Tertiary Student Finance: Beyond Student Loans

While student loans are a lifeline for many Kiwi tertiary students, they're just one piece of the puzzle. Exploring options like the revamped Fees Free scheme, Student Allowances, part-time work, and...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

While student loans are a lifeline for many Kiwi tertiary students, they're just one piece of the puzzle. Exploring options like the revamped Fees Free scheme, Student Allowances, part-time work, and smart budgeting can slash your study costs and set you up for a stronger financial future.

With tertiary fees rising and living expenses biting harder in 2026, it's crucial to look beyond borrowing. Whether you're kicking off uni, switching careers through polytech, or upskilling via apprenticeships, this guide breaks down practical ways to fund your education without maxing out your debt. We'll cover government support, earning while learning, family strategies, and investment tips tailored for New Zealanders.

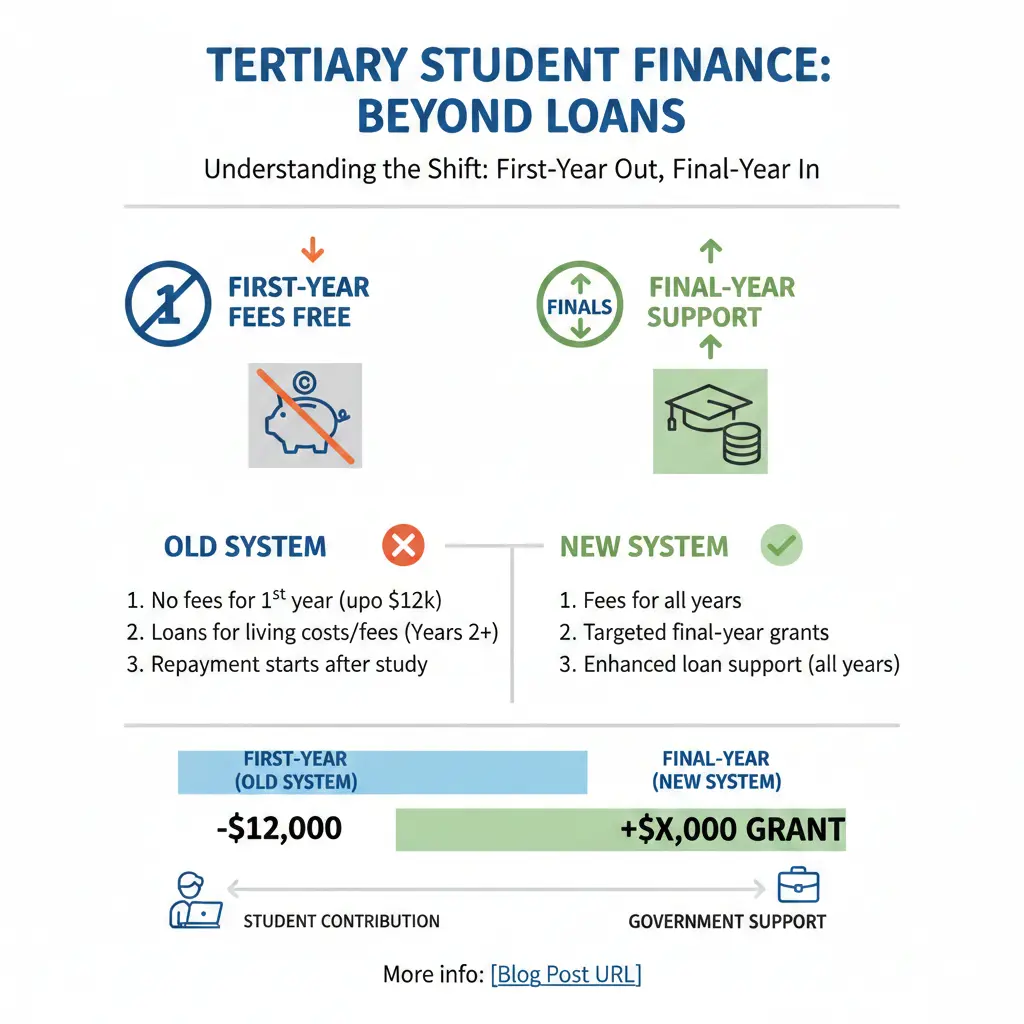

Understanding the Shift: First-Year Fees Free is Out, Final-Year Support is In

The landscape for tertiary funding changed in 2026. Gone is the universal first-year Fees Free for new learners. Instead, eligible students who complete their first qualification can now claim up to $12,000 towards their final year of study or final two years of work-based learning. This shift aims to encourage completion rates and ease the debt burden at the finish line.

Applications opened on 15 January 2026 via Inland Revenue's myIR portal. You pay fees upfront when enrolling, then apply within one year of finishing your first eligible programme. If you studied in 2025, your deadline is 31 December 2026. For those with a student loan, the entitlement credits directly to your balance; otherwise, it hits your bank account.

Who Qualifies for Final-Year Fees Free?

- New Zealand citizens or permanent residents enrolled in approved tertiary providers.

- Those who've passed their first eligible qualification (levels 3+ on the NZQCF).

- Full-time or equivalent study in the final year.

- Excludes those who've already used Fees Free or certain prior qualifications.

Check eligibility on the Inland Revenue Fees Free page. Pro tip: Plan your enrolment to align with this – it's a game-changer for multi-year degrees.

Student Allowances: Weekly Cash Without Repayment

If living costs are your biggest worry, the Student Allowance provides non-repayable weekly payments. In 2026, full-time students can receive up to $323.43 per week for living expenses, depending on your situation.

Administered by StudyLink (now part of Inland Revenue), these allowances consider your age, living arrangements, and income. Apply by the key deadline: for 2026, it's 16 December 2025. Late applications might mean missed payments.

Eligibility Essentials

| Category | Key Requirements | Max Amount (2026) |

|---|---|---|

| Full-time domestic students | 20+ years old, studying approved course >0.3 EFTS, income under threshold | $323.43/week |

| With dependents | Partner/child income test, accommodation supplement possible | Up to $400+/week |

| Part-time | At least 0.3 EFTS, proportional rates | Reduced rate |

Can't get living costs if you're in prison or on a main benefit. Pair this with a student loan for fees – allowances don't cover tuition.

Part-Time Work and Earnings Strategies

Many Kiwis juggle study with work, especially during breaks. In 2026, student visa holders (if international, but focusing on domestics here) and locals can earn without derailing allowances, as long as you stay under income thresholds.

Actionable tips:

- Holiday work: Retail, hospitality, or seasonal farm jobs pay well. Apply for a student loan repayment exemption if earnings push you over the $24,128 threshold – no repayments needed if studying full-time.

- On-campus gigs: Tutoring, library roles, or research assistants via your uni's career centre.

- Gig economy: Drive for Uber Eats or freelance on platforms like Airtasker, fitting around lectures.

- Track earnings via myIR to avoid over-repaying on loans.

Aim for 10-15 hours/week during term to avoid burnout. WINZ offers job support for students too.

Family Support and Smart Cash Management

Parents often wonder: pay fees upfront or let student loans handle it? With $10,000 saved, as in one NZ Herald case, it's often smarter to invest that cash interest-free while your child borrows.

Student loans remain interest-free if you live in New Zealand. Repayments start at 12% above $24,128 annual income. Use family funds for non-loanable costs like laptops or bonds, or invest in low-risk options:

Investment Options for Family Savings (3-5 Years)

- KiwiSaver: Boost your child's account for retirement – government contributes via employer matches.

- Term deposits: 4-5% rates in 2026, low risk.

- Conservative managed funds: 5-7% average returns, via banks like ASB or ANZ.

- First home deposit: Park it for their future property purchase, eligible for KiwiBuild schemes.

Avoid high-risk shares. Consult a financial adviser – past performance isn't indicative.

Other Funding Avenues: Scholarships, Grants, and More

Beyond government staples, tap into:

- Scholarships: Uni-specific (e.g., University of Auckland International Student Excellence), or field-based like Prime Minister's Scholarships for tech studies. Apply early via providers' sites.

- Course-related costs: Up to $1,000/year via student loan for books, computers.

- ACC Study Awards: For those with covered injuries, up to full fees.

- Employer sponsorship: Apprenticeships via TEC-funded programmes cover work-based learning.

- Charities: Rotary or Lions clubs offer local grants for Kiwi students.

2026 sees tighter provider funding scrutiny by TEC, ensuring sustainable options.

Budgeting Tools and Avoiding Pitfalls

Track expenses with apps like PocketSmith (NZ-based). Sample weekly budget for Auckland uni student:

| Expense | Amount |

|---|---|

| Rent (flat share) | $200 |

| Food | $100 |

| Transport | $50 |

| Misc (phone, fun) | $50 |

| Total | $400 |

With allowance at $323, top up via work. Watch student services fees – regulated for 2026, up to $500/year for support services.

Disclaimer: This isn't personalised financial advice. Consult StudyLink, IRD, or a certified adviser for your situation.

FAQ

1. Can I get both a Student Allowance and a student loan?

Yes, they complement each other – loans for fees/living, allowance for weekly non-repayable support.

2. What's the student loan repayment threshold in 2026?

$24,128 gross income per year; 12% above that.

3. How do I apply for final-year Fees Free?

Via myIR after completing your first qualification, from 15 Jan 2026.

4. Are student loans interest-free overseas?

No – interest applies if you're out of NZ for 183+ days/year.

5. Can parents gift money without tax issues?

Gifts under $27,000/year are tax-free; track via IRD for larger amounts.

6. What's the deadline for 2026 Student Allowance?

16 December 2025.

Next Steps to Secure Your Funding

1. Log into MyStudyLink or myIR to check eligibility today.

2. List your course costs and apply for allowances/loans ASAP.

3. Hunt scholarships via Education Counts or your provider.

4. Build a budget and line up part-time work.

5. Chat with a WINZ adviser or financial mentor for tailored help.

By diversifying beyond loans, you'll graduate with less debt and more options. Start planning now – your future self will thank you.

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...