Money and Mental Health: Managing Finances Through Tough Times

The relationship between your finances and your mental health is deeply interconnected. When money worries pile up, stress levels spike—and when you're struggling mentally, managing your finances beco...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

The relationship between your finances and your mental health is deeply interconnected. When money worries pile up, stress levels spike—and when you're struggling mentally, managing your finances becomes even harder. For Kiwis facing economic pressures in 2026, understanding how to protect both your wallet and your wellbeing isn't a luxury; it's essential.

The Real Cost of Financial Stress in New Zealand

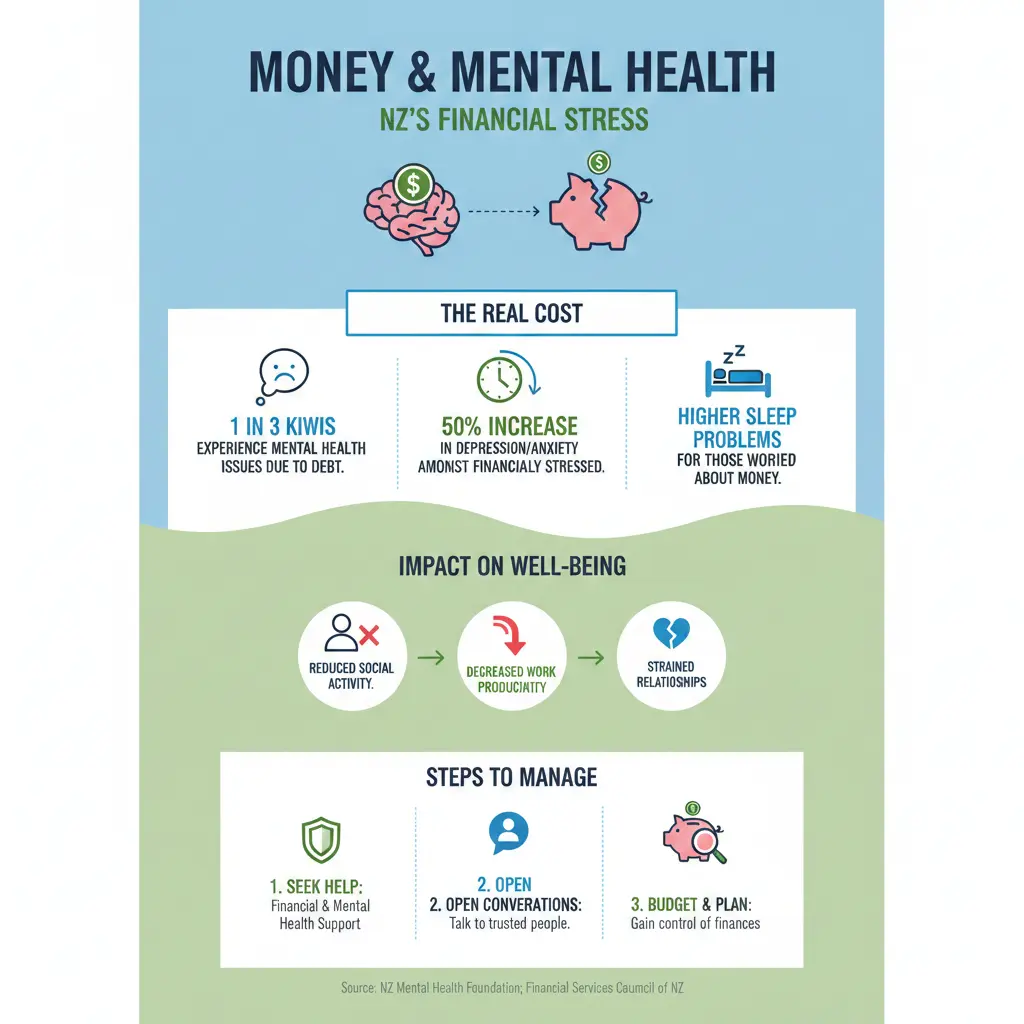

Financial anxiety is one of the biggest workplace stressors for New Zealand workers. Research shows that 54% of Kiwis cite money worries as their main cause of stress, affecting everything from sleep quality to job performance. This isn't just uncomfortable—it has measurable economic consequences.

Mental illness costs New Zealand approximately 5% of our gross domestic product annually, which translated to more than $20 billion in 2023. When financial stress triggers or worsens mental health conditions, the ripple effects extend across your relationships, work productivity, and long-term wellbeing. The good news? Early intervention and proactive financial management can significantly reduce these costs.

In the workplace, the impact is clear. In 2020, New Zealand lost 7.3 million working days and $1.85 billion due to work absence, with stress as a major contributor. Additionally, one in five New Zealand workers report always or often being stressed by work, and many of those stressors relate directly to financial concerns.

Understanding the Money-Mental Health Connection

Financial stress doesn't just feel bad—it actively damages your mental health. When you're worried about paying bills, affording healthcare, or covering unexpected expenses, your body stays in a constant state of alert. This triggers the release of stress hormones like cortisol, which can lead to anxiety, depression, and sleep problems.

The relationship works both ways too. When you're experiencing mental health challenges, managing finances becomes harder. Depression can drain motivation, anxiety can make decisions feel overwhelming, and conditions like ADHD can make it difficult to stay organised with bills and budgets.

Practical Steps to Manage Finances and Protect Your Mental Health

1. Create a Simple Budget You Can Actually Stick To

A budget doesn't need to be complicated or restrictive. Start by tracking where your money actually goes for one month—this removes guesswork and gives you real data. Use apps, spreadsheets, or even pen and paper; the method matters less than the consistency.

Once you see your spending patterns, allocate money to three categories: essentials (rent, food, utilities), debt repayment, and discretionary spending. The goal isn't deprivation; it's awareness. When you understand your money, you feel more in control—and control reduces anxiety.

2. Prioritise Your Mental Health in Your Budget

This might sound counterintuitive when money is tight, but mental health support is an investment, not an expense. Whether that's therapy, counselling, or even a gym membership that helps you manage stress, these aren't luxuries—they're preventative care.

In New Zealand, you can access mental health support through:

- Your GP – Your first point of contact for mental health concerns. They can refer you to subsidised counselling or therapy services.

- District Health Boards – Offer free or low-cost mental health services. Wait times vary, but services are available.

- 1737 Lifeline – Free call or text service available 24/7 for support in crisis moments.

- Employee Assistance Programmes (EAP) – Many employers offer free confidential counselling to staff. Check with your HR department.

- Community organisations – Many offer free or donation-based support groups and services.

3. Build an Emergency Fund (Even If It's Small)

One of the biggest sources of financial anxiety is the fear of unexpected expenses. A car repair, a medical bill, or job loss can send finances spiralling if you have no buffer. Start small—even $20 per week adds up to over $1,000 per year.

Having even a modest emergency fund dramatically reduces anxiety because you know you can handle surprises without going into debt or skipping essential expenses.

4. Address Debt Strategically

Debt is a major mental health stressor for many Kiwis. Rather than ignoring it, create a plan. List all your debts with interest rates and minimum payments. Focus on either paying off high-interest debt first (like credit cards) or smallest balances first (for psychological wins).

If you're struggling, contact your creditors—many will work with you on payment plans. Free debt advice is available through:

- Citizens Advice Bureau – Free financial guidance and support.

- Community Law Centres – Free legal and financial advice.

- Budget services – Available in most regions to help you create sustainable repayment plans.

5. Leverage Government Support Where Eligible

New Zealand has several support systems designed to help when you're struggling financially:

- WINZ (Work and Income) – Provides financial assistance, including emergency grants and benefits. If you're struggling, apply; there's no shame in using support you're entitled to.

- KiwiSaver – If you're facing genuine hardship, you may be able to access your KiwiSaver early. Check eligibility through the IRD website.

- Accommodation Supplement – If you're paying high rent, you may qualify for assistance.

- Community Services Card – Provides discounts on healthcare, prescriptions, and other services if your income is below certain thresholds.

6. Use Employer Wellbeing Support

Many New Zealand employers are increasingly investing in employee wellbeing, recognising that for every dollar spent on early intervention in workplace wellbeing, employers see at least $4.70 in return. Check what your workplace offers—this might include mental health days, counselling services, financial planning workshops, or stress management programmes.

Building Long-Term Financial Resilience

Beyond immediate stress management, building financial resilience protects your mental health long-term. This means:

- Automating payments – Set up automatic bill payments so you're not constantly worrying about due dates.

- Regular financial check-ins – Monthly or quarterly reviews prevent problems from snowballing.

- Upskilling – Learning about money management, investment basics, or career development can increase your sense of control and open new income opportunities.

- Diversifying income – If possible, side projects or freelance work can provide financial security and a sense of agency.

When to Seek Professional Help

If financial stress is causing persistent anxiety, depression, or affecting your ability to function, it's time to seek professional support. You don't need to solve everything alone. A therapist or counsellor can help you:

- Develop coping strategies for financial anxiety

- Address underlying mental health conditions that make money management harder

- Build confidence in financial decision-making

- Create a sustainable plan forward

Your GP is the best starting point. They can refer you to appropriate services and discuss whether counselling or other support would help.

Moving Forward

Managing finances through tough times isn't about achieving perfection or eliminating all stress—it's about taking control where you can and accessing support where you need it. Start with one small action today: whether that's tracking your spending, calling your GP, or researching what support is available to you.

Remember, your mental health and financial wellbeing are interconnected. Protecting one helps protect the other. You're not alone in struggling with money stress, and there's genuine, practical help available across New Zealand. Take that first step today.

Frequently Asked Questions

Sources & References

- 1

- 2

-

3

Statistics on workplace mental health and wellbeing — Mental Health Foundation Aotearoa — mentalhealth.org.nz

-

4

Workplace wellbeing investment returns — Mental Health Foundation Aotearoa — mentalhealth.org.nz

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...