Family Trust Tax Changes NZ: What Trustees Need to Know

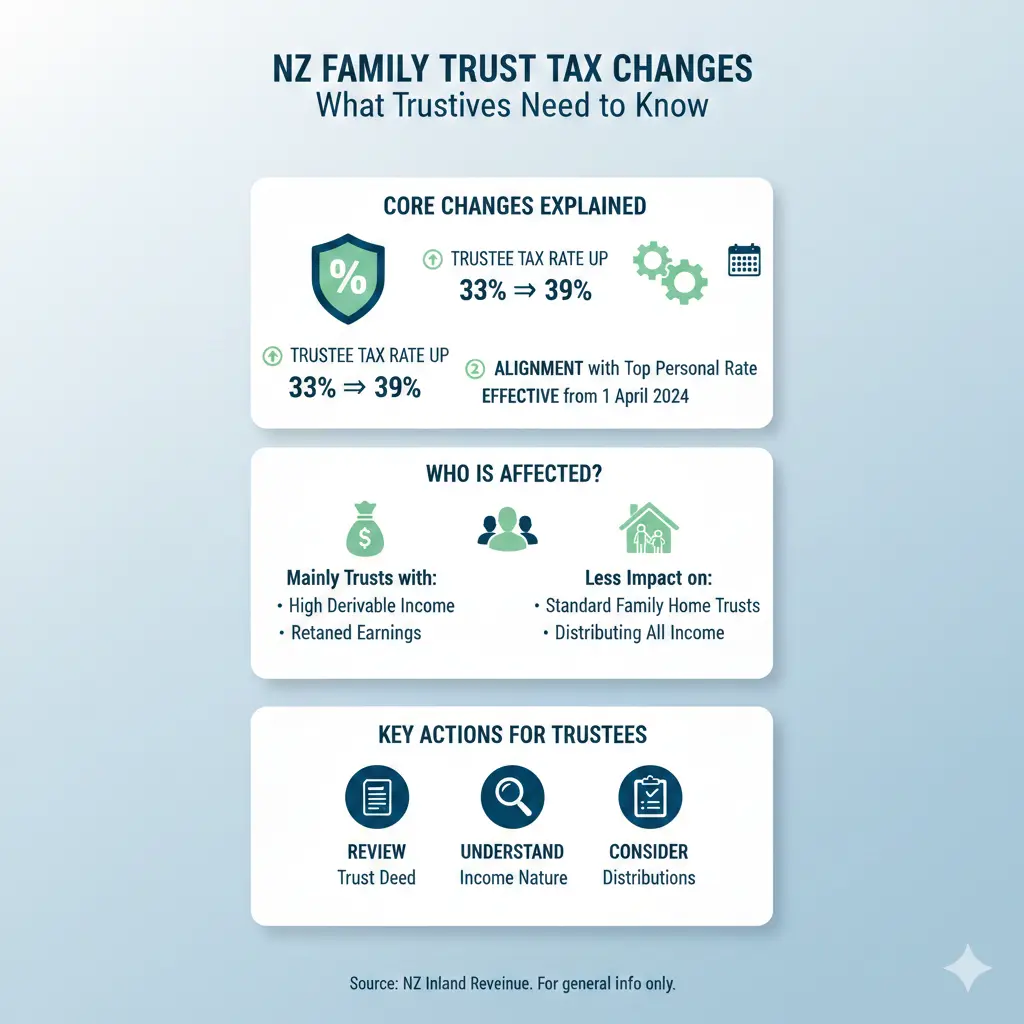

If you're a trustee in New Zealand, the recent hike in the trustee tax rate to 39% from 1 April 2024 has likely grabbed your attention.Family trust tax changes NZ mean it's time to review your strateg...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

If you're a trustee in New Zealand, the recent hike in the trustee tax rate to 39% from 1 April 2024 has likely grabbed your attention.Family trust tax changes NZ mean it's time to review your strategy to avoid unexpected tax bills and ensure compliance.

These changes, aligned with Budget 2023, target undistributed trust income over $10,000 annually, taxing it at the top personal rate to close tax advantages for high earners. For Kiwi families relying on trusts for asset protection or income management, understanding these shifts is crucial—especially with the Trusts Act 2019 still bedding in and new 125-year perpetuity rules in play. This guide breaks down what trustees need to know in 2026, with practical steps to adapt.

Understanding the Core Family Trust Tax Changes

The headline change is the trustee tax rate jumping from 33% to 39% on retained income exceeding $10,000 per tax year (after deductions, before carried-forward losses). This applies from the 2024/25 tax year onwards, matching the top individual marginal rate to prevent income accumulation in trusts as a tax dodge.

Previously, trusts enjoyed a flat 33% on undistributed income, often lower than high earners' rates. Now, unless distributed, that income gets hit harder—prompting many trustees to rethink retention strategies.

The $10,000 De Minimis Threshold

Small trusts get a break: if trustee income is $10,000 or less annually, it stays at 33%. This helps modest family trusts with low-yield investments or interest income, but most rental or business-owning trusts exceed this easily.

- Example: A trust earns $8,000 in bank interest—taxed at 33%.

- Contrast: $12,000 rental profit retained? Now 39%.

Historical Context: Why the Change?

Introduced in Budget 2023 by then-Revenue Minister David Parker, the hike addressed perceptions that wealthy Kiwis used trusts to funnel income at lower rates. With gift duty repealed in 2011, trusts boomed for asset transfers, but IRD scrutiny intensified.

Tax Rules for Trustee vs Beneficiary Income

Trust income splits two ways: retained (taxed to trustees) or distributed (taxed to beneficiaries at their personal rates). Distribution remains the key tax-saving tool, especially for beneficiaries in lower brackets like 10.5% (up to $15,600) or 17.5% ($15,601–$53,500).

Distribution Rules and Timing

To qualify for beneficiary rates, income must be distributed within six months of the tax year-end (e.g., by 31 December for March balances). Trustees must document allocations properly via resolutions and file IR3 returns with IRD.

| Income Source | Taxed to Trustee (Retained) | Taxed to Beneficiary (Distributed) | Key Tip |

|---|---|---|---|

| Rental Income | 39% (over $10k) | Personal rate | Distribute to low-income beneficiaries |

| Business Profits | 39% (over $10k) | Personal rate | Review if trust owns operating businesses |

| Interest/Dividends | 39% (over $10k) | Personal rate | Ideal for minor beneficiaries under thresholds |

Minor Beneficiaries: The Under-16 Trap

Distributions to kids under 16 are taxed at 39% trustee rates, except for the first $1,000 per child, which uses their personal rate. This 'minor beneficiary rule' stops income-splitting abuse.

"The whole point of this rule is to prevent trusts from being used simply to splinter income among young family members to get a better tax outcome."

Impacts on Common Family Trust Scenarios

Most Kiwi family trusts hold family homes, rentals, or investments. Here's how changes bite:

Rental Property Trusts

If your trust nets $50,000 rental profit and retains it, expect ~$19,500 tax at 39% (vs $16,500 at 33%). Distribute to two low-income adult kids ($25k each): tax drops to ~$5,660 total—a $13,840 saving.

Business Owners and Investment Trusts

Trust-run businesses face 39% on retained profits, pushing restructures like company ownership. High-net-worth families may wind up trusts if benefits don't outweigh compliance costs.

Asset Protection Still Viable?

Despite tax hikes, trusts shield from creditors, relationship property claims (under Property (Relationships) Act), and probate. But Trustees Act 2019 mandates duties like acting in beneficiaries' interests—non-compliance risks personal liability.

New Compliance and Legal Obligations

Trustees Act 2019 (effective 2021) extended perpetuity to 125 years and split duties into mandatory (e.g., know terms, act honestly) and default (e.g., prudence). No modifications to mandatory duties allowed.

- Register with IRD: All trusts need an IRD number; file IR3 annually.

- Annual Reviews: Assess tax, investments, and distributions yearly.

- Record-Keeping: Resolutions, accounts, beneficiary notices required.

2026-Specific Updates

Auckland property values remain flat, reducing trust growth but highlighting tax drag on yields. IRD's focus on trusts means audits are up—ensure settlor exclusion from income.

Practical Strategies for Trustees in 2026

Don't panic—adapt. Here's actionable advice:

- Distribute Proactively: Allocate to low-bracket beneficiaries (spouses, adult kids, grandkids over 16). Use resolutions before year-end.

- Review Investments: Shift to growth assets over income to minimise taxable distributions.

- Consider Winding Up: If tax costs outweigh protection, dissolve via deed and transfer assets (mind bright-line test for properties).

- Restructure: Move assets to companies (28% tax) or look-through companies for different rates.

- Get Professional Help: Lawyers draft compliant deeds; accountants model scenarios.

Pro Tip: Run projections: If your trust retains $20k+, 39% costs $7,800 vs $6,600—distribute if possible.

Next Steps for Kiwi Trustees

Grab your trust deed, latest accounts, and call your lawyer or accountant today. Model 2026 distributions to cut tax legally, ensure IR3 compliance, and confirm beneficiary details are current. For personalised advice, visit ird.govt.nz or consult a professional—tax rules evolve, and this isn't advice tailored to you.

Disclaimer: This article provides general information only. Seek independent financial, legal, and tax advice for your situation. Rates current as of 2026.

Frequently Asked Questions

Sources & References

-

1

Family Trusts in NZ: Tax and Legal Considerations — www.gcol.co.nz

-

2

Is Your Family Trust Still Fit for Purpose in 2026? - Shanahans Law — www.shanahanslaw.co.nz

-

3

A Simple Guide to the 39% Trust Tax Rate in NZ — businesslike.co.nz

-

4

The Family Trust — www.lawsociety.org.nz

-

5

Family Trusts May No Longer Be Worth It — www.become.nz

-

6

Why use a trust following the trustee tax rate increase? — www.bellgully.com

-

7

Changes to Tax Laws – What Trustees Need to Know — duncancotterill.com

-

8

How to Set Up a Family Trust in New Zealand: A 2025 Guide — www.arnetlaw.co.nz

-

9

Trustee income tax rates — www.ird.govt.nz

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...