Brightline Rule Changes 2024: Current Property Tax Rules

Imagine flipping a Kiwi bach in under two years and keeping every dollar of profit tax-free—thanks to the latest Brightline Rule changes 2024. For property investors and homeowners across New Zealand,...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine flipping a Kiwi bach in under two years and keeping every dollar of profit tax-free—thanks to the latest Brightline Rule changes 2024. For property investors and homeowners across New Zealand, these updates signal a major shift in how we handle residential land sales, making tax planning simpler and more predictable in 2026.

Whether you're a first-time investor in Auckland eyeing a quick resale or a family in Christchurch restructuring assets, understanding the current property tax rules is crucial. From the shortened two-year period to tweaks in main home exclusions and interest deductibility, these changes affect everyone from landlords to everyday Kiwis selling up. Let's break it down step by step, with practical tips tailored to our New Zealand context.

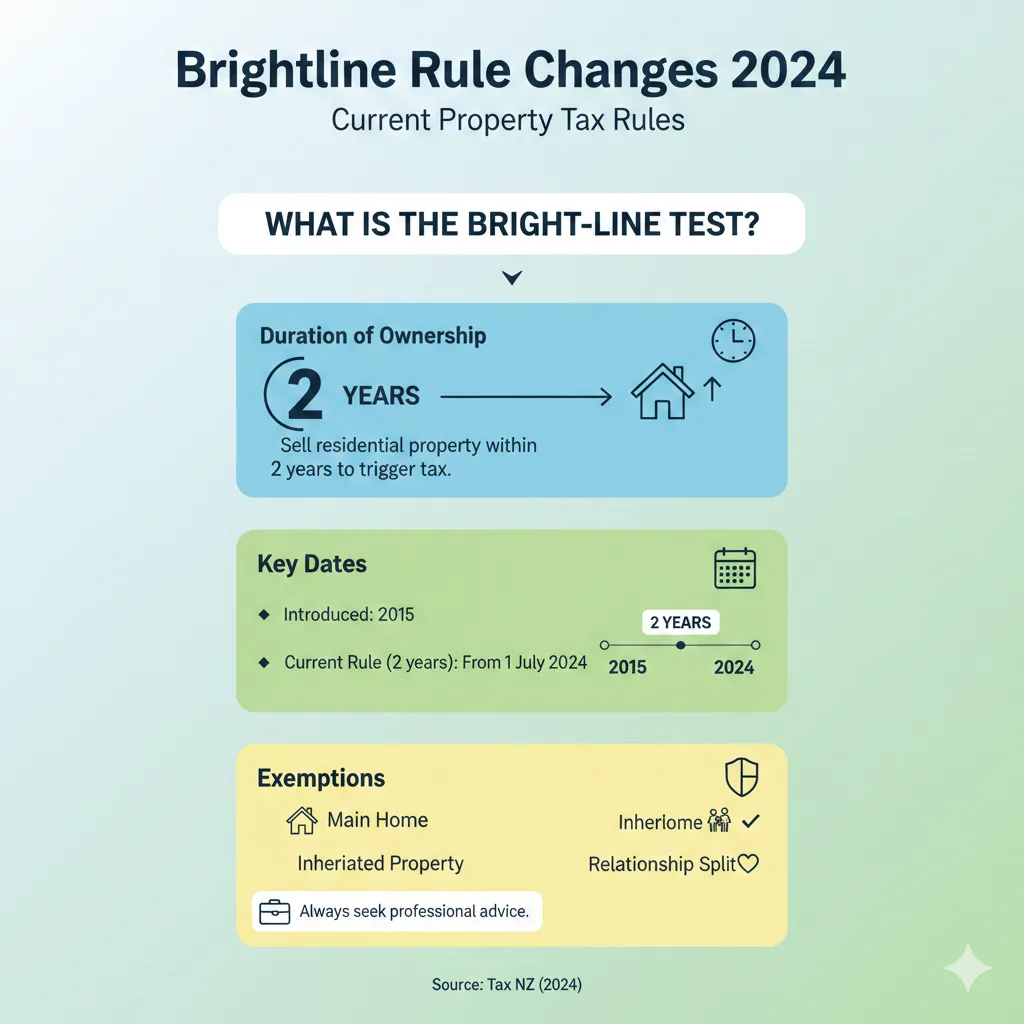

What is the Bright-Line Test?

The Bright-Line Test is an IRD rule designed to tax profits from residential property sales treated as income, rather than capital gains. It applies if you sell within a set period after acquisition, capturing gains on houses, apartments, townhouses, and bare residential land—but not farmland or business premises.

Before 2024, periods stretched to five or ten years, creating headaches for long-term holders. Now, in 2026, the focus is squarely on short-term flips, aligning with government promises to simplify rules for genuine investors.

Why the Changes Matter for Kiwis

These reforms restore balance after years of extended timelines that deterred investment. For instance, a Hamilton landlord who bought in 2023 can now sell after July 2024 without Bright-Line tax, as long as it's beyond two years—freeing up capital for KiwiSaver top-ups or family needs. But get it wrong, and you'll face IRD scrutiny come tax time.

Key Brightline Rule Changes 2024: The New 2-Year Period

The headline change hit on 1 July 2024: the Bright-Line period for properties sold on or after this date dropped to **two years** for all residential land, scrapping the old five- and ten-year distinctions and new-build separations.

Bright-Line Start and End Dates

- Start date: Generally, when the property title transfers to you via LINZ (settlement date for standard buys). For off-the-plan purchases, it's the binding sale and purchase agreement (SPA) date.

- End date: When you sign a binding SPA to sell (not settlement).

Pro tip: Track these dates meticulously. Use LINZ records or your lawyer's settlement docs to confirm—vital for IRD filings.

Properties Sold Before 1 July 2024

Legacy rules linger for earlier sales:

| Acquisition Date | Bright-Line Period |

|---|---|

| On or after 27 March 2021 | 5 years (new builds) or 10 years (others) |

| 29 March 2018 to 26 March 2021 | 5 years |

If you sold between 1 April and 1 July 2024, stick to these periods in your 2025 tax return.

Main Home Exclusion: Back to All-or-Nothing

Good news for families: the main home exclusion is now a full pass if the property was your **main home for more than 50% of the time AND land area**. No more pro-rating—it's all or nothing, reverting to pre-2024 simplicity.

Example: You buy a Wellington villa, live there 60% of the time over 18 months, then rent it out. Sell after 1 July 2024? Fully exempt, even if under two years. But dip below 50%, and the entire gain is taxable.

"The exclusion will apply in full, if the property has been used as a main home for more than 50% of the time (and more than 50% by land area)."

Other Exemptions

- Inherited properties

- Farmland or business premises

- Overseas main homes (but NZ tax residents pay on overseas flips within two years)

Interest Deductibility: Phased Return for Investors

Alongside Bright-Line tweaks, interest on residential loans phases back to full deductibility:

- From 1 April 2024: 80% deductible

- From 1 April 2025: 100% deductible

For a Dunedin rental with $30,000 annual interest, that's $24,000 deductible in 2024/25, rising to full next year. Pair this with the shorter Bright-Line, and cash flow improves dramatically for compliant landlords.

Practical Tip: Review Your Loan Structure

Chat with your bank or accountant now. Mix residential and commercial loans? Segregate to maximise deductions, but document everything for IRD audits.

Roll-Over Relief: Family and Trust Essentials

Transferring property within families or trusts? Roll-over relief defers Bright-Line tax if:

- Underlying ownership stays substantially the same

- Associates (family members) are involved

- Used only once per property every two years

Scenario: Mum gifts her Auckland section to a family trust holding 100% beneficiary interest. No tax trigger, preserving the two-year clock. Ideal for estate planning or KiwiSaver-aligned wealth protection.

How to Calculate Your Bright-Line Tax Liability

Step-by-step for 2026 filers:

- Confirm acquisition and SPA dates

- Check if within two years (post-1 July 2024 sales)

- Apply exclusions (main home, roll-over)

- Calculate gain: Sale price minus cost base (purchase + improvements)

- Tax at your marginal rate (up to 39% for high earners)

Tool tip: Use IRD's online calculator or myIR portal for provisional estimates. Report via your end-of-year tax return.

Common Pitfalls to Avoid

- Ignoring SPA dates over settlement

- Miscalculating main home usage (keep power bills, electoral roll proof)

- Forgetting overseas properties if you're a NZ tax resident

Practical Advice for New Zealand Property Owners

As we hit 2026, here's actionable Kiwi-focused strategy:

- Buy-and-hold investors: Breathe easy—two years covers most flips without tax.

- Landlords: Time sales post-two years; claim full interest from April 2025.

- First-home buyers: Use as main home >50%? Sell anytime tax-free.

- Developers: Watch off-the-plan rules; structure via companies for relief.

Consult IRD's property hub or a local accountant. For WINZ or ACC overlaps (e.g., selling to fund retirement), cross-check eligibility.

FAQ: Common Brightline Questions from Kiwis

Does the new 2-year rule apply to my 2023 purchase?

Yes, if sold on/after 1 July 2024. Pre-July sales follow old rules based on acquisition date.

What's a 'main home' under the rules?

Your primary residence >50% time and land area. Prove with residency docs.

Can I deduct interest on my rental in 2026?

Fully, since 1 April 2025. Track via accounting software.

What about gifting property to kids?

Roll-over relief likely applies if family-linked and first use in two years.

Do overseas buys count?

Yes, for NZ tax residents selling within two years.

How do I report Bright-Line income?

Via myIR with IRD numbers for buyer/seller. Deadlines align with tax year-end.

Navigating Brightline Rule changes 2024 puts you ahead in New Zealand's property game. With a shorter window, full interest deductions, and smarter exclusions, 2026 offers clearer paths to build wealth—whether flipping in Rotorua or holding long-term in Queenstown.

Next steps:

- Review property dates against IRD timelines

- Log into myIR for personalised guidance

- Book a tax advisor—don't DIY complex scenarios

- Monitor ird.govt.nz for updates

Disclaimer: This is general info, not advice. Seek professional financial or tax guidance for your situation, especially with IRD, KiwiSaver, or WINZ implications.

Related Articles

Working Multiple Jobs NZ: Tax and Legal Considerations

Juggling multiple jobs can boost your income, but it's crucial to understand the tax implications and legal requirements that come with working more than one role in Aotearoa. Whether you're a contrac...

Name Changes NZ: Legal Process and Costs

Considering a fresh start with a new name? Whether it's after marriage, divorce, or simply embracing a personal transformation, changing your name in New Zealand is straightforward but requires follow...

Holiday Home Tax Rules NZ: Private Use and Rental

Own a bach in Coromandel or a holiday home in Queenstown? You're not alone—many Kiwis cherish these escapes, but renting them out while enjoying personal use can trip you up on tax rules. Getting the...

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...