Reverse Mortgages NZ: Accessing Home Equity in Retirement

If you're approaching retirement and wondering how to make your home work harder for you financially, a reverse mortgage might be worth exploring. This type of loan lets you access the equity you've b...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

If you're approaching retirement and wondering how to make your home work harder for you financially, a reverse mortgage might be worth exploring. This type of loan lets you access the equity you've built up in your home without having to sell it or make regular repayments. For many Kiwis who are asset rich but cash poor, it can provide a financial lifeline during the retirement years.

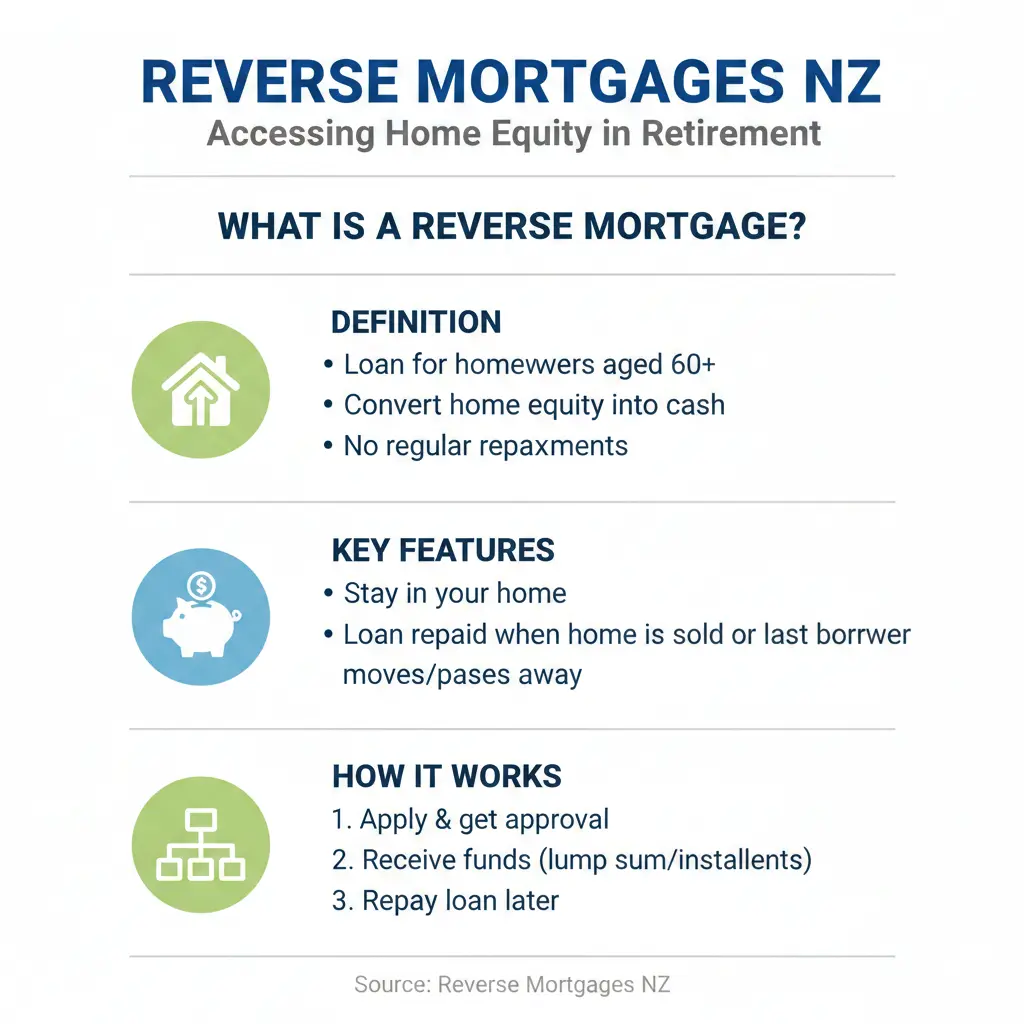

What Is a Reverse Mortgage?

A reverse mortgage is a specialised loan designed for people aged 60 and over that allows you to release equity from your residential property. Unlike a traditional mortgage where you make regular repayments to reduce what you owe, a reverse mortgage works in the opposite direction—the loan balance grows over time as interest compounds.

Instead of receiving a lump sum upfront, you can draw funds as needed or arrange regular advances. The key difference is that you're not required to make regular repayments of principal or interest while you're living in the home. Instead, the loan is repaid when you eventually sell the property, move into care, or pass away—at which point the property is usually sold and the loan is settled from the proceeds.

How Reverse Mortgages Work in New Zealand

New Zealand's reverse mortgage system includes important protections that set it apart from overseas schemes. All reverse mortgage providers in New Zealand guarantee that you cannot end up in a negative equity position. This means if the loan balance exceeds your home's value when it comes time to repay, you or your estate won't be pursued for the shortfall.

The amount you can borrow is calculated based on your age and your home's value. Generally, the older you are, the higher the percentage of your home's equity you can access. This approach protects your remaining equity for future needs.

Eligibility Requirements

To qualify for a reverse mortgage in New Zealand, you'll need to meet several criteria:

- Be aged 60 or over (some lenders require 70+)

- Own your home outright or be nearly mortgage-free

- Have your home as your principal residence or secondary property

- Own a standalone, residential property built with conventional construction

- Meet your lender's minimum property value requirements

If you have a small mortgage remaining, some lenders like Heartland Bank will help you clear it using part of your reverse mortgage funds.

The Costs You Need to Know About

Reverse mortgages come with a range of fees that can significantly impact your borrowing costs. These typically include:

- Valuation fee: usually $600+ to assess your home's value

- Application and establishment fees

- Drawdown fees for additional advances

- Mortgage discharge fees when the loan is repaid

- Legal fees for registration and discharge

Together, these fees can easily exceed $2,500. It's crucial to factor these costs into your decision-making.

Interest Rates and the Cost of Borrowing

One of the most significant considerations with reverse mortgages is the interest rate. Current reverse mortgage rates in New Zealand are typically around 10%, compared to standard mortgage rates of 6% to 8%. This is substantially higher than traditional home loans.

Here's where it gets critical: reverse mortgage interest rates are variable (floating), not fixed. If the Reserve Bank increases its official cash rate, your reverse mortgage rate will likely increase too. This compounding effect can be dramatic over time. A $100,000 loan borrowed over 20 years could cost $893,502 at 11% interest or $1,089,255 at 12% interest.

The reason for these higher rates is that lenders are providing funds over an extended period without regular repayments to reduce the principal.

Important Restrictions and Conditions

Before committing to a reverse mortgage, understand the lifestyle restrictions that come with it:

- You must live in the home: If you want to move into residential care or relocate elsewhere, you'll need to repay the loan first

- Limited rental options: You cannot rent out your entire property and live somewhere else, as this violates the agreement terms. However, renting one or two rooms while you live there is usually permitted

- Ongoing maintenance obligations: You must keep up with home insurance payments, council rates, and property maintenance to lender standards

- First mortgage only: Your lender must be the first and only mortgagee on the property—you cannot take out additional mortgages

Impact on Government Benefits and Your Estate

A crucial step before applying for a reverse mortgage is contacting Work and Income (WINZ) to understand how it might affect your supplementary benefits or other government financial support. The funds you access could potentially impact your eligibility for certain assistance programmes.

Additionally, if your goal is to leave your home to your family, a reverse mortgage will reduce the equity available in your estate. By the time the property is sold to repay the loan, there may be little or nothing left for your heirs, depending on how much you've borrowed and how long the loan has been outstanding.

When a Reverse Mortgage Might Make Sense

Despite the costs and restrictions, reverse mortgages can be appropriate for certain situations:

- You're asset rich but cash poor, with a valuable home but limited retirement income

- You plan to stay in your home for the long term

- You want to avoid selling your home or downsizing

- You need funds for essential expenses, healthcare, or home modifications

- You've exhausted other options like KiwiSaver withdrawals or downsizing

However, if you're considering a reverse mortgage simply to fund rising council rates or non-essential spending, it's worth exploring alternatives first.

Alternatives to Consider

Before committing to a reverse mortgage, explore other options that might better suit your situation:

- Downsizing: Selling your home and moving to a smaller, more affordable property

- Home equity loan: A traditional loan against your home where you make regular repayments

- KiwiSaver withdrawal: If you're over 65, you can withdraw your full balance

- Renting out a room: Generate income without taking on debt

- Retirement village options: Some villages offer equity release schemes or rental arrangements

Frequently Asked Questions

Getting Professional Advice

A reverse mortgage is a significant financial decision with long-term implications. Before applying, consider seeking advice from:

A financial adviser who specialises in retirement planning

Your solicitor, to understand the legal implications

Work and Income, regarding government benefits

Your accountant or tax adviser, if relevant

Take time to understand all the terms and conditions, compare different lenders, and ensure you're comfortable with the restrictions and costs involved.

Moving Forward

A reverse mortgage can be a valuable tool for accessing your home equity in retirement, particularly if you're in a genuine financial bind and plan to remain in your home long-term. However, it's not a decision to make lightly. The high interest rates, compounding costs, and lifestyle restrictions mean it should generally be considered only after exploring other options.

If you do decide to proceed, start by contacting Work and Income to understand any benefit implications, then speak with a qualified financial adviser who can assess your specific situation. Getting the right advice upfront could save you thousands of dollars and help you make a decision that genuinely serves your retirement goals.

Sources & References

Reverse Mortgages: Financial Lifeline or Liability? — McMillan&Co.

New Zealand Mayor Slammed for Recommending Reverse Mortgages — HousingWire

NZ Reverse Mortgage FAQs — Heartland Bank

Reverse Mortgages — MoneyHub NZ

Reverse Mortgages – What You Need To Know — Quay Law

Reverse Equity Mortgages — SBS Bank

Golden Years Doesn't Need to Mean Tight Budgets — Godfreys Law

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...