First Home Loan: How to Buy with Just 5% Deposit

Imagine standing in your own Kiwi home, keys in hand, without needing to save for years on end. For many first-home buyers in New Zealand, that's no longer a distant dream—thanks to the First Home Loa...

James writes about the New Zealand property market, renting, home ownership, and housing costs. He breaks down complex property topics into practical advice for renters and buyers.

Imagine standing in your own Kiwi home, keys in hand, without needing to save for years on end. For many first-home buyers in New Zealand, that's no longer a distant dream—thanks to the First Home Loan scheme, you can step onto the property ladder with just a 5% deposit.

With house prices still high but interest rates stabilising in 2026, this government-backed option underwritten by Kāinga Ora makes homeownership achievable sooner. Whether you're renting in Auckland or eyeing a regional gem, we'll walk you through everything you need to know: eligibility, how to apply, costs involved, and tips to boost your chances. Let's get you ready to make that first offer.

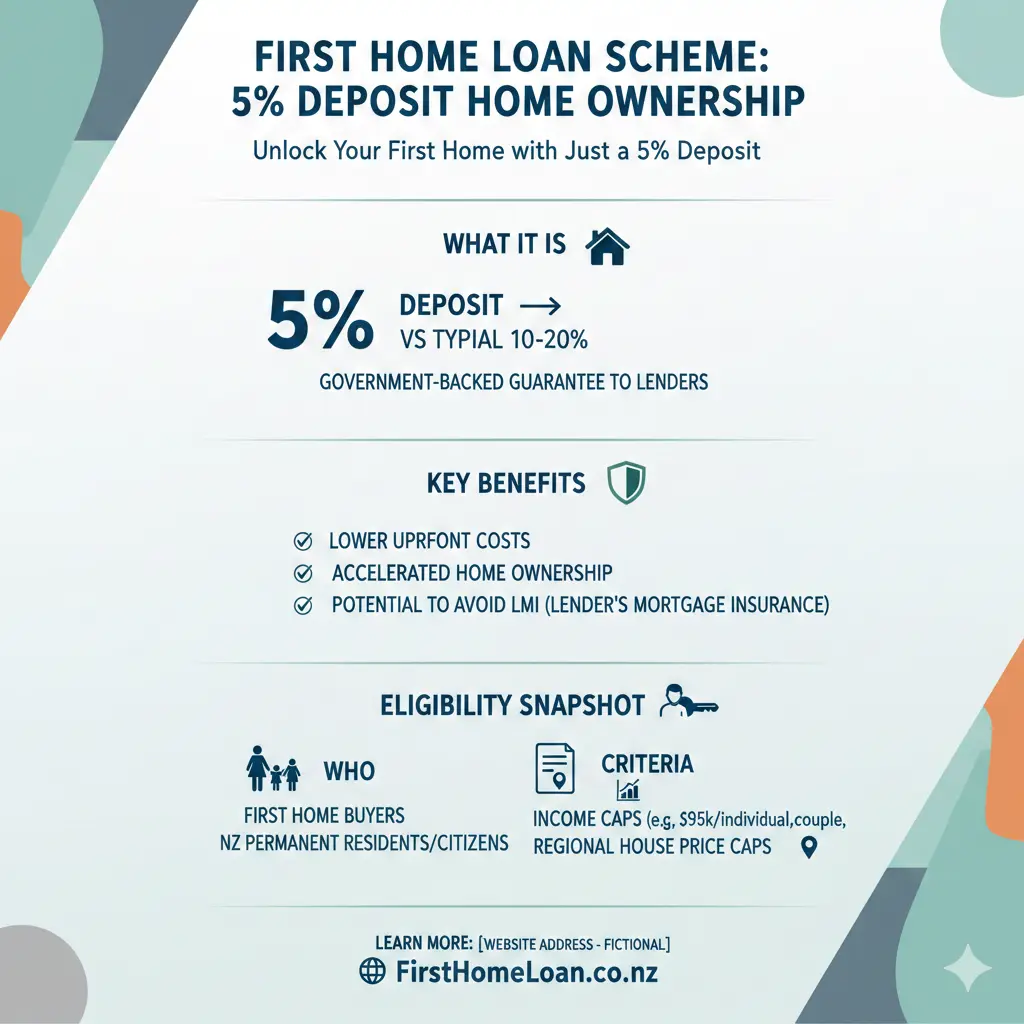

What is the First Home Loan Scheme?

The First Home Loan (previously known as the Welcome Home Loan) lets eligible Kiwis buy their first home with a minimum 5% deposit, bypassing the standard 20% lenders usually demand. Issued by participating banks and underwritten by Kāinga Ora, it allows loans up to 95% of the property's value (Loan-to-Value Ratio or LVR of 95%).

This scheme sits outside normal bank lending rules, introduced post-2008 financial crisis to protect borrowers and lenders. In 2026, it's especially timely as more first-home buyers secure approvals with low deposits amid a 'Goldilocks' market—stable rates and easing LVR perceptions.

How It Differs from Standard Mortgages

Normally, banks require a 20% deposit due to Reserve Bank LVR restrictions, meaning for a $900,000 average home, you'd need $180,000 saved—tough on a $52,500 median income. With First Home Loan:

- You need just 5% ($45,000 on a $900,000 home).

- Banks can lend the rest because Kāinga Ora guarantees part of the risk.

- No bank offers below 5% without this scheme or a family guarantee.

| Property Value | 5% Deposit (First Home Loan) | 20% Deposit (Standard) |

|---|---|---|

| $500,000 | $25,000 | $100,000 |

| $900,000 | $45,000 | $180,000 |

This table shows the deposit savings—crucial for speeding up your purchase.

Who Qualifies for a First Home Loan in 2026?

Not everyone can access this scheme; you must meet strict criteria from Kāinga Ora and your chosen lender. Here's the breakdown:

Key Eligibility Requirements

- First-time buyer: You (and any co-applicants) must not own another property or land in NZ (Māori land excepted).

- 5% deposit: At least 5% of purchase price from savings, KiwiSaver withdrawal, First Home Grant (if available), or gifts. No maximum deposit.

- Primary residence: The home must be your main home—no investment properties.

- Income and affordability: Household income under $130,000 for one/two buyers, or $150,000+ with kids (check current caps on Kāinga Ora site). Lenders assess debt-to-income (DTI) ratios.

- Property caps: Value under $1.2 million in Auckland/Wellington/Tasman, $900,000 elsewhere (2026 limits—confirm latest).

- Credit and age: Over 18, good credit history, stable job. Lenders check affordability rigorously.

If you exceed income caps, consider low-deposit options like 10-15% from banks, but rates may be higher.

Using KiwiSaver and Gifts

Boost your deposit with KiwiSaver first-home withdrawal (up to your balance plus $10,000 government contribution if eligible). Family gifts count fully towards the 5%, but document them clearly—no repayment expected. Example: $20,000 savings + $5,000 KiwiSaver = 5% on a $500,000 home.

Step-by-Step Guide to Applying

Getting your First Home Loan takes preparation. Follow these actionable steps:

- Check eligibility: Use Kāinga Ora's online tool at kaingaora.govt.nz.

- Save your deposit: Aim for 5%+ to show commitment. Track via apps like PocketSmith.

- Get pre-approval: Approach participating lenders like Kiwibank, Westpac, or Co-operative Bank.

- Find your home: Work with a REINZ agent; focus on properties under caps.

- Apply formally: Submit income proof, credit check, and deposit evidence. Expect LMI calculation.

- Settlement: Pay LMI upfront or add to loan; move in!

Participating lenders (2026): Kiwibank, Westpac, Co-operative Bank, and more—full list on Kāinga Ora site.

Costs and Fees to Budget For

Beyond the deposit, factor in these 2026 realities:

- Lenders Mortgage Insurance (LMI): 1% of borrowed amount, e.g., $4,750 on $475,000 loan. Protects lender; mandatory.

- Interest rates: Often standard 'special' rates despite high LVR—shop around.

- Other fees: Legal ($1,500-$2,500), LIM ($300), building report ($800), moving costs.

- Ongoing: Council rates, insurance, maintenance—budget 1-2% of home value yearly.

Total upfront for $500k home: ~$30,000 (deposit + LMI + fees). Use mortgage calculators on bank sites.

Pros and Cons of Buying with 5% Deposit

Pros

- Enter the market faster—$25k vs $100k savings.

- Use KiwiSaver/gifts flexibly.

- Build equity sooner in a rising market.

- Fixed/floating/offset options available.

Cons

- LMI adds thousands.

- Higher risk if prices fall—negative equity possible.

- Stricter affordability checks; debt issues disqualify.

- Not for luxury homes over caps.

"Changes mean lenders are approving more home loans to buyers with low deposits, and some people might not realise they qualify."

Practical Tips for First-Home Buyers in 2026

- Boost affordability: Pay down debt, avoid new credit. Get free advice from MoneyTalks (moneytalks.co.nz).

- Regional focus: More options outside Auckland—e.g., $500k buys well in Waikato or Canterbury.

- Team up: Couples/pāharakeke qualify on combined income.

- Pre-approval power: Makes offers stronger in competitive sales.

- 2026 market: Most first buyers use <20% deposits; leverage this.

Alternatives if You Don't Qualify

Can't meet criteria? Try:

- 10-15% deposit loans (higher rates).

- Kāinga Whenua for Māori land.

- Family guarantee for 100% (risky).

- Save longer or relocate regionally.

Next Steps to Your First Home

You're closer than you think. Start by checking eligibility on the Kāinga Ora website, gather your documents, and chat with a lender today. With discipline and the right scheme, that 5% deposit could unlock your future. Contact a participating bank or visit lifetimes.co.nz for more Kiwi home-buying guides—your home awaits.

Frequently Asked Questions

Sources & References

-

1

Low-Deposit Home Loans - MoneyHub NZ — www.moneyhub.co.nz

-

2

First Home Loan - Kainga Ora — kaingaora.govt.nz

- 3

-

4

Kāinga Ora First Home Loan - The Co-operative Bank — www.co-operativebank.co.nz

-

5

First Home Loan - Kiwibank — www.kiwibank.co.nz

-

6

First Home Loan | Westpac NZ — www.westpac.co.nz

-

7

Buying Your First Home in NZ in 2026? Watch This First - YouTube — www.youtube.com

-

8

Why 2026 is a 'Goldilocks year' for first-home buyers | RNZ News — www.rnz.co.nz

Related Articles

First Home Grant NZ: How to Get Up to $10000

Buying your first home is one of the biggest financial decisions you'll make, and the New Zealand government wants to help. The First Home Grant puts up to $10,000 directly towards your deposit, makin...

Why 2026 is the Hardest Year to Buy a Home (and How to Beat the Odds)

Imagine standing at the edge of the property ladder in 2026, eyeing your dream home while prices hover stubbornly high, listings pile up, and buyer confidence wavers. For Kiwis, this year feels toughe...

Buying Your First Home in 2026: A Step-by-Step NZ Checklist

Imagine standing in your own Kiwi bach or cosy family home, keys in hand, after years of renting. In 2026, with interest rates stabilising and first-home schemes still strong, buying your first home i...

Selling Your Home? 10 Low-Cost Renovations That Add $50k in Value

If you're planning to sell your home in New Zealand, you don't need to break the bank with a complete renovation to attract buyers and boost your sale price. The good news? Some of the most effective...