Buying at Auction NZ: Complete Guide for First-Timers

Buying a property at auction in New Zealand can feel daunting, especially if you're a first-timer. But with the right preparation and understanding of how our unique auction system works, you'll be in...

James writes about the New Zealand property market, renting, home ownership, and housing costs. He breaks down complex property topics into practical advice for renters and buyers.

Buying a property at auction in New Zealand can feel daunting, especially if you're a first-timer. But with the right preparation and understanding of how our unique auction system works, you'll be in a much stronger position to make a confident offer and secure your dream home. Whether you're in Auckland, Wellington, Christchurch, or anywhere else across Aotearoa, this guide will walk you through everything you need to know.

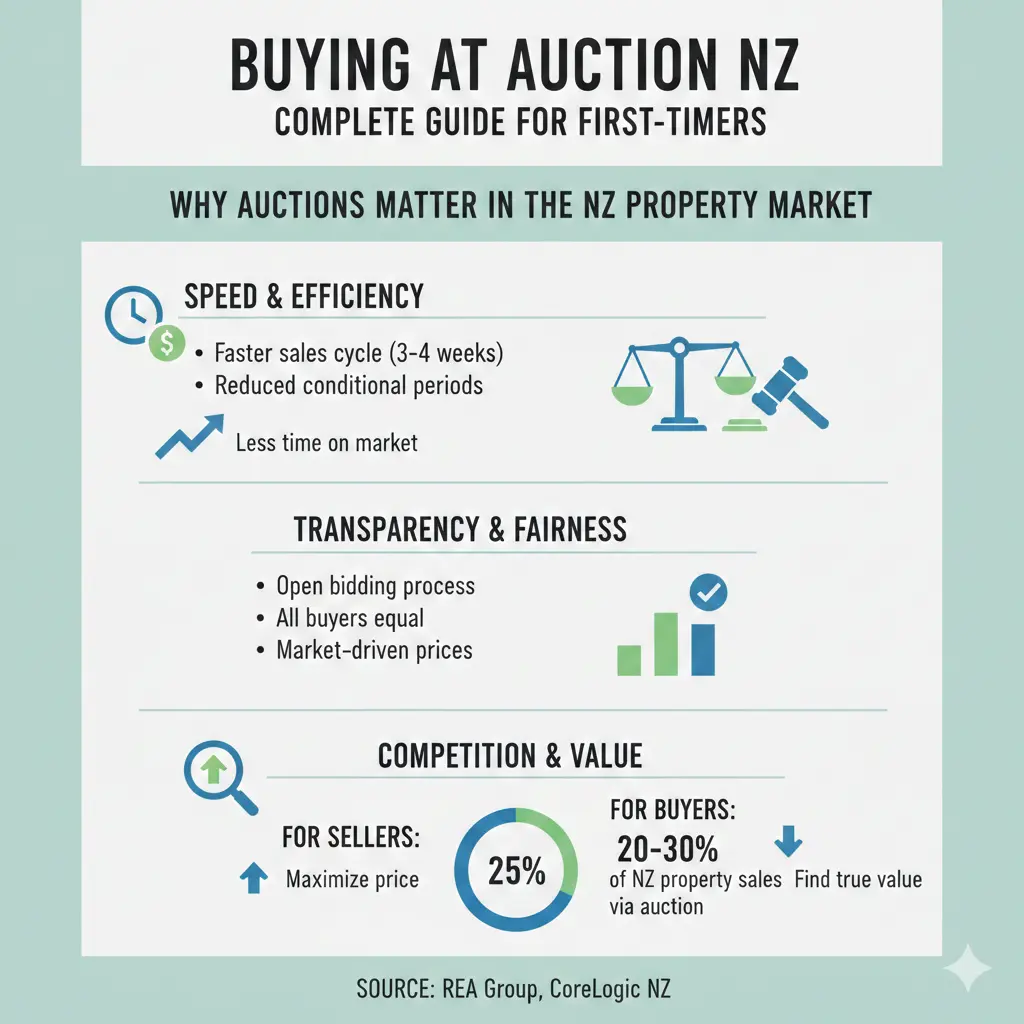

Why Auctions Matter in the New Zealand Property Market

Auctions remain one of the most popular ways to buy and sell property in New Zealand. They're fast, competitive, and transparent—qualities that appeal to both buyers and sellers. The market moves quickly, and understanding the auction process gives you a real advantage, especially in competitive markets where multiple buyers are interested in the same property.

The 2026 property market has shown some interesting momentum early in the year, making it an active time for auctions across the country. If you're thinking about buying, now's a good time to understand the process thoroughly.

Understanding the Key Steps Before Auction Day

Get Pre-Approved for Finance

This is absolutely essential if you're planning to bid at auction. Pre-approval means your bank or lender has confirmed you can borrow the amount you need. Without it, you're not ready to bid—full stop. The auction process moves fast, and you'll need to pay your deposit immediately if you win, so having your finances locked in beforehand is non-negotiable.

Check Your Eligibility with the Overseas Investment Office (OIO)

If you're a foreign buyer, you'll need to confirm your eligibility with the Overseas Investment Office before you sign anything. This is critical: signing a contract when you're ineligible can lead to massive fines. Don't skip this step. Check the OIO rules early in your property search so you know whether you can legally purchase.

Research the Property Thoroughly

Before auction day, you'll want to gather as much information as possible about the property. Here's what you should do:

- Conduct a title search to understand the property's legal history

- Request a Land Information Memorandum (LIM) from your local council—this reveals zoning, flood risks, and any unconsented building works

- Get a professional property inspection report

- Inspect the house, land, and surrounding neighbourhood yourself

- Understand the neighbourhood and local amenities

The LIM report is particularly important. It's a public document that tells you everything the council knows about the property, including whether it's in a flood zone or has any building consent issues. Always request one—it's a small investment that could save you thousands.

Determine the Property's Value

You need to have a realistic idea of what the property is worth before you step into the auction room. Use recent comparable sales in the area, online property valuations, and feedback from your real estate agent to set a maximum bid price. Stick to it—auction fever is real, and it's easy to get caught up in the moment and overpay.

Understanding Different Sale Methods in New Zealand

Not all properties are sold the same way. Understanding the different methods helps you prepare your offer strategy:

- Auction: Fast and competitive. You bid unconditionally, and if you win, you pay your deposit immediately (usually 10%).

- Deadline Sale / Tender: You submit a confidential written offer by a specific deadline.

- Negotiation: The traditional offer and counter-offer process.

- Asking Price: The seller lists a price, but negotiation is often possible.

Many properties listed for auction can also be sold prior to auction day if a strong offer comes in. Look for the words "unless sold prior" on the listing—this means the seller is open to selling beforehand if the right offer arrives.

The Auction Process: What to Expect on the Day

Registration and Preparation

Arrive early on auction day. You'll need to register your interest, and the agent will give you a bidders number. If you're bidding online via video conferencing, registration happens online, but make sure you test your internet connection beforehand and watch another auction first to understand how it works.

Auctions are usually held at the property itself or at the real estate agent's office. Get the exact location and time from the agent well in advance.

Understanding the Reserve Price

Before bidding starts, the seller sets a reserve price—the minimum amount they're willing to accept. You won't know what this is, but it's important to understand how it works. Bidding usually starts below the reserve price, and anyone can make the first bid. The auctioneer will make it clear which bids are vendor bids (bids from the seller to encourage bidding towards the reserve).

How Bidding Works

Once the auctioneer reads out the terms and conditions, bidding begins. Here's how it works:

- Each bid must be higher than the one before

- The auctioneer decides the minimum bid increment

- You can bid by raising your hand or your bidders number clearly

- If you're bidding by phone, the agent will inform you about bids and let you know when to bid

- For online bidding, there may be a slight delay on your screen—refresh it to see the latest bids

Once the reserve is met, vendor bids are no longer allowed, and the highest bid wins.

What Happens If You Win

If your bid is the highest when the gavel comes down, you've won the auction. You'll immediately be asked to sign the sale and purchase agreement and pay your deposit. This is why having your finances ready beforehand is so crucial—you won't have time to arrange funds later.

If the Reserve Isn't Met

If bidding doesn't reach the reserve price, the seller has options. They may:

- Lower the reserve price and continue the auction

- Negotiate privately with the highest bidder

- Choose not to sell the property

If you're the highest bidder below the reserve, the auctioneer may take you aside for negotiations. If the seller accepts your bid, it becomes the new reserve price, and the auction continues. However, you haven't officially won until the auctioneer accepts your bid as the final selling price.

Key Differences: Auction vs. Other Sale Methods

Understanding how auctions differ from other methods will help you prepare your strategy:

| Aspect | Auction | Negotiation | Tender |

|---|---|---|---|

| Speed | Fast—usually within a week | Variable—can take weeks | Fixed deadline, quick decision |

| Conditions | Bidding is unconditional | You can include conditions | Usually unconditional |

| Finance Ready | Must be pre-approved | Can arrange after offer | Usually pre-approved needed |

| Flexibility | Limited—you pay deposit immediately | More flexible negotiation | No negotiation after tender closes |

Important Things to Remember About Auction Conditions

When you bid at auction, you're agreeing to buy the property unconditionally. This means:

- You cannot include conditions like "subject to finance" or "subject to inspection"

- Any conditions you and the seller agreed to before the auction must be met within agreed timeframes

- You need to know exactly what conditions apply before you bid

This is why doing your homework beforehand—inspections, LIM reports, valuations—is so important. You won't have the luxury of making your purchase conditional on these things on auction day.

Settlement: What Happens After You Win

Once you've won the auction and signed the agreement, settlement happens on an agreed date. On settlement day, your lawyer and the seller's lawyer swap funds for keys. Make sure you understand the settlement date when you bid—it's usually specified in the auction terms.

Your Next Steps to Auction Success

Buying at auction in New Zealand doesn't have to be intimidating. Here's your action plan:

- Get pre-approved for finance with your bank or lender

- Check OIO eligibility if you're a foreign buyer

- Find a property you're interested in and get all the information (LIM, inspection, valuation)

- Hire a lawyer or conveyancer to review the legal documents

- Set your maximum bid price and stick to it on the day

- Register for the auction and arrive early

- Bid confidently knowing you've done your preparation

The key to successful auction buying is preparation. Know the property, know your budget, have your finances sorted, and understand the process. When you walk into that auction room (or log in online), you'll be ready to make a smart, informed decision. Good luck with your property search!

Frequently Asked Questions

Sources & References

-

1

Buying property in New Zealand in 2026 — www.smartcurrencyexchange.com

-

2

How to buy a home at auction in New Zealand — www.wisemove.co.nz

-

3

Auction, Tender, Negotiation or Asking Price? A Simple Guide for Kiwi Home Buyers — www.themortgagehub.co.nz

-

4

Selling at auction in NZ: what you need to know — www.trademe.co.nz

-

5

WATCH: Perspectives Property Report February 2026 — www.nzsothebysrealty.com

Useful Tools

Related Articles

First Home Grant NZ: How to Get Up to $10000

Buying your first home is one of the biggest financial decisions you'll make, and the New Zealand government wants to help. The First Home Grant puts up to $10,000 directly towards your deposit, makin...

Why 2026 is the Hardest Year to Buy a Home (and How to Beat the Odds)

Imagine standing at the edge of the property ladder in 2026, eyeing your dream home while prices hover stubbornly high, listings pile up, and buyer confidence wavers. For Kiwis, this year feels toughe...

Buying Your First Home in 2026: A Step-by-Step NZ Checklist

Imagine standing in your own Kiwi bach or cosy family home, keys in hand, after years of renting. In 2026, with interest rates stabilising and first-home schemes still strong, buying your first home i...

Selling Your Home? 10 Low-Cost Renovations That Add $50k in Value

If you're planning to sell your home in New Zealand, you don't need to break the bank with a complete renovation to attract buyers and boost your sale price. The good news? Some of the most effective...