ($2,600/month) for a one-bedder, eating 55% of a $4,700 net income alone. Solution? Share housing or relocate. Meanwhile, a Wellington family on $100,000 household income used 50/30/20 to clear $15,000 debt in 18 months, per MoneyHub users.

Pros:

- Simple for beginners – no need for zero-based budgeting.

- Promotes KiwiSaver and emergency funds (aim for 3-6 months' expenses).

- Flexible for irregular incomes like gig work; average your last three months.

Cons:

- High needs in NZ (housing, petrol at $2.80/L).

- Inflation at 2-3% in 2026 squeezes wants.

- Not ideal for low-income households on benefits; prioritise WINZ allowances first.

NZ-Specific Adjustments for 2026

Tailor the rule to our landscape:

Incorporate KiwiSaver and Government Changes

From April 2026, default KiwiSaver jumps to 3.5% (matched by employers), halving government contributions to 25c/dollar (max $260.72). Slot this into your 20%: e.g., 8% total KiwiSaver ($360 on $4,500 net) leaves room for extra savings. High earners over $180,000 lose the govvie top-up, so ramp up personal contributions.

Handle High Housing Costs

If needs hit 60%, cut wants to 20% and savings to 20% (60/20/20). Use KiwiBuild or Kainga Ora for affordable options, or check Trade Me Rentals for flats under $500/week outside Auckland.

Factor in Local Expenses

- Groceries: $150/person weekly at Countdown; shop PAK'nSAVE for savings.

- Transport: AT HOP card or fuel; WOF/regs add $300/year.

- Insurance: House/contents via AMI, health via Southern Cross.

- Debt: Student loans auto-deduct; pay extra in 20% bucket.

For families, blend with Working for Families – Budget 2025 tweaks thresholds for 142,000 families, adding $14/fortnight.

Tools and Tips to Make It Stick

Success comes from tracking. Try:

- Apps: MoneyHub's 50/30/20 calculator, PocketSmith (NZ-based), or YNAB.

- Spreadsheets: Free templates from MoneyHub or Google Sheets.

- Bank Tools: ASB or BNZ budgeting features auto-categorise.

Practical Tips:

- Automate: Set direct debits for savings first.

- Review quarterly, especially post-Budget changes.

- Side hustle: Uber or Trade Me sales boost your 20%.

- Emergency fund: 3 months' needs in a notice saver at 4-5% interest.

Next Steps: Get Started Today

Grab your latest payslip, download MoneyHub's calculator, and map your first 50/30/20 budget. Adjust for NZ realities like KiwiSaver hikes and housing, and you'll build financial freedom. Small changes compound – that 20% could mean a $50,000 KiwiSaver boost by 65. Track for 30 days, tweak as needed, and share your wins in the comments. You've got this, Kiwis!

Frequently Asked Questions

Sources & References

-

1

Budget 2025 At a Glance — treasury.govt.nz — www.treasury.govt.nz

-

2

Financial Goals: How to Plan for 2025-2026 | Lifetimes NZ — lifetimes.co.nz

-

3

50/30/20 Budget Calculator — moneyhub.co.nz — www.moneyhub.co.nz

-

4

What is the 50/30/20 Budget Rule? — thesheetcode.com — thesheetcode.com

-

5

The 50/30/20 Rule: A Smart Way to Budget — rbl.bank.in — www.rbl.bank.in

-

6

7 Essential Rules for Saving Money — bricksandmortgages.co.nz — bricksandmortgages.co.nz

-

7

4 Steps on How to Budget in NZ — nectar.co.nz — nectar.co.nz

-

8

10 Things to Do Differently with Money — moneyhub.co.nz — www.moneyhub.co.nz

Related Articles

The "No-Spend" Month: How One Kiwi Saved $2;000 in 30 Days

Imagine looking at your bank account at the end of the month and seeing an extra $2,000 staring back at you—all because you said "no" to impulse buys, takeaways, and those sneaky coffee runs. That's e...

How to Calculate Your Take-Home Pay with the NZ Salary Calculator

Ever wondered why your bank account doesn't match that shiny new job offer? You're not alone—many Kiwis scratch their heads over the gap between gross salary and actual take-home pay. With New Zealand...

Budgeting for Beginners: The "50/30/20 Rule" Adjusted for NZ Salaries

Struggling to make your Kiwi paycheck stretch further? You're not alone—many of us feel the pinch from rising rents, grocery bills, and that tempting flat white habit. But what if a simple rule could...

How to Travel the World on a NZ Salary

Ever dreamed of sipping cocktails on a Thai beach or exploring the ancient ruins of Machu Picchu, all while earning a solid Kiwi wage? With New Zealand's average monthly salary hitting 5,666 NZD in 20...