Unit Titles vs Fee Simple: Understanding Property Ownership

Ever wondered why one Kiwi homeowner can renovate their backyard deck without a hitch, while their neighbour in the next apartment block needs approval from a committee? The answer lies in the type of...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Ever wondered why one Kiwi homeowner can renovate their backyard deck without a hitch, while their neighbour in the next apartment block needs approval from a committee? The answer lies in the type of property ownership: Unit Titles vs Fee Simple. In New Zealand's dynamic property market, grasping these differences is crucial for buyers, sellers, and investors alike, especially as we navigate 2026's housing landscape with rising interest rates and evolving regulations.

This guide breaks down Unit Titles vs Fee Simple: Understanding Property Ownership in plain Kiwi terms. We'll explore what each means, their pros and cons, real-world examples, and practical steps to help you make informed decisions—whether you're a first-home buyer eyeing a Wellington townhouse or an investor in Auckland apartments.

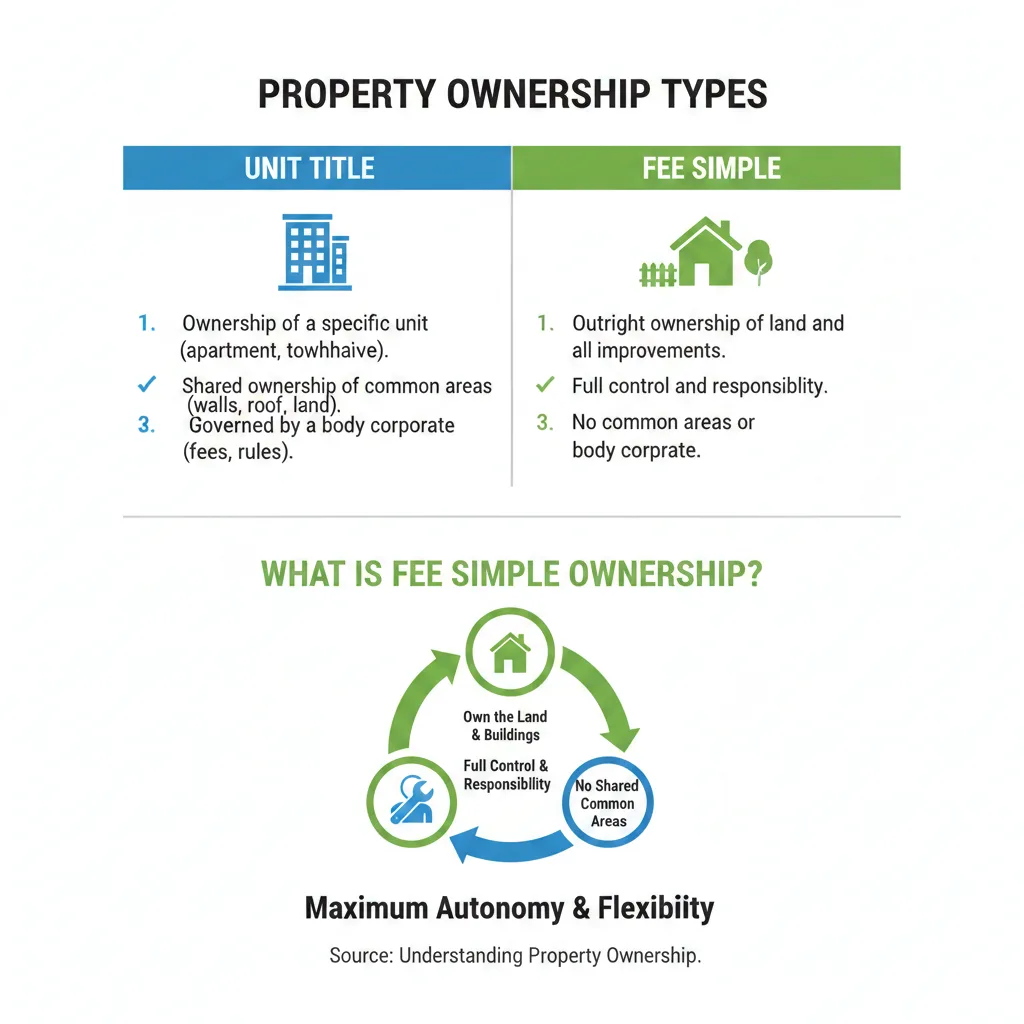

What is Fee Simple Ownership?

Fee simple, often called freehold, is the gold standard of property ownership in New Zealand. It grants you complete, indefinite ownership of both the land and any buildings on it. No one else owns the ground beneath your feet, giving you maximum control—subject only to local council rules, zoning laws, and any easements or covenants noted on the title.

Picture a standalone house in Christchurch's suburbs: you own it all outright. Want to add a sleep-out or subdivide? You're generally free to proceed without consulting neighbours, as long as you meet building consents from your local council.

Key Features of Fee Simple

- Full autonomy: Build, renovate, or landscape without shared approvals.

- No ongoing levies: No body corporate fees—your costs are just rates, insurance, and maintenance.

- Higher market appeal: Buyers prefer fee simple for its simplicity and resale value boost.

- Subject to title restrictions: Check for easements (e.g., neighbour's right-of-way) or covenants (e.g., no commercial use).

In 2026, with KiwiSaver withdrawals supporting more first-home purchases, fee simple remains the top choice for 70-80% of standalone homes, per recent Stats NZ data on title distributions.

What is Unit Title Ownership?

Unit titles, also known as strata or stratum estates, dominate multi-unit developments like apartments, townhouses, and retirement villages. You own your individual unit (including balconies or garages) plus a proportional share of common areas like driveways, pools, and roofs. The body corporate—a collective of all owners—holds the land title for everyone's benefit.

Think of a modern Auckland high-rise: your two-bedroom unit is yours alone, but the lobby, lifts, and gym are shared. This setup avoids ground rent but introduces body corporate levies.

Key Features of Unit Titles

- Shared responsibility: Body corporate manages maintenance, insurance, and rules via the Unit Titles Act 2010 (amended 2022).

- Annual levies: Expect $3,000-$10,000+ yearly (2026 averages), covering insurance, repairs, and a long-term maintenance fund (LTMF).

- Body corporate governance: Mandatory membership; vote on budgets, elect committees, and approve major works.

- Restrictions on changes: Alterations often need body corporate consent to protect shared elements.

Recent Unit Titles Amendment Act changes in 2022 strengthened rules for complexes with 10+ units, mandating better financial disclosures—vital for buyers reviewing pre-purchase reports.

Unit Titles vs Fee Simple: A Side-by-Side Comparison

To help you decide, here's a clear breakdown of Unit Titles vs Fee Simple across key factors relevant to Kiwi buyers in 2026.

| Aspect | Fee Simple (Freehold) | Unit Title |

|---|---|---|

| Ownership | 100% land + building | Unit + share of common property |

| Control Over Changes | High (council consent only) | Medium (body corporate approval needed) |

| Ongoing Costs | Rates + insurance (~$3,000-$6,000/yr) | Levies ($3,000-$15,000+/yr) + rates |

| Resale Value | Typically higher premium | Lower entry price, but levy risks |

| Best For | Families, investors seeking independence | Urban dwellers, low-maintenance seekers |

| Risks | Title defects (e.g., covenants) | Special levies, poor body corporate |

This table highlights why fee simple suits those valuing freedom, while unit titles appeal for affordability in cities like Wellington or Dunedin.

Pros and Cons: Making the Right Choice

Advantages of Fee Simple

- Ultimate flexibility—no neighbour vetoes on renovations.

- Predictable costs without surprise levies.

- Easier financing; banks view them favourably for mortgages.

- Stronger equity for KiwiSaver first-home grants or IRD tax deductions on interest (post-2024 rules).

Drawbacks of Fee Simple

- Higher upfront purchase price.

- Full maintenance burden falls on you.

- Less common in dense urban areas.

Advantages of Unit Titles

- Cheaper entry—ideal for first-home buyers using Kāinga Ora schemes.

- Shared upkeep; professional management handles repairs.

- Access to amenities like gyms or pools at lower personal cost.

Drawbacks of Unit Titles

- Levies can spike with special levies (e.g., earthquake repairs in Christchurch).

- Body corporate disputes or sinking funds can devalue properties.

- Resale slower if fees rise amid 2026's inflation pressures.

Real-World Examples in New Zealand

In Auckland's Wynyard Quarter, fee simple townhouses fetch premiums for their standalone appeal, while nearby unit title apartments offer harbour views at 20-30% less—but with $8,000 annual levies. Post-2022 amendments, a Lower Hutt body corporate successfully funded a $2 million roof replacement via fair levies, showcasing good governance.

Christchurch buyers often convert cross-leases to fee simple for $20,000-$50,000, boosting values by 10-15% amid rebuild demand. Always check LINZ titles via your lawyer before bidding at auction.

Legal and Financial Implications for Kiwis

Under the Unit Titles Act 2010 (2022 updates), sellers must provide body corporate disclosure statements, including financials and minutes—review these for red flags like disputes or underfunded LTMF. Fee simple properties shine in ACC claims for standalone builds but watch IRD capital gains rules if flipping (no general CGT as of 2026, but bright-line test applies).

Mortgage-wise, banks cap unit title loans at 80-90% LVR if levies exceed thresholds. Use Settled.govt.nz for free guides and consult WINZ for housing support if eligible.

Practical Tips for Buyers and Owners

- Due diligence: Get a LIM report and title search from LINZ ($40 online).

- Review body corporate: For unit titles, scrutinise 3 years' financials—aim for healthy LTMF (10% of replacement value).

- Conversion options: Cross-lease to fee simple? Budget $30,000+ for surveyors, solicitors, and LINZ lodgement.

- Lawyer up: Engage a property lawyer early; costs $1,500-$3,000 but saves heartache.

- Budget buffer: Add 20% to levies for specials in unit titles.

- Sell smart: Highlight fee simple perks in listings for faster sales.

"Thorough due diligence by a property lawyer is essential to identify defective titles or restrictive covenants before you sign."

FAQ: Unit Titles vs Fee Simple

1. Can I convert a unit title to fee simple?

Rarely feasible due to shared ownership; subdivisions require full body corporate and council approval—costly and complex. Stick to cross-lease conversions.

2. How much are body corporate levies in 2026?

Averages $4,000-$12,000/year for Auckland units, varying by size and location. Check disclosure statements.

3. Which is better for investment?

Fee simple for control and yields; unit titles for cash flow if levies are low. Factor bright-line test (10 years).

4. Do fee simple properties have body corporates?

No—unless part of a residents' society (voluntary). Pure fee simple means no mandatory fees.

5. What's the risk of special levies in unit titles?

High for older blocks; 2022 laws mandate sinking funds, but poor management can hit owners with $10,000+ calls.

6. How do I check ownership type before buying?

Review the LIM and title via your lawyer or LINZ portal. Settled.govt.nz explains all types.

Next Steps for Smart Property Decisions

Ready to dive in? Start with a free title search on LINZ, grab a body corporate pack for units, and chat to a registered lawyer or valuer. For first-home helpers, check Kāinga Ora or KiwiSaver rules via ird.govt.nz. Remember, this isn't personalised advice—consult professionals for your situation, as property laws evolve.

Whether fee simple freedom or unit title convenience fits your Kiwi lifestyle, knowledge empowers better buys. Bookmark Lifetimes NZ for more money guides.

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...