Property vs Shares: Where Should Kiwis Invest?

Ever wondered if that deposit in your KiwiSaver could grow faster in shares, or if buying a rental property in Christchurch is the smarter long-term play? For Kiwis facing high living costs and tricky...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Ever wondered if that deposit in your KiwiSaver could grow faster in shares, or if buying a rental property in Christchurch is the smarter long-term play? For Kiwis facing high living costs and tricky markets, deciding between property vs shares boils down to your goals, risk tolerance, and timeline. Let's break it down with real NZ data and practical advice to help you choose wisely.

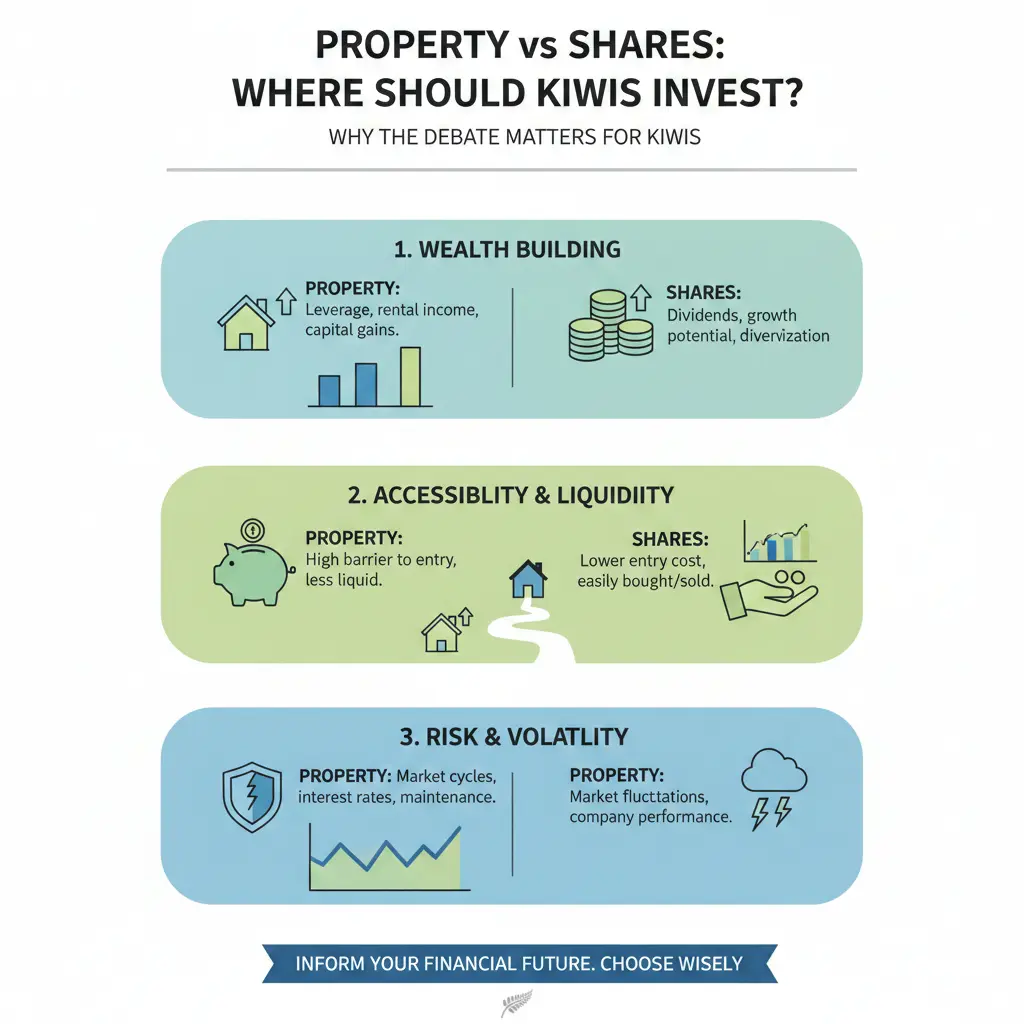

Why the Property vs Shares Debate Matters for Kiwis

In Aotearoa, investing is more than numbers—it's about building security amid rising rates, job shifts, and KiwiSaver tweaks. Property has long been our go-to, with median house prices hovering around $808,430 as of late 2025. Shares, via the NZX or global markets, offer liquidity and diversification without the 20% deposits or maintenance hassles. But which delivers better returns for 2026 and beyond? We'll compare historical performance, forecasts, risks, and tax rules tailored to New Zealanders.

Property Investing in New Zealand: The Kiwi Classic

Property remains a cornerstone for many Kiwis, promising capital growth, rental income, and leverage through mortgages. But post-2022 peaks, values dipped 17.6% nationally, stabilising at flat levels through much of 2025.

2026 House Price Forecasts

Expect modest growth rather than booms. The Reserve Bank predicts 3.75% national house price rises by December 2026, while ANZ forecasts 5%. Cotality's chief economist sees cautious optimism, with 5% potential uplift as mortgage refixes drop rates into the mid-4%s and unemployment eases from above 5%.

- Auckland: Recovery in mid-teens percentages from troughs, but standalone houses lag 14% below peaks—townhouses even more.

- Christchurch: Standalone homes surpassing peaks; townhouses flat due to supply surges.

- Provinces like Southland or New Plymouth: Hitting records, buoyed by farming returns and resilience.

A $800,000 property could hit $830,400 by year-end on ANZ's view, netting $30,400 capital gain before costs. Yields? Around 3-4% gross in main centres, higher (up to 6%) in affordable spots like some provincial areas.

Pros of Property

- Tangible asset: You can live in it, rent it, or pass it to tamariki.

- Leverage: Borrow at 4-5% to control a big asset; equity builds as prices rise.

- Gearing benefits: Interest deductibility reinstated for investors since 2024, though phased.

- Inflation hedge: Rents and values often track CPI.

Cons and Risks

Illiquidity means months to sell, plus high entry barriers—think 20-40% deposits under LVR rules. Maintenance, council rates, insurance, and vacancies eat yields. With DTI limits incoming and townhouse supply ramping, broad growth like 2012-2021 is off the table. Unemployment ticks and election-year uncertainty (CGT talk, RMA reforms) could mute gains.

Shares Investing: The Flexible Alternative

Shares via NZX 50 or ETFs like Smartshares offer diversification without the landlord grind. No plumbing bills, instant liquidity, and dividends—perfect for busy Kiwis.

Recent NZX Performance and 2026 Outlook

The NZX 50 returned about 8.5% annually over the past decade (to 2025), outpacing property's leveraged but volatile returns post-fees. Globally, S&P 500 equivalents via NZ platforms averaged 10-12% long-term. For 2026, with OCR at 2.25-3% and economy recovering, expect 7-10% from diversified portfolios as rates stabilise.

KiwiSaver funds heavy in shares (e.g., growth funds) delivered 9-11% in 2025 amid rate cuts, beating bank term deposits at 4-5%.

Pros of Shares

- Liquidity: Sell anytime during market hours—no auctions.

- Low entry: Start with $100 via Sharesies or Hatch; no big deposits.

- Diversification: Spread across 50+ companies or global ETFs.

- Dividends: 4-6% yields from NZX staples like Fisher & Paykel Healthcare.

Cons and Risks

Volatility hits hard—NZX dropped 10-15% in 2022 corrections. No leverage means slower compounding unless using margin loans (risky). Market crashes, like 2008's 40% plunge, test nerves. For NZ-specific, small market means reliance on globals.

Head-to-Head: Property vs Shares Comparison

Here's a side-by-side for a $100,000 investment over 10 years (assuming 2026 starts; conservative estimates).

| Factor | Property (Leveraged) | Shares (Diversified ETF) |

|---|---|---|

| Avg Annual Return (Gross) | 6-8% (3-5% growth + 3% yield) | 8-10% (cap growth + dividends) |

| 2026 Forecast | 3.75-5% price rise | 7-10% (economy rebound) |

| Costs | 5-7% (rates, maint, agents) | 0.5-1% (fees) |

| Risk Level | High (illiquid, local market) | Medium-High (volatile but diversified) |

| Tax | Bright-line 2-10 yrs; deduct interest | Dividends PIE (10.5-28%); no CGT |

| Liquidity | Weeks-Months | Instant |

Property shines with leverage: $100k deposit on $500k buy could double equity in good years. Shares win on ease and total returns for unleveraged investors. Historically, property edged shares pre-2022 (7-9% vs 7%), but shares pulled ahead post-correction.

New Zealand Tax Rules: Key Differences

Tax shapes choices. Property: Bright-line test taxes gains if sold within 2 years (main home) or 10 (investor)—IRD rules. Rental losses offset via interest deductibility (full from 2024/25 for existing loans). Shares: No capital gains tax—huge win. Dividends taxed at your PIE rate (10.5% low-income), with imputation credits. Use IRD's investor tools to model.

Risks in 2026: What Kiwis Need to Watch

Both face OCR hikes by Dec 2026 (ANZ view), pushing mortgage rates up. Unemployment above 5% curbs rents/demand. Property risks: Supply glut in townhouses, RMA changes. Shares: Global slowdowns, election volatility. Diversify—don't all-in one.

Practical Tips: Where Should You Invest?

- Assess goals: Retirement? Shares via KiwiSaver. Family legacy? Property.

- Risk tolerance: Hands-off? Shares. Control freak? Rentals.

- Start small: Try Sharesies for shares; house hack (buy to live/rent) for property.

- Run numbers: Use Opes Partners calculator for property yields; MoneyHub for shares forecasts.

- Diversify: 60/40 property/shares split common for balanced Kiwis.

- Seek advice: Authorised financial adviser or IRD webinars—free via sorted.org.nz.

Next Steps for Smart Kiwi Investing

Crunch your numbers with free tools from sorted.org.nz or IRD.govt.nz. Chat to a financial adviser via FMA register. Track ANZ Property Focus monthly for updates. Whether property in provincial gems or shares for liquidity, align with your whanau goals—steady wins over time. Start today: open a Sharesies account or scout OneRoof listings.

Frequently Asked Questions

Sources & References

-

1

House Price Predictions (2026): What to Expect in NZ | Opes Partners — www.opespartners.co.nz

-

2

New Zealand House Prices 2026: What the Numbers Actually Say — www.najibrealestate.co.nz

- 3

-

4

Why 2026 Could Be the BEST Time to Buy a house in New Zealand — www.youtube.com

-

5

Property Focus | For homeowners and investors - ANZ — www.anz.co.nz

-

6

The 6 Worst Places to Invest in NZ for 2026 (The Data Is Brutal) — www.youtube.com

-

7

House Price Predictions 2026 & 2027 - MoneyHub NZ — www.moneyhub.co.nz

Related Articles

Ethical Investing in NZ: Top 5 Sustainable Funds for Kiwis

Ever wondered if you can grow your KiwiSaver or investments while doing good for the planet and people? Ethical investing in New Zealand is booming, with Kiwis pouring billions into funds that priorit...

Beginner's Guide to Investing in New Zealand

Getting started with investing in New Zealand doesn't have to be complicated. Whether you're looking to grow your wealth, save for retirement, or build financial security, there are plenty of accessib...

How to Buy Shares in New Zealand: Step-by-Step Guide

Ever wondered how to dip your toes into share investing without getting overwhelmed? Whether you're saving for a house deposit, retirement, or just want to grow your hard-earned cash, buying shares in...

ETFs vs Managed Funds: Which is Better for Kiwi Investors?

When you're ready to invest your money, you'll likely come across two main options: exchange-traded funds (ETFs) and managed funds. Both offer diversification and professional management, but they wor...