DTI Ratios NZ: How Debt-to-Income Rules Affect Your Borrowing

If you're a Kiwi dreaming of buying your first home or expanding your property portfolio, you've likely heard about DTI ratios NZ. These debt-to-income rules, introduced by the Reserve Bank of New Zea...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

If you're a Kiwi dreaming of buying your first home or expanding your property portfolio, you've likely heard about DTI ratios NZ. These debt-to-income rules, introduced by the Reserve Bank of New Zealand (RBNZ) in July 2024, are reshaping how much you can borrow for a mortgage. Understanding how these restrictions affect your borrowing power is crucial in today's market.

In this guide, we'll break down what DTI ratios mean for you, how to calculate yours, and practical steps to improve it. Whether you're an owner-occupier or investor, these rules could determine if you secure that home loan. Let's dive in.

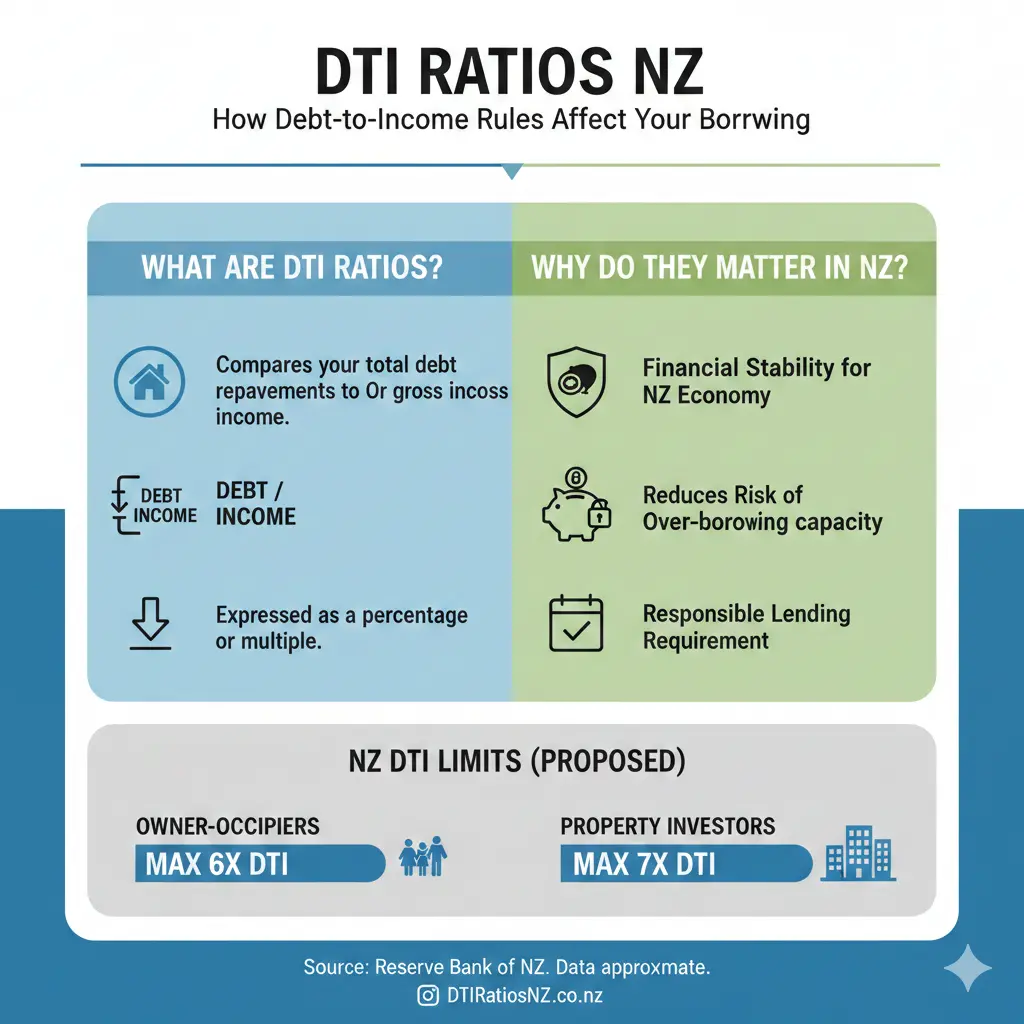

What Are DTI Ratios and Why Do They Matter in New Zealand?

The debt-to-income (DTI) ratio measures your total debt against your gross annual income, expressed as a multiple. It's a key tool banks use to assess if you can afford repayments without overextending financially.DTI ratios NZ became a headline act when the RBNZ enforced restrictions from 1 July 2024 to promote financial stability and curb risky lending.

Before these rules, banks focused heavily on loan-to-value (LVR) ratios. Now, DTI adds an income-based layer, ensuring debt doesn't spiral beyond what Kiwis can service. This is especially relevant amid rising interest rates and house prices in 2026.

The Purpose Behind RBNZ's DTI Restrictions

The RBNZ introduced DTI 'speed limits' alongside LVR rules to protect New Zealand's economy from housing downturns. By limiting high-DTI lending, they reduce default risks during economic slowdowns. These macroprudential tools help maintain stability without halting the market entirely.

How to Calculate Your DTI Ratio: A Step-by-Step Guide

Calculating your DTI is straightforward and empowers you to check your borrowing capacity before approaching a bank. Use gross income (pre-tax) and include all debts.

Step 1: Tally Your Total Debt

Add up:

- Existing mortgage or home loan balances

- Car loans and personal loans

- Student loans (including any StudyLink debt)

- Credit card limits and overdrafts (full limits, not just balances)

- Any new borrowing you're applying for, like the proposed mortgage

Tip: KiwiSaver contributions or everyday expenses like rent don't count as debt here.

Step 2: Determine Your Gross Income

Include:

- Salary or wages

- Rental income from investments

- Self-employment earnings (use tax returns for proof)

- Other verifiable sources, like family trusts

Step 3: Apply the Formula

DTI = Total Debt ÷ Gross Annual Income

For example, if you and your partner earn $150,000 combined gross but have $900,000 in total debt (including a new $800,000 mortgage), your DTI is 6 ($900,000 ÷ $150,000). That's the threshold for owner-occupiers.

Plug your numbers into an online calculator from sites like MoneyHub for instant results.

New Zealand's DTI Lending Rules in 2026: The Current Limits

These rules apply to new residential lending by registered banks (not non-bank lenders). They remain unchanged into 2026.

Owner-Occupiers

You'll generally need a DTI of 6 or lower. Banks can approve up to 20% of new owner-occupier loans above 6, creating a 'high-DTI' quota. If your bank's quota is full, you might face rejection despite a solid application.

Investors

Investors face a 7 or lower DTI limit, with 20% allowance for higher ratios. This encourages prudent investment while allowing flexibility.

Real Kiwi Example: A couple earning $120,000 wants a $700,000 home with $50,000 other debt. New mortgage: $650,000. Total debt: $700,000. DTI: 5.83 (approved easily). Bump the loan to $750,000? DTI hits 6.67—high-DTI territory.

Exemptions and Exceptions

- New builds or construction loans

- Refinancing existing loans (with limits)

- Certain non-bank lenders

- Check RBNZ guidelines or consult a broker for your case

How DTI Ratios NZ Affect Your Borrowing Power

These rules cap how much you can borrow relative to income. A family on $100,000 might max out at $600,000 debt (DTI 6), limiting home choices in pricey Auckland. Investors on $80,000? Up to $560,000 (DTI 7).

Compared globally, NZ's limits (6-7) are moderate. Australia caps at 6 from February 2026, while Canada is stricter at 4.5.

DTI vs LVR: Understanding Both

| Metric | Measures | NZ Limit (Owner-Occupier) |

|---|---|---|

| DTI | Debt / Income | 6x (20% over) |

| LVR | Loan / Property Value | 80-95% (varies) |

Practical Tips to Lower Your DTI Ratio and Boost Approvals

A high DTI doesn't mean game over. Here's how Kiwis can improve theirs:

- Pay Down Debt: Clear credit cards or personal loans first—banks count full limits.

- Increase Income: Add rental income proof or a side hustle. Self-employed? Update IRD filings.

- Shop Lenders: Non-banks ignore DTI; compare via brokers.

- Time Your Application: Early in the month when quotas reset.

- Boost Deposit: Lower mortgage reduces total debt

Actionable Advice: Use KiwiBank's guides or a mortgage broker to pre-assess. Track via apps like PocketSmith.

"DTI rules mean buyers may not borrow as much as before—in most cases, no more than six times income." — OneRoof via Wright Financial

Common Scenarios: DTI Impact on First-Home Buyers and Investors

First-Home Buyers

With KiwiSaver withdrawals and First Home Grants, young couples can stretch further. But DTI caps often hit dual-income households eyeing Auckland semis.

Property Investors

Higher 7x limit helps, but interest deductibility changes add pressure. Focus on cashflow-positive properties.

Disclaimer: This isn't financial advice. Consult a licensed adviser or IRD for personalised guidance on taxes and KiwiSaver.

Next Steps: Take Control of Your Borrowing Today

Run your DTI numbers now, chat with a mortgage broker, and explore KiwiSaver boosts or WINZ support if needed. Staying under limits positions you strongly in NZ's competitive market. For tailored advice, visit ird.govt.nz or rbnz.govt.nz.

Track market shifts—DTI rules evolve. Position yourself to borrow smarter, not harder.

Frequently Asked Questions

Sources & References

-

1

New Zealand's Debt-to-Income Ratio Lending Rules Explained — lifetimes.co.nz

-

2

Debt to Income Ratios Explained - MoneyHub NZ — www.moneyhub.co.nz

-

3

Debt-to-income ratio (DTI): What is it and why does it matter? — wrightfinancial.co.nz

-

4

Understanding debt-to-income ratios - Home loans - Kiwibank — www.kiwibank.co.nz

-

5

DTI Rules Explained: What They Mean for NZ First-Home Buyers — www.newzealandmortgages.co.nz

-

6

Debt-to-Income Ratios (2026): Everything You Need to Know — www.opespartners.co.nz

-

7

APRA's New 2026 Debt-to-Income Rules - Camden Professionals — www.camdenprofessionals.com.au

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...