Mortgage Portability: Taking Your Loan to a New Property

Imagine you've finally found your dream home in a quieter suburb, but your current mortgage rate is locked in at a favourable deal you don't want to lose. That's where mortgage portability comes in—al...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Imagine you've finally found your dream home in a quieter suburb, but your current mortgage rate is locked in at a favourable deal you don't want to lose. That's where mortgage portability comes in—allowing Kiwis to transfer their existing loan to a new property without starting from scratch. In New Zealand's dynamic housing market, this option can save you thousands in fees and keep your repayments manageable, especially as rates stabilise around 4.5% by mid-2026.

Whether you're upsizing in Auckland, downsizing in Wellington, or relocating to Christchurch, understanding mortgage portability empowers you to move confidently. This guide breaks down everything you need to know, from eligibility to pitfalls, tailored for New Zealand homeowners navigating 2026's market.

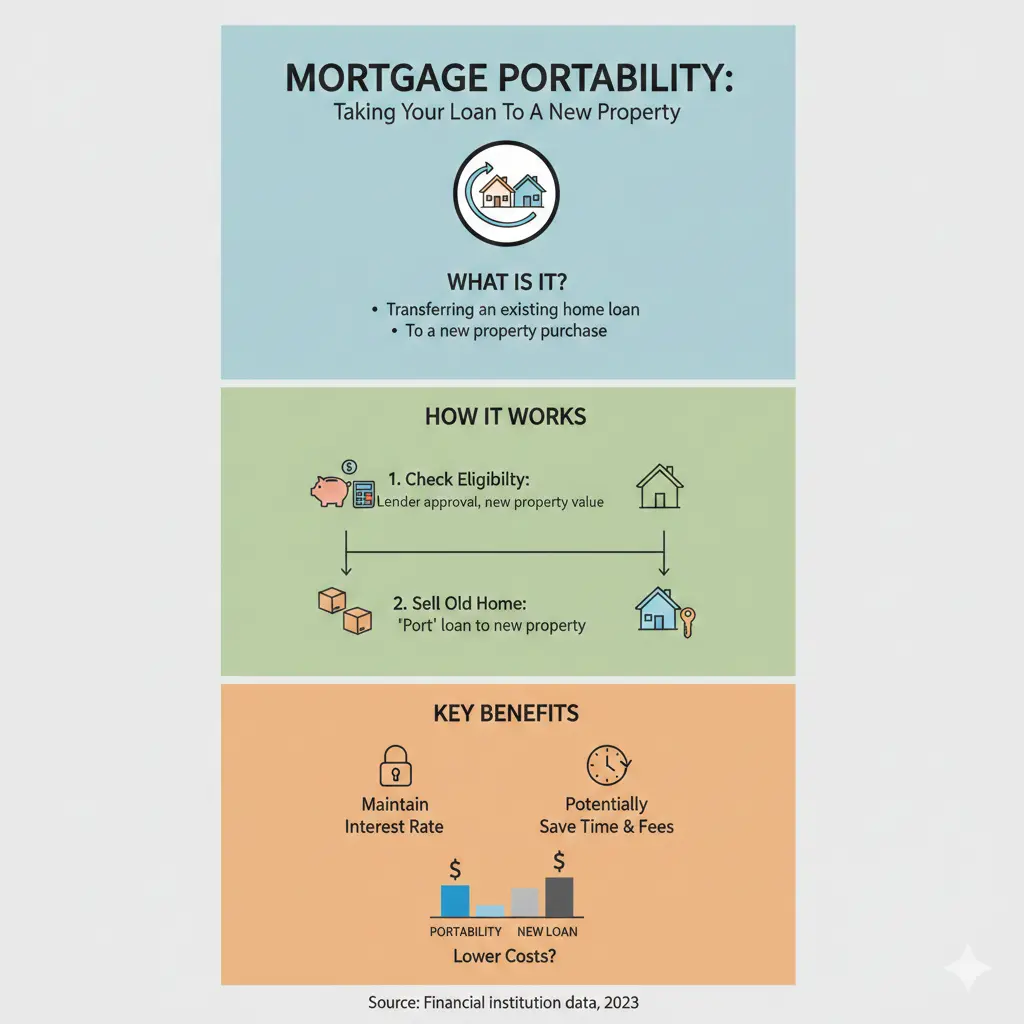

What is Mortgage Portability?

Mortgage portability, often called loan portability, lets you take your current home loan—complete with its interest rate, term, and conditions—and apply it to a new property when you sell your existing one. It's a feature offered by most major New Zealand banks like ANZ, ASB, BNZ, Kiwibank, and Westpac, designed to retain customers during property moves.

Instead of refinancing (which involves fresh credit checks, legal fees, and potentially higher rates), portability streamlines the process. Your loan balance transfers directly, preserving your fixed-rate deal if it's still competitive. With the Official Cash Rate (OCR) at 2.25% as of late 2025 and expected stability through 2026, holding onto a low rate via portability could be a smart move amid predictions of fixed rates between 3.50% and 6.00%.

How Mortgage Portability Works in Practice

- Sell your current home: Time your sale to align with purchasing the new property, minimising cashflow gaps.

- Notify your lender early: Contact your bank or mortgage broker 4-6 weeks before settlement to confirm portability eligibility.

- Valuation and approval: The bank values the new property; your loan-to-value ratio (LVR) must meet their criteria, typically under 80% without lenders mortgage insurance (LMI).

- Transfer the loan: On settlement day, the loan ports over seamlessly, with any equity from the sale reducing the balance or funding the purchase.

This process avoids break fees on fixed-rate loans, which can cost thousands if you refinance elsewhere.

Eligibility Criteria for Mortgage Portability in New Zealand

Not all loans qualify, so check your mortgage contract. Most standard residential loans from big four banks and Kiwibank support portability, but low-equity or interest-only loans might not.

Key Requirements

- Loan Type: Fixed, floating, or split loans usually qualify. Construction or investment property loans often don't.

- LVR Limits: The new property's LVR must comply with Reserve Bank rules—e.g., no more than 80% LVR for owner-occupiers in 2026.

- Equity Position: You need sufficient equity in the old home to cover any shortfall on the new purchase.

- Timeline: Port within 6-12 months of selling (varies by lender).

- Credit Check: A light re-assessment occurs, but no full re-application if your situation hasn't changed significantly.

For example, if your Auckland villa sells for $1.2 million with a $800,000 loan at 4.99% fixed, you can port that to a $1.1 million home in Hamilton, using the $400,000 equity as deposit.

Special Cases: First Home Buyers and Investors

First home buyers with KiwiBuild or progressive loans can often port, but confirm with your lender. Investors face stricter rules due to LVR restrictions (60% max in 2026), making portability trickier for rental portfolios.

Benefits of Mortgage Portability for Kiwis

In a market where 40-50% of mortgages refix soon with potential payment jumps of $200-$600 monthly, portability locks in stability. Here's why it's a game-changer:

- Retain Low Rates: Keep your sub-5% rate amid 2026 forecasts of 4.5% averages.

- Fee Savings: Avoid $2,000-$5,000 in legal and valuation fees, plus break costs up to 3 months' interest.

- Speed: Faster than refinancing; settlements align perfectly.

- Flexibility: Adjust loan splits post-port for affordability, like adding offset accounts.

- Market Timing: With housing confidence rebuilding and 5% value rises predicted, porting lets you move without rate risk.

Real Kiwi example: Sarah in Dunedin ported her 3.99% fixed loan from a townhouse to a family home, saving $15,000 in fees and maintaining payments at $2,800 fortnightly.

Potential Drawbacks and Risks

Portability isn't always seamless. Be aware of these hurdles:

Common Pitfalls

- New Property Valuation: If the new home values lower than purchase price, you may need extra deposit or face LMI.

- Rate Mismatch: Fixed terms don't extend; refix at current rates post-term (potentially higher than your original).

- Costs Still Apply: Discharge fee ($100-$300), new valuation ($500+), and legal fees ($1,000+).

- Upsizing Limits: Can't borrow more without lender consent and income proof.

- Market Volatility: 2026 refix shocks could hit if OCR rises unexpectedly.

Tip: Use a mortgage broker to compare portability vs. refinancing—tools like those from MoneyHub show if shopping around yields better deals.

Step-by-Step Guide: How to Port Your Mortgage in 2026

Follow these actionable steps for a smooth transition:

Preparation Phase (4-8 Weeks Out)

- Review your loan contract for portability clause.

- Engage a lawyer experienced in NZ property (find via NZ Law Society).

- Get pre-approval for the new property, disclosing intent to port.

- Calculate equity: Sale price minus loan minus costs.

Execution Phase

- Submit portability application to your bank with new property details.

- Arrange dual settlements: Old home sale funds new purchase.

- Monitor LVR—aim for <80% to avoid insurance.

- Post-port, review structure: Consider splitting terms for flexibility.

Pro Tip: Time your move for summer 2026 when listings peak, but sales volumes rise mildly.

Comparing Portability to Refinancing

| Factor | Mortgage Portability | Refinancing |

|---|---|---|

| Rate Retention | Yes, full transfer | New market rate |

| Fees | Low ($1,500-$3,000) | High ($3,000-$10,000+) |

| Time | 2-4 weeks | 4-8 weeks |

| Credit Check | Minimal | Full re-application |

| Best For | Similar value moves | Better rates/equity release |

In 2026's stable rate environment (OCR steady at 2.25%-3.50%), portability wins for most unless rates drop sharply.

Tax and Financial Implications

Porting doesn't trigger bright-line test for capital gains if owner-occupied. Update IRD for any equity changes affecting KiwiSaver or income-tested benefits like Working for Families. No GST on residential ports.

Disclaimer: This isn't financial advice. Consult a licensed adviser or use sorted.org.nz tools for personalised scenarios.

Next Steps for Porting Your Mortgage

Ready to move? Start by reviewing your loan docs and chatting with your bank or a mortgage adviser via the Financial Advice New Zealand. Compare rates using Canstar or Interest.co.nz, factor in 2026 forecasts, and get quotes from multiple lenders. Act early to capitalise on rebuilding market confidence. Your seamless property upgrade awaits—port smart, save big.

Always seek professional financial advice tailored to your circumstances. Rates and rules can change; verify with official sources.

Frequently Asked Questions

Sources & References

- 1

-

2

Interest Rate Predictions 2026 & 2027 - MoneyHub NZ — moneyhub.co.nz — www.moneyhub.co.nz

-

3

2026 Mortgage Rate Outlook: Scenarios, No Certainties! — newzealandmortgages.co.nz — www.newzealandmortgages.co.nz

- 4

- 5

- 6

- 7

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...